Passive Income Investing in Australia: What Actually Works

36 mins ago

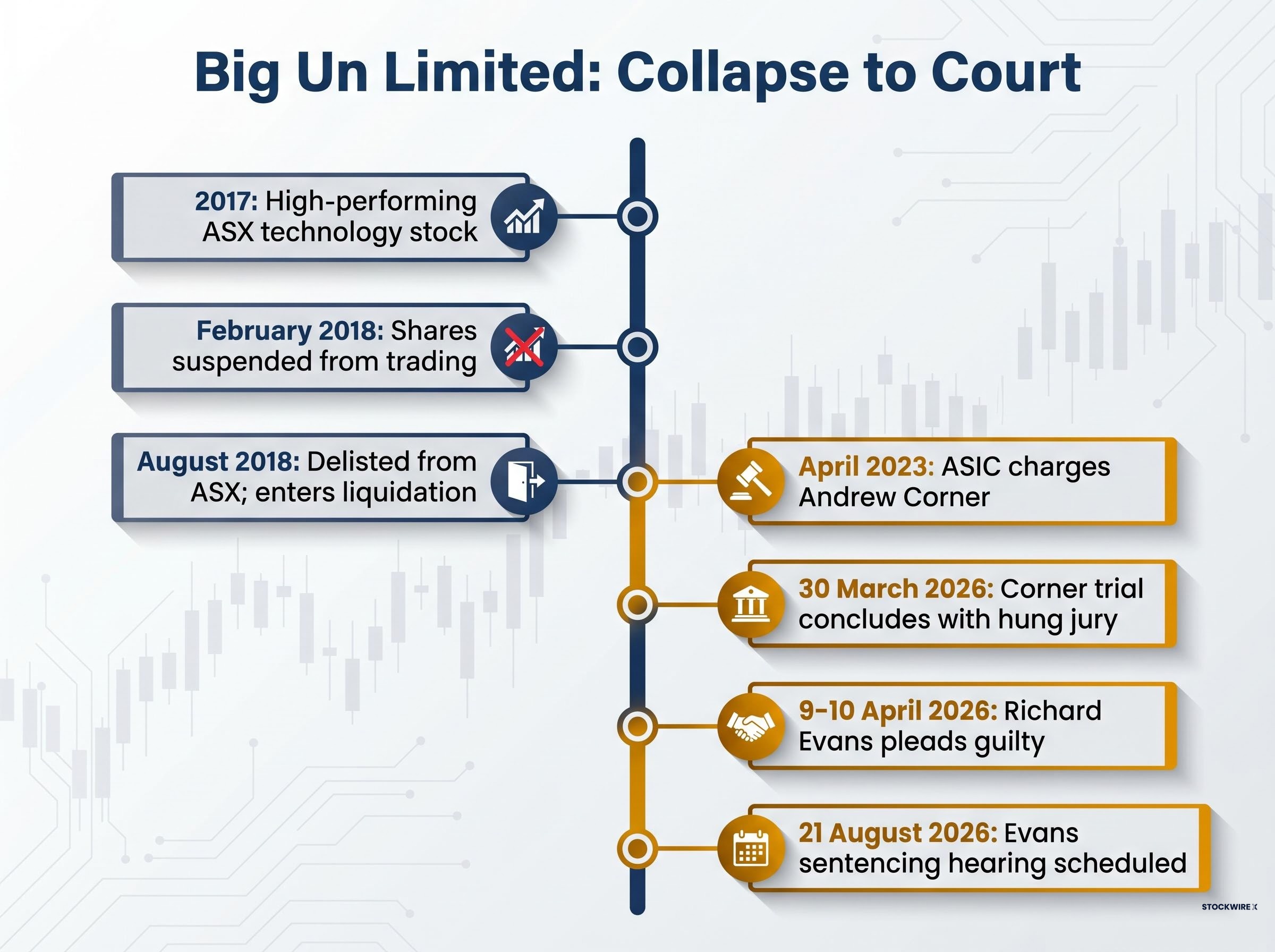

An ASX-listed technology stock that looked like one of 2017’s standout performers had collapsed entirely by mid-2018. Nearly eight years later, two of its former executives are still working through the legal consequences. The Big Un Limited collapse remains one of the more instructive examples of governance failure in Australian small-cap technology stocks, and both enforcement threads reached significant milestones in early 2026. A hung jury was delivered on 30 March 2026 in the former CFO’s trial. The former CEO entered a guilty plea in April 2026. Together, these developments brought the case back into focus.

