Micron Confirms HBM4 Deal, Then Falls 7.7% in AI Selloff

1 hr ago

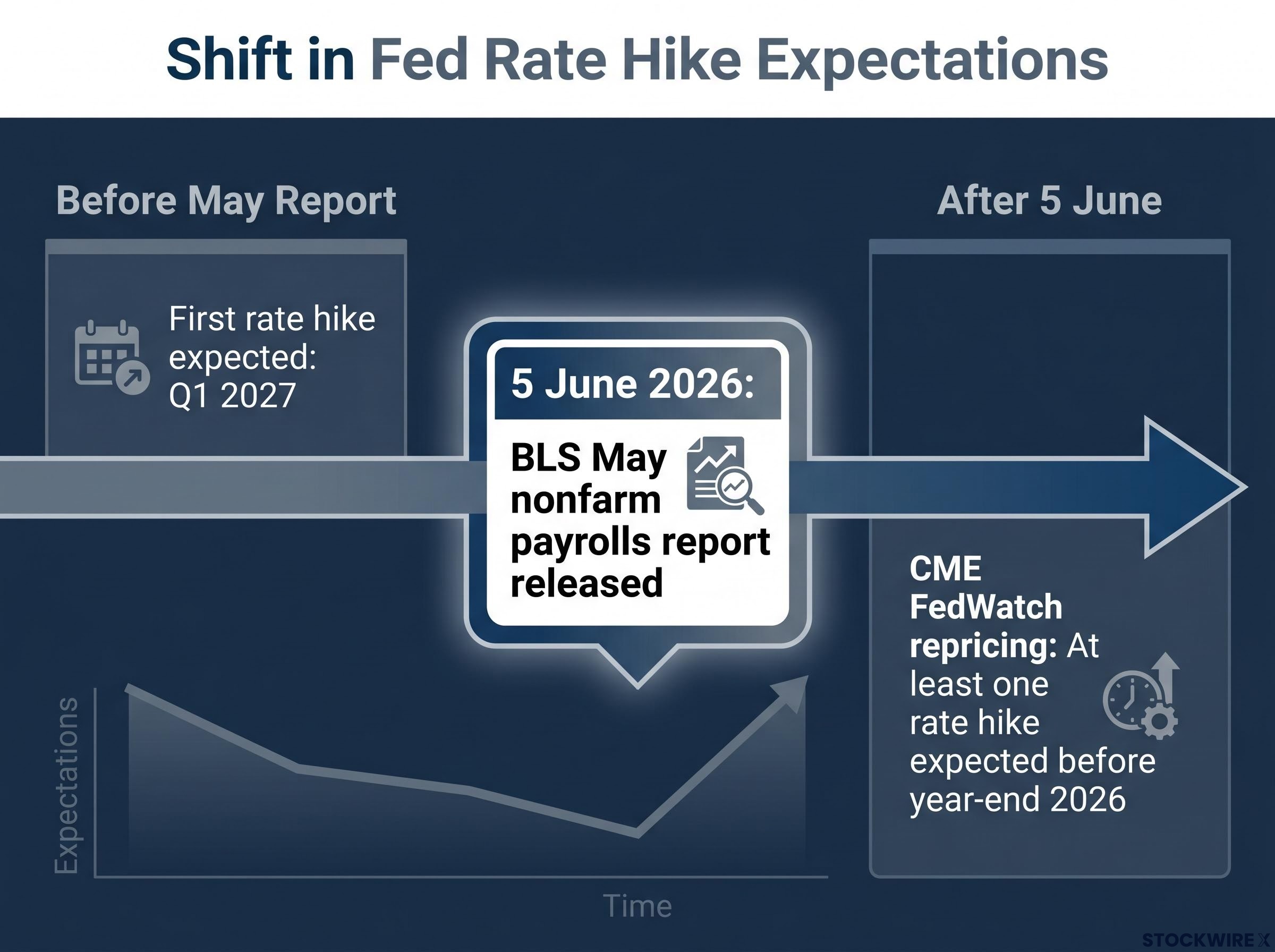

Before Friday’s open, markets had largely written off a 2026 Federal Reserve rate hike. By mid-morning, that consensus was gone. The May nonfarm payrolls report, released 5 June 2026 by the Bureau of Labor Statistics (BLS), surprised to the upside with enough force to reprice Fed funds futures in real time, pulling the first expected rate increase from early 2027 into the final months of 2026.

