Helloworld Cuts FY26 Guidance as Middle East Conflict Crushes Airline Margins

Helloworld Travel revises FY26 earnings guidance amid Middle East travel disruption

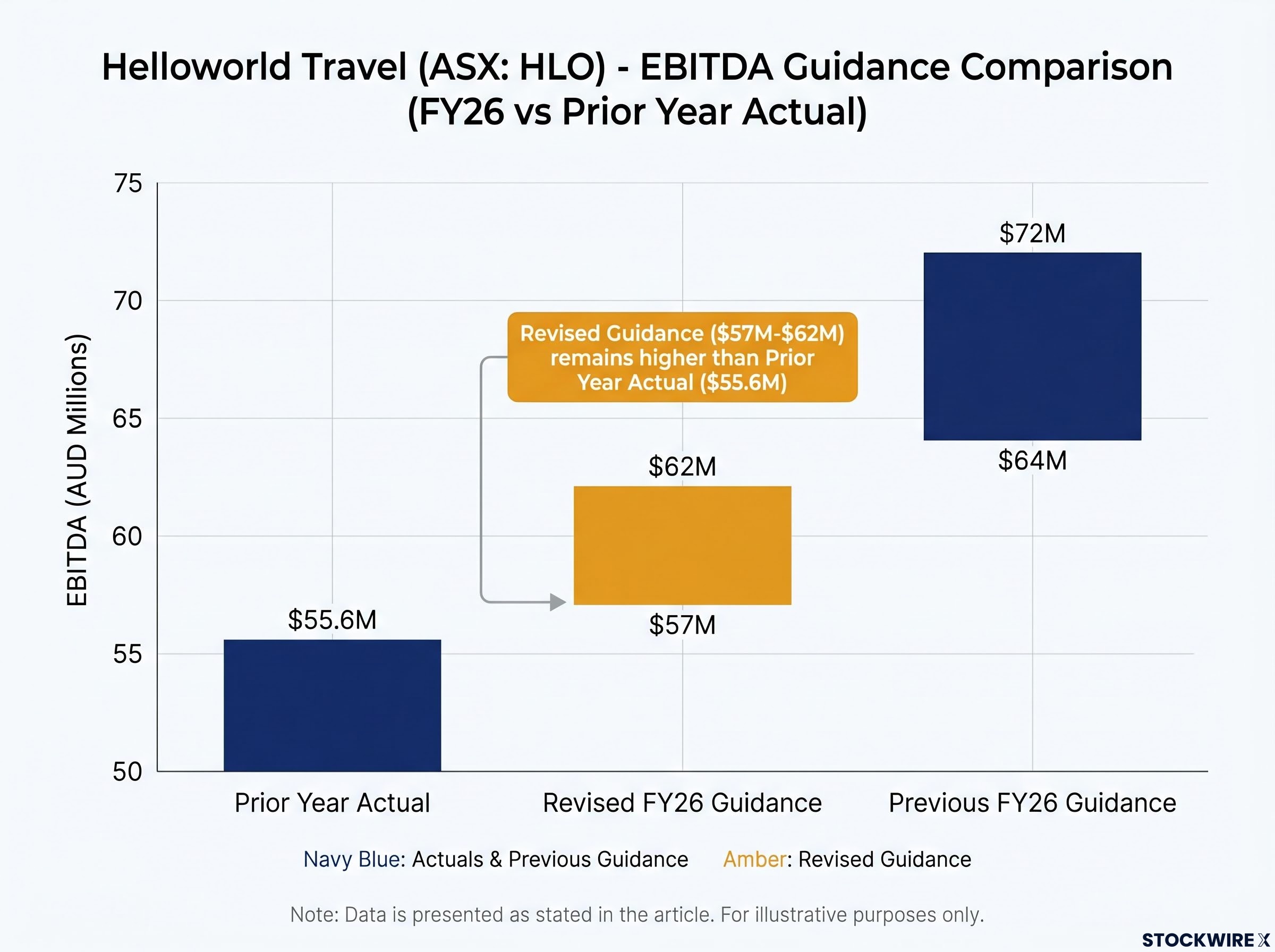

Helloworld Travel (ASX: HLO) has revised its FY26 Underlying EBITDA guidance to $57 to $62 million, down from the previously stated range of $64 to $72 million. The downgrade reflects disruption caused by the Middle East conflict, which has interrupted flight routes through Dubai, Doha, and Abu Dhabi. Despite the revision, the new guidance range still represents growth above the prior year actual of $55.6 million. The guidance excludes any fair value remeasurement of the company’s investment in Webjet Group Limited.

Despite the near-term earnings pressure, forward bookings from July onwards are tracking ahead of last year, signalling resilience in underlying travel demand.

When big ASX news breaks, our subscribers know first

How Middle East airspace disruptions reshaped Q4 booking patterns

Before the conflict escalated, Q4 FY26 air sales were tracking strongly above the prior corresponding period — approximately 29% higher in Australia and 16% higher in New Zealand. However, high levels of cancellations and re-bookings have shifted the trajectory, with Q4 FY26 now tracking approximately 4% below the prior year for both markets.

