Genetic Signatures completes 90-day strategic review with $5M cost reduction

Genetic Signatures has completed its 90-day strategic review, delivering immediate structural changes and a clear path to profitability following decisive action by CEO Maria Halasz. The review identified an $5 million annualised cost reduction with full effect from FY2027, alongside a three-phase framework designed to stabilise the business, optimise operations, and ultimately scale revenue. The company maintains more than 500,000 tests per year through existing contracts whilst extending its cash runway to support delivery of stated strategic objectives.

The review framed Genetic Signatures’ turnaround as a three-horizon roadmap spanning Months 1-6 (Stabilise), Months 4-12 (Optimise), and Months 9-24 (Scale). Management has moved from diagnosis to action within the 90-day window, addressing cost structure misalignment head-on whilst protecting revenue-generating assets and preserving the company’s proprietary 3base® technology platform. The immediate outcome is a reset organisational structure, secured long-term supply agreements in Australia and Denmark, and paused US market investment pending development of a scalable business model.

When big ASX news breaks, our subscribers know first

What the review uncovered

The strategic assessment identified Genetic Signatures’ 3base® technology as a defensible scientific asset with untapped potential, but revealed organisational inefficiencies that constrained performance. The talented workforce was spread too thinly across overlapping research and development functions, whilst sales and business development resources remained insufficient. The fixed cost base proved unsustainably high relative to revenue, and cost control processes were not consistently observed.

The US market assessment revealed limited success despite the FDA 510(k) clearance for the EasyScreen™ Parasite Detection kit. Three key challenges emerged: reimbursement difficulties for the full pathogen portfolio, a workflow not fully automated for high-throughput laboratories, and a competitive landscape that evolved substantially since product launch. Legacy supply agreements were servicing customers beyond their economic value, creating margin pressure without corresponding strategic benefit.

| Finding | Opportunity |

|---|---|

| Revenue diversity limited | Focus on profitability with margin discipline |

| Cost base unsustainably high | $5M reduction implemented |

| US market underperforming | Paused until scalable model developed |

| 3base® technology underexploited | Comprehensive IP and product strategy in development |

The review confirmed the company’s proprietary 3base® chemistry delivers superior sensitivity in infectious disease diagnostics and holds potential in other applications. The EasyScreen™ assay range is validated across multiple PCR platforms and approved by regulators (IVD, 510(k), TGR), performing well in hospital and reference laboratories with low to medium throughput requirements. However, product differentiation varied by territory, creating additional regulatory, marketing, and production costs without corresponding value capture.

What is a strategic review and why do companies undertake them?

A strategic review is a systematic assessment of a company’s operations, market position, and resources to determine the optimal path forward. Companies typically undertake reviews following new leadership appointments, periods of underperformance, significant market changes, or when capital reallocation becomes necessary. The process examines every aspect of the business, from cost structure and product portfolio to geographic strategy and organisational design.

The typical outputs include cost restructuring programmes, market prioritisation decisions, organisational redesign, and updated capital allocation frameworks. Strategic reviews often serve as inflection points in a company’s trajectory, with investors closely monitoring whether management delivers on identified changes or reverts to previous patterns. In Genetic Signatures’ case, CEO Maria Halasz initiated the review immediately upon appointment to reset the business for sustainable growth.

Investors assess strategic reviews based on three factors: the depth of analysis, the speed of implementation, and the measurability of outcomes. Genetic Signatures has provided concrete metrics ($5M cost reduction, three-horizon timeline with specific deliverables) against which execution can be tracked. The 90-day timeframe from initiation to completed actions demonstrates management credibility and urgency.

Actions already completed

Genetic Signatures has executed four key deliverables within the review period, moving beyond planning to tangible outcomes:

-

Cost reduction programme: Completed line-by-line expenditure review delivering $5 million in annualised savings through rightsizing, with full effect from FY2027. Established purchasing processes and controls expected to generate further operational savings.

-

Organisational restructure: Brought quality control and customer support under unified leadership to improve responsiveness to customer requirements. Reset leadership accountabilities to increase productivity across the organisation.

-

Danish hospital contract: Signed strategically significant agreement with Hvidovre Hospital, demonstrating EMEA market traction and opening new European opportunities.