The shift lands in an already complicated macro environment. U.S.-Israeli military operations in Iran, now in their fourth month, have kept oil prices elevated and inflationary risk alive. For investors who built positioning around a Fed on hold through year-end, the repricing raises an immediate question: is this a durable policy signal, or a single-report overreaction?

What follows is an assessment of what the jobs data actually showed, how markets repriced in real time, what moderating factors could cap the hawkish shift, why the Iran conflict complicates the Fed’s response, and what investors should monitor from here.

The surprise was real, but it was not uniform across every metric. The May payrolls figure came in stronger than consensus expectations, delivering the kind of beat that moves institutional pricing rather than one that gets revised away in the next month’s update. Before the release, the prevailing view was straightforward: the Fed would hold borrowing costs steady through the remainder of 2026, with the first rate increase arriving no earlier than Q1 2027.

The May payrolls release was the marquee event in a dense June 2026 data calendar that also covered eurozone CPI, ISM manufacturing and services surveys, and Canadian employment, making it one of the most consequential macro weeks of the mid-year period for investors tracking central bank policy shifts.

That timeline lasted until the data hit screens. The three components that mattered most told a nuanced story:

Before the May report, markets priced the first Fed rate hike for early 2027. By mid-morning on 5 June, CME FedWatch pricing had shifted to reflect at least one hike before year-end 2026.

The distinction matters. This was a payrolls beat strong enough to reprice the policy timeline, but the accompanying unemployment and wage figures left room for debate about how far that repricing should go. That nuance is what separates a signal from an overreaction.

The repricing followed a mechanical sequence that investors can track in real time through the CME FedWatch Tool, which translates Fed funds futures pricing into implied probabilities of rate decisions at specific Federal Open Market Committee (FOMC) meetings. When futures contracts move, the tool recalculates the market-implied likelihood of a hike, cut, or hold at each upcoming meeting.

On 5 June, the sequence ran as follows:

The result was a clean directional move: markets went from pricing no action in 2026 to pricing at least one hike before the year closes. That is a material shift in institutional positioning, not a marginal tweak.

The May payrolls beat accelerated a shift that had already been building for weeks: the Fed rate outlook repriced sharply through late April and May as sticky core PCE data and hawkish official signals moved institutional money from pricing 50-75 basis points of cuts to assigning meaningful probability to a hike before year-end.

Analysts at Vital Knowledge characterised the payrolls beat as tilting Fed expectations toward tightening, while noting that the move was unlikely to trigger a dramatic shift in the broader policy outlook. The reading frames this as a measured hawkish pivot, not the opening of an aggressive hiking cycle.

That distinction carries weight. A single strong report changes probabilities; it does not change the Fed’s institutional posture overnight. The question now is whether subsequent data confirms or contradicts the signal.

A strong jobs report shifts market pricing. It does not, by itself, lock in a rate hike. The gap between those two statements is where the Fed’s decision-making framework lives.

The Federal Reserve operates under a dual mandate set by Congress: maximise employment and maintain price stability. Both sides of that mandate feed into rate decisions. A strong labour market satisfies one half; inflation data determines the other. The FOMC weighs both before moving.

The Federal Reserve dual mandate, as defined by Congress, requires the FOMC to pursue maximum employment alongside price stability, with the central bank’s 2 percent inflation target serving as the operational benchmark against which wage and price data are measured when rate decisions are under consideration.

Beyond payrolls and inflation, the Fed monitors a range of inputs that shape its cumulative assessment:

The Fed’s rate decisions reflect accumulated evidence across these inputs, not a reactive call based on a single report.

Fed officials have consistently framed rate decisions as cumulative assessments. The phrase “data-dependent” is not a hedge; it is a description of how the FOMC actually operates. No single payrolls report, regardless of its strength, guarantees a policy change at the next meeting.

The moderate unemployment and wage growth figures in the May report are exactly the kind of mixed signal that complicates a clean hawkish interpretation. Payrolls beat expectations, but wages did not spike and unemployment did not plunge. That combination shifts probabilities without closing the debate.

Investors who treat the CME FedWatch Tool as a deterministic forecast rather than a probabilistic snapshot risk repositioning on incomplete information. It measures where institutional money sits today; it does not predict where the Fed will land in three months.