This article reconstructs the full arc of what happened at Big Un Limited, explains how ASIC’s insider trading proceedings against Andrew Corner and Richard Evans unfolded, and unpacks what a hung jury means for the Corner case going forward. Readers will come away with a clear picture of both the corporate collapse and the regulatory response it triggered.

Big Un Limited was, for a time, precisely the kind of ASX small-cap technology story that attracts retail investor attention: a company with a rising share price, a growth narrative, and a profile that outpaced its size. Through 2017, the stock was regarded as a high-performing ASX-listed technology company.

The trajectory reversed with startling speed. The collapse moved through three distinct stages:

The gap between apparent success and corporate failure was measured in months, not years. That speed matters because it contextualises why ASIC’s subsequent enforcement action centred on conduct that allegedly occurred while insiders still held material non-public information about the company’s true condition.

Australian insider trading law targets a specific kind of unfairness: the use of material information that the broader market does not yet have. In practical terms, the prohibition covers two distinct forms of conduct. A person who possesses inside information must not trade in the relevant securities, and must not communicate that information to another person who might then trade on it.

The core prohibition, in plain terms: A corporate insider who holds information that would, if made public, reasonably be expected to have a material effect on the price of a company’s securities is prohibited from trading in those securities or passing that information to others.

The distinction between these two forms of liability is precisely what separates the allegations against the two former Big Un executives.

The two prohibitions at the centre of both proceedings, trading on inside information and communicating it to others, both derive from section 1043A of the Corporations Act, which establishes the statutory definition of inside information and the conditions under which those prohibitions are engaged.

| Type of Conduct | Corner Allegation | Evans Charge | Legal Basis |

|---|---|---|---|

| Trading on inside information | Allegedly sold 1.7 million Big Un shares worth more than $5 million while in possession of inside information | Not applicable | Prohibition on trading while holding material non-public information |

| Communicating inside information | Not applicable | Pleaded guilty to one charge of communicating inside information | Prohibition on disclosing material non-public information to others |

Corporate officers such as CFOs and CEOs are natural targets for insider trading scrutiny. Their roles grant them direct and continuous access to material non-public information, from funding arrangements to financial results, in the ordinary course of business. When a company’s circumstances deteriorate before that deterioration becomes public, it is the C-suite that holds the information asymmetry.

The information asymmetry that characterises insider trading cases often originates in the same window where continuous disclosure obligations are being tested: the gap between when an executive becomes aware of material information and when that information reaches the market.

ASIC filed charges against Corner in April 2023, more than five years after the collapse itself. That timeline reflects the investigative complexity of insider trading cases and ASIC’s willingness to pursue them over long horizons.

Two enforcement proceedings emerged from the same corporate collapse, but they reached very different destinations in the same month. The timeline of both matters traces a long arc:

According to ASIC media release 26-069MR, both proceedings reached their respective milestones within weeks of each other.

ASIC media release 26-069MR confirms the precise dates of Evans’s guilty plea and provides the official record of both enforcement proceedings stemming from the Big Un collapse, including the charges originally filed against Corner in April 2023.

Corner’s trial ran for approximately five weeks before the jury was unable to reach a verdict. The hung jury, delivered on 30 March 2026, meant that the former CFO was neither convicted nor acquitted. The matter was listed for further mention on 20 April 2026.

As of 1 June 2026, no retrial decision had been announced publicly. The charges, relating to the alleged sale of 1.7 million shares worth more than $5 million while in possession of inside information, remain unresolved. The gap between the April 2023 charges and the 2026 trial illustrates the typical duration of white-collar criminal proceedings in Australia.

Richard Evans (formerly known as Richard Evertz), the former CEO, entered a guilty plea to one charge of communicating inside information on approximately 9-10 April 2026. The trial that had been scheduled against him was vacated following the plea.