The 10-year Hvidovre Hospital agreement was secured through a competitive tender process, covers 28,000 gastrointestinal samples in year one with an estimated 3% annual volume growth, and is expected to serve as a reference site for further European sales cycles.

- Australian supply agreement: Secured long-term contract for EasyScreen™ gastrointestinal and respiratory detection kits, protecting the domestic revenue base.

The company implemented an AI policy and began AI-enablement of administrative and certain product development functions to drive productivity gains. Product upgrades addressing supply chain risks and improving laboratory workflow have been deployed, removing constraints on existing contract servicing. The restructured organisation increased cash runway to allow delivery of key strategic objectives without requiring immediate capital raising.

Execution within 90 days establishes management credibility against stated commitments. The Danish hospital contract signals tangible EMEA progress rather than aspirational market entry plans. The combination of cost reduction, revenue protection, and operational upgrades creates the foundation for the optimisation and scaling phases.

Geographic strategy reset

Australia and EMEA as priority markets

Genetic Signatures has designated Australia and EMEA as priority markets based on existing customer relationships, clear value proposition, and favourable regulatory environments. The company maintains long-term contracts delivering more than 500,000 tests per year, providing stable revenue whilst management implements the turnaround strategy. The EMEA growth signal emerges from the Hvidovre Hospital contract in Denmark, which validates the company’s clinical differentiation and opens new European opportunities.

Material reserves in Genetic Signatures’ instrument pool mean capital expenditure on new contracts will be limited. Existing instruments possess sufficient capacity to service Australian, EMEA, and APAC markets without requiring immediate investment in additional hardware. This capital-light expansion model aligns with the company’s profitability-first philosophy and enables margin discipline in new supply agreements.

APAC as the next growth frontier

The Asia-Pacific region represents Genetic Signatures’ Horizon 3 focus, positioned for execution during months 9-24 of the strategic roadmap. The company has appointed a Head of Sales and Support APAC with more than 20 years in senior business development roles in molecular diagnostics across Asia, commencing 1 July 2026. Low regulatory hurdles in several APAC countries enable faster market entry compared to more stringent jurisdictions.

The APAC appointment demonstrates forward commitment to the growth strategy rather than aspirational statements. Management is building sales infrastructure ahead of formal market entry, creating execution capacity before deploying capital into territory expansion. This sequencing reduces execution risk and ensures the organisation can support growth when opportunities materialise.

US market paused

Genetic Signatures has paused US market spending, redirecting resources to geographies with clearer paths to revenue. The decision reflects three challenges identified in the review: reimbursement difficulties for the full pathogen portfolio, workflow not fully automated for high-throughput laboratory requirements, and an evolved competitive landscape since the EasyScreen™ Parasite Detection kit received FDA 510(k) clearance.

The pause is disciplined capital allocation, not market abandonment. Laboratory Developed Tests (LDTs) not regulated by the FDA since 2025 offer a potential re-entry pathway for differentiated products delivering standalone clinical value with established reimbursement. The medium-term opportunity remains, but requires product design and commercialisation model adjustments before deployment.

The Optimus Prime instrumentation project has been paused in line with the US strategy reset. The project was developed to address high-throughput US laboratory requirements, and its suspension allows resource reallocation to EMEA and APAC markets where the existing instrument pool provides sufficient capacity. Management will revisit Optimus Prime alongside any potential US relaunch once a scalable business model is established.