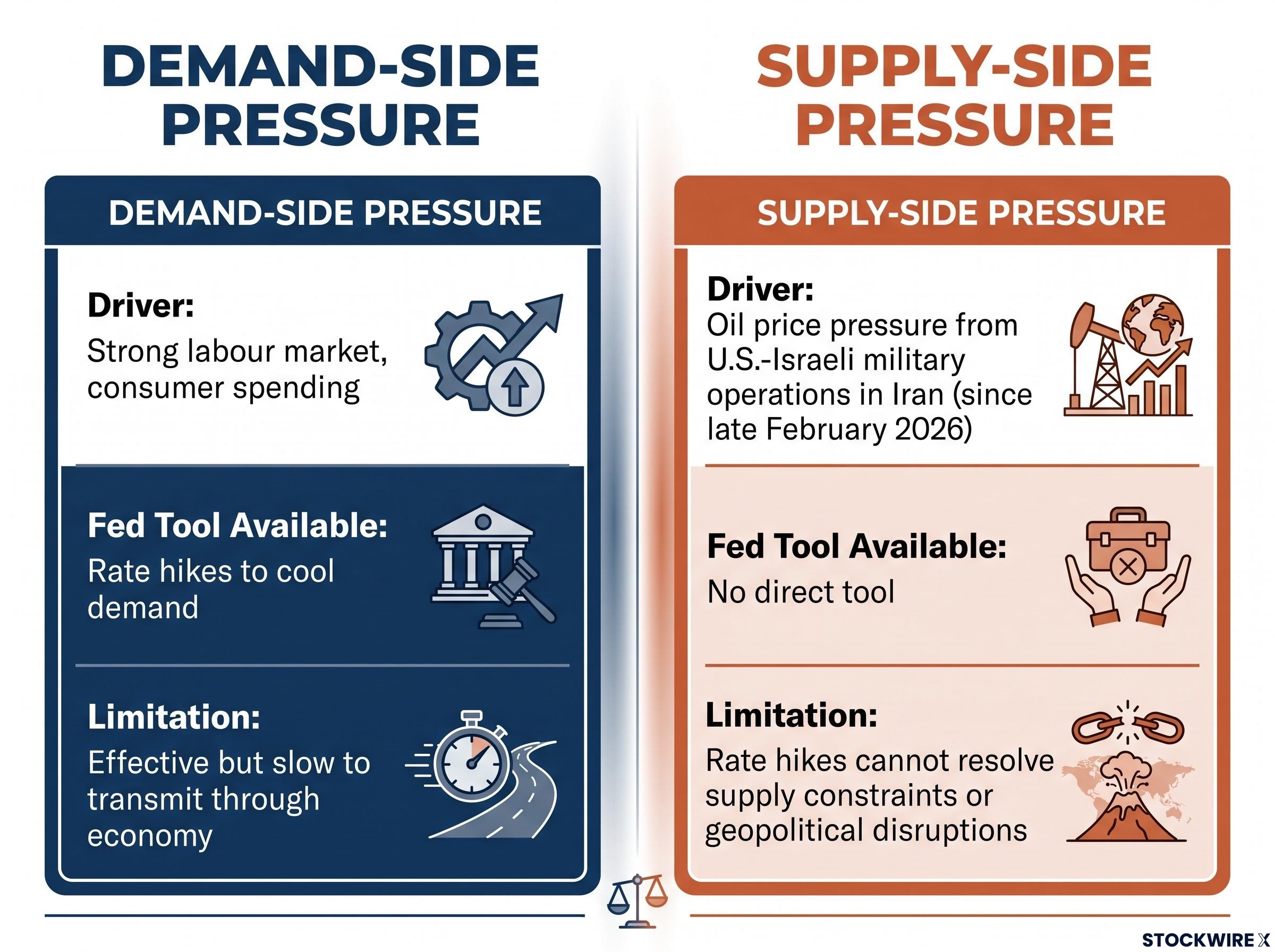

The jobs report did not arrive in a vacuum. The U.S.-Israeli military engagement with Iran, which began in late February 2026, has been running for more than three months. Over that period, elevated oil prices have fed into headline inflation readings, adding a second variable to the Fed’s policy calculus that complicates the signal from the labour market.