The capacity constraint has been severe. International flights departing from Australia on the three major Middle Eastern carriers (Emirates, Qatar, and Etihad) dropped from 150 per week to nil in March, recovering to approximately 82 per week currently. The reduction in Middle Eastern carrier capacity has forced a shift in booking patterns towards Asian carriers, which typically offer lower override income for travel agencies. Higher jet fuel prices have compounded the impact, leading to elevated air ticket pricing that has dampened new travel demand.

| Metric | Pre-Conflict Trajectory | Current Position |

|---|---|---|

| Australia Q4 air sales vs pcp | +29% | -4% |

| New Zealand Q4 air sales vs pcp | +16% | -4% |

| ME carrier weekly flights | 150 | ~82 |

The carrier mix shift has had a disproportionate impact on earnings. Override income, which is commission revenue earned from airlines when volume targets are met, has moved away from higher-yielding partnerships with Middle Eastern carriers to lower-yielding deals with some Asian carrier partners. This explains why the earnings downgrade is more pronounced than the booking volume decline alone would suggest.

What is airline override income and why does carrier mix matter?

Override income is commission revenue travel agencies earn from airlines when they hit volume targets with specific carrier partners. For Helloworld, this means that when the company books a certain threshold of seats with Emirates, Qatar, or Etihad, it receives enhanced commission rates on top of standard fees.

The Middle East conflict disrupted this dynamic. When flights via Dubai, Doha, and Abu Dhabi stopped or reduced sharply, customers re-booked onto alternative routes operated by Asian carriers. These alternative carriers typically offer lower commission structures than the Middle Eastern partners Helloworld had lucrative deals with. As a result, the same number of tickets sold can generate less revenue if the carrier partnerships yield lower margins.

This explains why the earnings impact is disproportionate to the booking volume decline. It is a margin compression issue, not just a volume issue. The shift in carrier mix reduces the profitability of each transaction, even when total bookings recover.

Premium travel and non-air revenue show structural resilience

Despite the disruption, Helloworld’s product mix continues to improve, supporting earnings quality over the longer term. Premium seat bookings (premium, business, and first class) now represent approximately 53% of air sales by dollar value in Australia and 50% in New Zealand for the year to date in FY26. This compares to 50% and 46% respectively in the prior year.

Non-air revenue is also gaining share. For the year to date ending April 2026, Helloworld’s Australian retail networks derived:

- 63% of sales from air bookings

- 37% of sales from higher-yielding non-air products (including land, cruise, insurance, and car hire)

This compares to 66% and 34% respectively in the prior year.

In New Zealand, the split is 71% air and 29% non-air for the year to date, compared to 81% and 19% in the prior year.

Management has framed leisure travel as “firmly entrenched as a non-discretionary item” for Helloworld’s core demographic. The resilience of premium bookings and the growing contribution from non-air products suggest the company is capturing higher-value customers who continue to prioritise travel spending despite macroeconomic headwinds.

Dividend outlook and shareholder returns

Helloworld anticipates paying an FY26 final dividend similar to the FY26 interim dividend paid in March 2026, subject to the finalisation of FY26 financial statements and final determination by the Board of Directors. At the company’s closing share price of $1.40 on 4 June 2026, this would represent a fully franked yield of approximately 7% per annum.

The dividend guidance signals management’s commitment to shareholder returns despite the near-term earnings pressure from the Middle East conflict. The Board’s intention to maintain dividends at prior levels suggests confidence in the company’s cash generation capacity and the transient nature of the current disruption.

Webjet stake and recovery outlook

Helloworld currently holds 78,250,205 ordinary shares in Webjet Group Limited (ASX: WJL), representing 20.118% of voting power when adjusted for WJL’s share buybacks. The company is WJL’s largest shareholder and continues to monitor the performance of the business and assess its options regarding the investment.

Management has indicated that, based on previous experience with travel disruptions, demand is anticipated to recover to previous levels within 60 to 90 days of a resolution to the conflict. Forward bookings from July onwards are already tracking above the prior year, reinforcing this view.

Andrew Burnes, CEO & Managing Director

“People want to travel, they want the services of a travel professional to make sure it is done right, and they want to have the back up of a travel professional if anything goes wrong along the way.”

The resilience of forward bookings supports management’s view that underlying demand for leisure travel remains robust, particularly for the complex, multi-destination trips that characterise Helloworld’s core market in Australia and New Zealand.

The next major ASX story will hit our subscribers first

Investor call details

CEO Andrew Burnes and CFO Mike Smith will host an investor phone call to discuss the trading update on Tuesday, 9 June 2026 at 11:00am AEST. The registration link is available in the ASX announcement.

Could Middle East Airspace Disruptions Create a Buying Opportunity for Helloworld Travel Investors?

Despite near-term earnings pressure from reduced Middle Eastern carrier capacity, Helloworld’s forward bookings from July onwards are tracking ahead of last year, whilst premium travel and non-air revenue continue to show structural resilience. The company maintains its commitment to shareholder returns with an anticipated fully franked dividend yield of approximately 7% per annum.

Management expects demand to recover within 60 to 90 days of a conflict resolution, based on previous travel disruption patterns. For detailed financial performance metrics and strategic positioning, visit the Helloworld Travel investor centre to access the full trading update and upcoming investor call details.