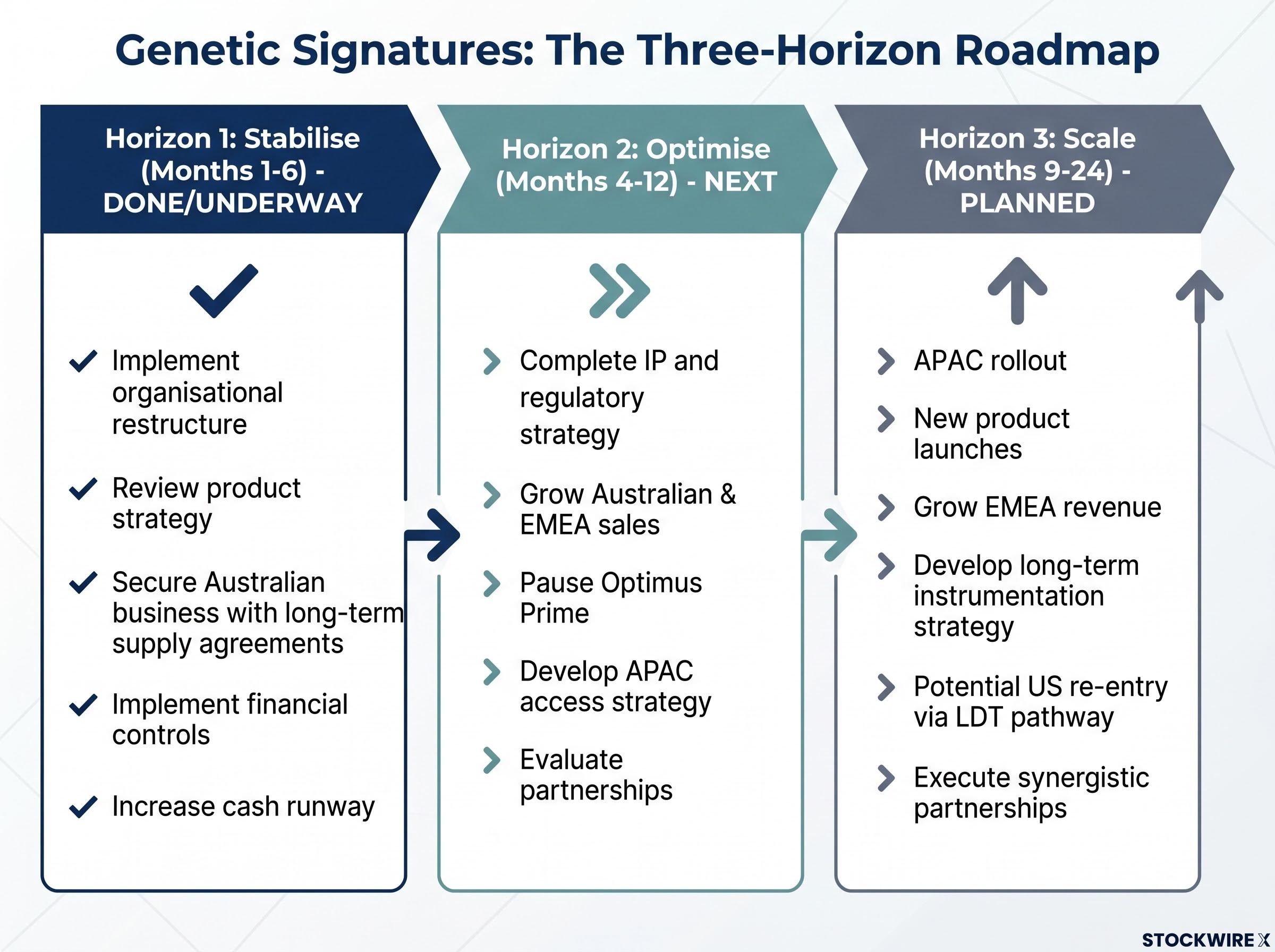

The three-horizon roadmap

Genetic Signatures has structured its turnaround as a phased approach balancing immediate stabilisation with medium-term optimisation and longer-term scaling:

Horizon 1: Stabilise (Months 1-6) — DONE/UNDERWAY

- Implement organisational restructure

- Review product strategy and market access approach

- Secure Australian business with long-term supply agreements

- Implement financial controls, savings programmes, and reporting systems

- Increase cash runway to support strategic delivery

Horizon 2: Optimise (Months 4-12) — NEXT

- Complete Board-endorsed IP, regulatory, product, and corporate strategy

- Grow Australian and EMEA sales from existing customer base

- Pause Optimus Prime and review instrumentation options

- Develop APAC market access strategy

- Settle organisational culture and stabilise workforce

- Evaluate potential partnerships as growth accelerators

Horizon 3: Scale (Months 9-24) — PLANNED

- APAC market rollout and revenue generation

- New product launches addressing broader geographic opportunities

- Grow direct EMEA business and distributor revenue

- Develop long-term instrumentation strategy

- Potential US market re-entry via LDT pathway

- Execute synergistic product and corporate partnerships

The guiding philosophy prioritises profitability over revenue, with margin discipline applied to new contracts. Large supply agreements will improve unit economics, and every dollar spent requires justification against expected return, timeframe, and risk. This outcome-based capital allocation replaces the previous activity-based spending model.