The transmission mechanism is direct. Conflict disrupts oil supply or raises supply-risk premiums; higher oil prices flow into transport, manufacturing, and consumer energy costs; those costs push headline inflation higher. The Fed then faces a question it cannot answer with a single tool.

Goldman Sachs estimates that a sustained $10-$20 per barrel crude increase adds several tenths of a percentage point to U.S. headline CPI over 12 months, a transmission path that operates independently of the labour market strength the Fed would normally address with rate adjustments, and the geopolitical risk premium embedded in current oil prices is itself highly reversible if diplomatic conditions change.

| Pressure Source | Driver | Fed Tool Available | Limitation |

|---|---|---|---|

| Demand-side | Strong labour market, consumer spending | Rate hikes to cool demand | Effective but slow to transmit through economy |

| Supply-side | Oil price pressure from Iran conflict | No direct tool | Rate hikes cannot resolve supply constraints or geopolitical disruptions |

A strong jobs market and oil-driven inflation are not the same problem, and rate hikes address only one of them. The Fed can cool demand; it cannot reopen supply lines in the Middle East.

This is the tension that makes the current environment genuinely uncertain. If the Fed hikes to address demand-side heat, it simultaneously tightens financial conditions in an economy already absorbing a supply-side shock. If it holds to avoid compounding the supply-side damage, it risks allowing demand-driven inflation to build. Neither path is clean.

The repricing is real, but it is not settled. Whether the market’s hawkish shift holds depends entirely on whether the data that follows confirms the May jobs report as the start of a trend or reveals it as a one-off beat. The difference between those two outcomes determines whether the Fed actually moves.

The asset classes most directly exposed to a confirmed 2026 rate hike are already repricing:

The three data releases that will most determine whether this repricing holds are:

One data point shifts probabilities. A trend locks in expectations. Investors do not need to reposition entire portfolios on the strength of a single report, but they should know which holdings carry the most exposure if the trend confirms.

For investors who want to move from tracking the repricing to acting on it, our dedicated guide to investing during rate hikes covers portfolio recalibration strategies across equities and fixed income, with specific attention to high-margin, low-debt sectors that have historically held up when monetary conditions tighten against an energy cost backdrop.

The May payrolls beat was a genuine signal shift. The CME FedWatch repricing reflects legitimate institutional reassessment, not noise. Markets moved from pricing no hike in 2026 to pricing at least one before year-end, and that move was grounded in data, not sentiment.

The moderating factors remain real. Wage growth and unemployment were not alarming, and the Fed’s data-dependent stance means this is a probability shift, not a locked-in outcome. A single report opened the door; it did not walk through it.

The Iran conflict keeps the policy outlook genuinely uncertain even after the jobs data provided partial clarity. The Fed is now navigating two distinct inflationary pressures with a toolkit designed for one of them.

Investors who want to stay ahead of the Fed’s evolving stance should monitor the next BLS employment release and the upcoming PCE inflation print as the clearest confirmations, or contradictions, of Friday’s repricing signal.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Fed rate hike expectations refer to the market's implied probability of the Federal Reserve raising interest rates at upcoming FOMC meetings, typically measured in real time using the CME FedWatch Tool, which translates Fed funds futures pricing into percentage likelihoods of a hike, cut, or hold.

The May 2026 nonfarm payrolls report came in stronger than consensus forecasts with enough breadth to signal genuine labour market momentum, prompting traders to sell Fed funds futures contracts priced for rates on hold through 2026 and pushing the implied timeline for the first hike forward from early 2027 to before year-end 2026.

The ongoing U.S.-Israeli military engagement with Iran has kept oil prices elevated, feeding supply-side inflationary pressure that rate hikes cannot directly address; this forces the Fed to weigh demand-side tightening against the risk of compounding economic damage from an energy cost shock it has no tool to resolve.

Long-duration Treasuries, utilities sector equities, and real estate investment trusts (REITs) carry the highest direct exposure, as rising rate expectations push bond yields higher, compress present values of stable cash flows, and raise financing costs for leverage-dependent structures.

The next BLS employment report, the upcoming CPI release, and the language in the next FOMC meeting statement are the three key indicators: a second payrolls beat and elevated inflation would reinforce the hawkish shift, while a miss on either would likely unwind much of the repricing.