A sentencing hearing has been set for 21 August 2026. The outcome of that hearing will determine the penalty for what is now a confirmed criminal conviction.

The Evans sentencing hearing on 21 August 2026 will add another data point to the developing picture of insider trading penalties in Australia, where the Full Federal Court has confirmed that general deterrence is the dominant sentencing consideration and that custodial terms remain available even after appellate reduction.

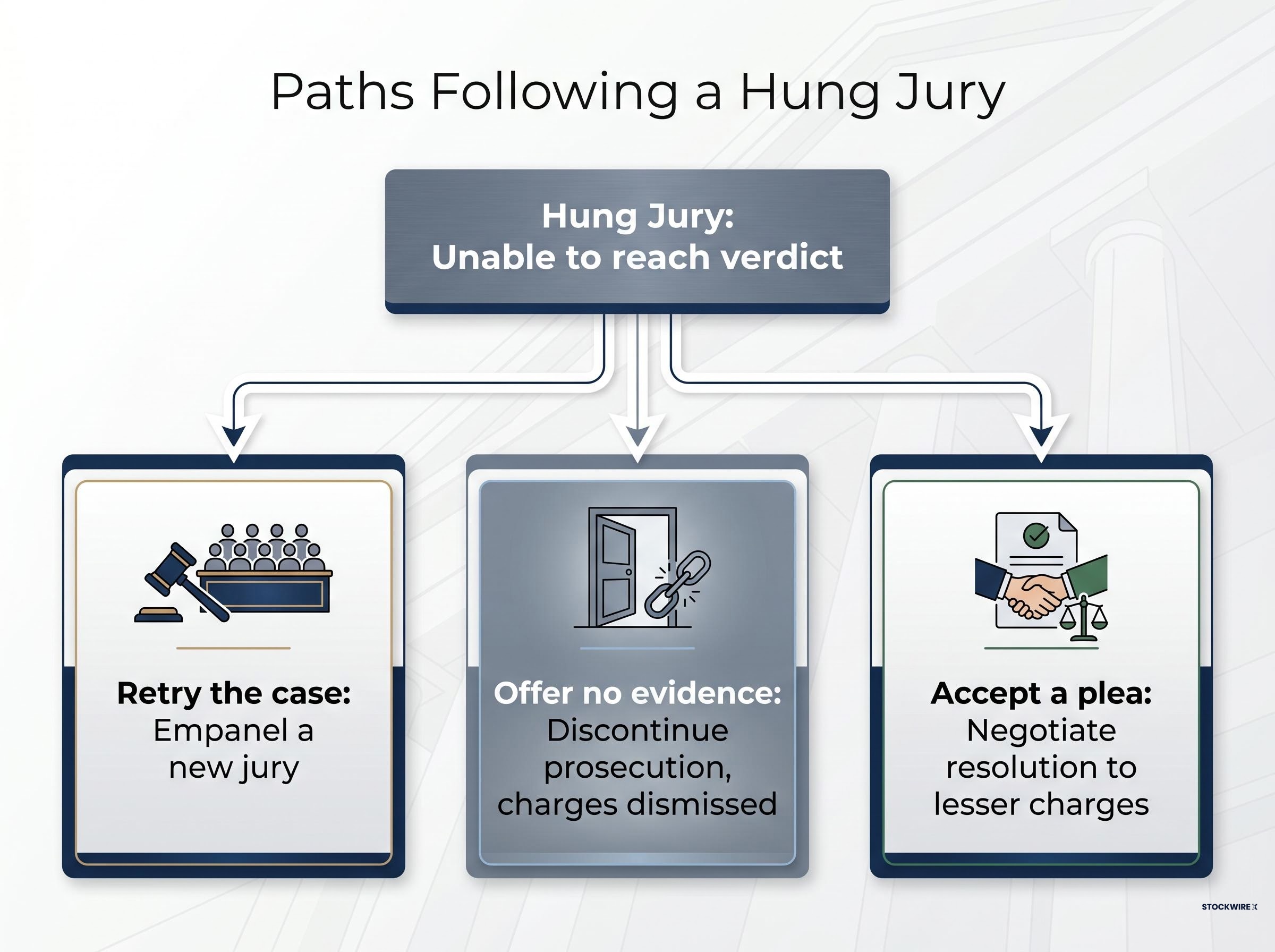

A hung jury is not an acquittal. That distinction matters.