The three-horizon structure de-risks execution by creating clear stage gates. Investors can track progress against stated milestones rather than assessing management against vague transformation narratives. Horizon 1 is substantially complete, with cost reductions implemented, key contracts secured, and organisational structure reset. Horizon 2 activities are underway, including the APAC leadership appointment and partnership evaluation processes.

Leadership team driving the turnaround

The executive team combines sector-specific credentials with direct experience in product commercialisation, global market access, and organisational turnaround:

-

Maria Halasz, Chief Executive Officer: More than 20 years in senior management roles across the life sciences sector, including prior listed company CEO experience. Track record includes licensing diagnostics and leading global product launches.

-

Susanne Petersen, Chief Technology Officer: More than 20 years in molecular diagnostic product development, covering assay and clinical development alongside regulatory oversight. Responsible for 3base® technology exploitation strategy.

-

Angela Wang, Head of Finance: Four years as Genetic Signatures Financial Controller with thorough knowledge of operations and finances. Driving the company’s AI strategy alongside financial control implementation.

-

John Buckels, Head of Sales and Support EMEA: More than 15 years in senior business development roles in infectious disease diagnostics globally, bringing industry knowledge and extensive European contacts.

-

Peter Njuguna, Head of Product Care, Q&S: Technology development background with experience across the full product cycle, including customer support, compliance, and quality control.

-

Head of Sales and Support APAC (commencing 1 July 2026): More than 20 years in senior business development roles in molecular diagnostics across Asia, with deep regional knowledge and established networks.

The APAC appointment signals commitment to geographic expansion ahead of formal market entry, creating execution capacity before deploying capital. The leadership structure brings quality control and customer support under the same reporting line, improving responsiveness to customer requirements identified in the strategic review.

Investment thesis following the review

Management has articulated six strategic principles forming the post-review investment framework:

-

Stabilise before optimising and scaling: Right-sized cost base, stabilised customer relationships, realigned organisational structure, and implemented sustainable controls and reporting systems. Outcome: increased cash runway without immediate capital raising requirement.

-

Profitability over revenue: Large contracts structured to improve unit economics. Quality of revenue matters more than headline growth. Margin discipline applied to all new contracts, even if short-term revenue fluctuates.

-

Outsourced business model: Focus on organisational strengths (3base® chemistry, assay validation, customer relationships) whilst outsourcing non-core activities including most research and development expenditure.

-

Capital allocation discipline: Every dollar spent justified against return, expected outcome, timeframe, and risk. Activity-based spending replaced with outcome-based capital allocation.

-

Focus on growth: EMEA, APAC, and Australia prioritised for expansion based on existing customers, clear value proposition, and low regulatory hurdles. US remains medium-term opportunity pending scalable model development.

-

Partnerships as force multipliers: Active pursuit of synergistic partnerships with manufacturers, service providers, OEM partners, and instrument manufacturers. Evaluate corporate partnerships where strategic alignment exists.

The 90-day review has reset investor expectations by establishing measurable milestones against which execution can be tracked. The company moves from aspirational transformation narrative to concrete deliverables: $5 million cost reduction verified, Danish and Australian contracts secured, APAC leadership hired, and organisational structure finalised. Execution against Horizon 2 and Horizon 3 objectives will determine whether Genetic Signatures converts stabilisation into sustainable growth and margin expansion.

1H FY26 operating performance showed revenue of $8.7 million, up 2.4% year-on-year, with underlying losses improving 23.8% to $6.4 million, providing the financial baseline against which the $5 million cost reduction targets its FY2027 profitability inflection.

Ready to Explore How Genetic Signatures Plans to Reach Profitability?

The strategic review has delivered concrete actions including $5 million in cost reductions, long-term supply agreements, and a three-horizon roadmap designed to stabilise operations and scale revenue. Management’s 90-day execution demonstrates credibility whilst extending the cash runway to support delivery of stated objectives.

For investors assessing the turnaround thesis, comprehensive company research materials including financial models, management track records, and detailed strategic analysis are available through the Genetic Signatures investor centre. The centre provides access to historical performance data, upcoming milestones, and independent research to support informed investment decisions.