A hung jury means the jury was unable to reach the required verdict, either guilty or not guilty. The defendant is neither convicted nor cleared. The charges remain on foot.

Under NSW criminal procedure, when a jury cannot reach a unanimous (or otherwise required) verdict, the trial concludes without a determination of guilt or innocence. The judge discharges the jury, and the matter returns to the prosecution for a decision on next steps.

That decision turns on a prosecutorial assessment of the public interest. The prosecution considers factors such as the strength of the remaining evidence, the cost and burden of a second trial, and whether a retrial is likely to produce a different outcome. The three possible paths following a hung jury are:

In the Corner matter, the case was listed for further mention on 20 April 2026. No public announcement on which path ASIC intends to take had been made as of 1 June 2026. The hung jury preserves the status quo: the charges are unresolved, and the prosecution’s options remain open.

The specifics of the Big Un collapse point toward structural conditions that investors and compliance professionals encounter repeatedly in the small-cap technology segment of the ASX.

Several governance risk indicators are visible in the Big Un pattern:

Small-cap technology stocks on the ASX are particularly exposed to insider trading risk because the information gap between insiders and the market tends to be wider when coverage is sparse and disclosure norms are less institutionalised than in large-cap equivalents. When a company’s senior leadership holds information that would materially affect the share price, and external oversight is limited, the conditions for insider trading risk are structurally elevated.

The enforcement timeline itself carries a signal. The alleged conduct occurred during Big Un’s operational period. The company collapsed in 2018. ASIC filed charges in 2023. The trial concluded in 2026. Approximately eight years separated the conduct period from the trial outcomes, a span that illustrates ASIC’s capacity to pursue white-collar matters long after the company in question has ceased to exist.

ASIC’s enforcement priorities for 2025 and 2026 explicitly name insider trading, and the regulator established a dedicated insider trading team in late September 2024, a structural investment that signals the Big Un proceedings are part of a broader, sustained campaign rather than an isolated response to a single collapse.

The Big Un Limited case is not finished. Evans has pleaded guilty and awaits sentencing on 21 August 2026. Corner’s case remains unresolved, pending a prosecutorial decision on whether to pursue a retrial.

Two questions will determine the case’s final shape:

The company itself entered liquidation in 2018 and remains in that state. The enforcement consequences have now outlasted the company by nearly a decade, a reminder that corporate governance failures at the executive level can generate legal proceedings that persist long after the entity itself has disappeared from the ASX.

The Big Un proceedings sit alongside a broader pattern in Australian corporate enforcement where executive liability for compliance failures is being defined case by case, with courts and regulators drawing increasingly precise lines between what executives knew, what they disclosed, and what they should have escalated.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Big Un Limited was an ASX-listed small-cap technology company that was regarded as a standout performer through 2017 before its shares were suspended in February 2018 following disclosures related to its funding arrangements. The company was delisted from the ASX and entered liquidation in August 2018, remaining in that state as of the latest available information.

A hung jury means the jury was unable to reach the required verdict, so the defendant is neither convicted nor acquitted and the charges remain on foot. Following a hung jury, the prosecution can choose to retry the case, offer no evidence and effectively discontinue the charges, or negotiate a plea to lesser charges.

ASIC charged former CFO Andrew Corner in April 2023 with insider trading, alleging he sold 1.7 million Big Un shares worth more than $5 million while in possession of inside information. Former CEO Richard Evans (also known as Richard Evertz) pleaded guilty in April 2026 to one charge of communicating inside information, with a sentencing hearing scheduled for 21 August 2026.

Trading on inside information involves a person who holds material non-public information personally buying or selling the relevant securities. Communicating inside information involves disclosing that material non-public information to another person who may then trade on it; both forms of conduct are prohibited under section 1043A of the Corporations Act.

The Big Un case illustrates that ASIC can and does pursue white-collar matters over very long timeframes; the alleged conduct occurred during the company's operational period, the company collapsed in 2018, ASIC filed charges in 2023, and the trial outcomes arrived in 2026, spanning approximately eight years from the conduct period to resolution.