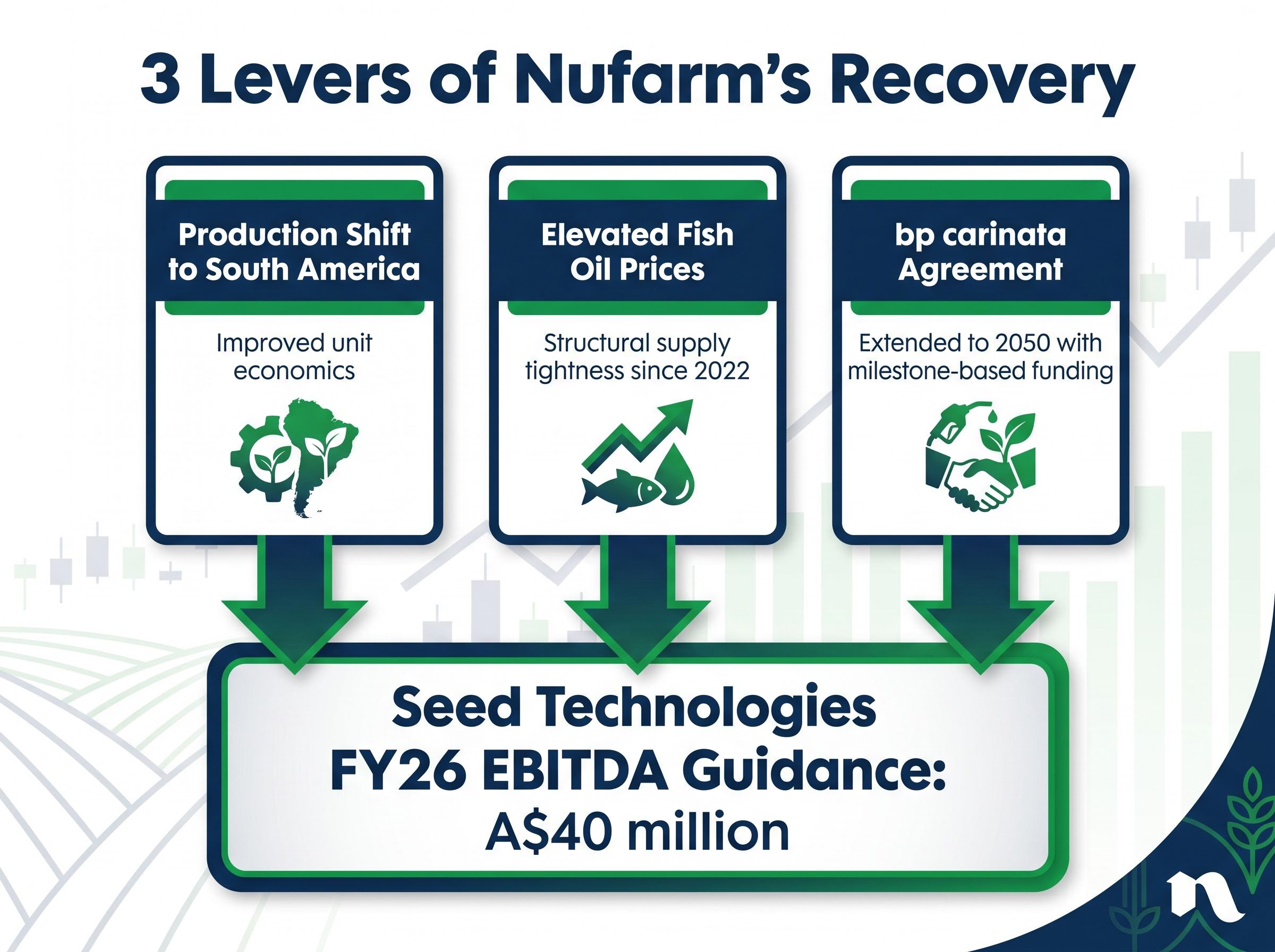

Twelve months ago, Nufarm’s Omega-3 canola programme triggered one of the most severe single-session share price collapses in the company’s recent history, erasing roughly 30% of its market value in a single day. The programme that caused the damage now sits at the centre of a Seed Technologies EBITDA guidance upgrade from A$30 million to A$40 million for FY26, announced alongside the HY26 results on 27 May 2026. The reversal is not accidental: a production geography shift, a structurally tighter fish oil market, and an expanded commercial agreement with bp carinata have each contributed to stabilising what was once the company’s most visible liability.

This analysis traces the mechanics of that turnaround, quantifies the earnings trajectory it has produced, examines the valuation discount that still separates Nufarm from global agrochemical peers, and frames the 2028 regulatory deregulation timeline in Europe and China as the next potential rerating catalyst for investors assessing whether the recovery has further to run.

What broke Nufarm’s share price and what the A$28 million writedown actually revealed

The damage was immediate and severe. Nufarm shares fell approximately 30% in a single session after management withdrew Omega-3 canola revenue targets, a disclosure that forced the market to reprice the entire Seed Technologies segment in one afternoon.

The accounting entry that followed told investors what had gone wrong operationally. Management recorded an A$28 million inventory writedown in the prior interim result, representing unsaleable or stranded Omega-3 canola inventory that could not be commercialised at the volumes or prices originally projected.

The A$28 million inventory writedown was not a write-off of the Omega-3 programme’s science or intellectual property. It was a writedown of physical inventory that could not be sold, a production and commercialisation failure rather than a scientific one.

That distinction matters for anyone assessing the recovery. The underlying technology, a genetically modified canola plant capable of producing long-chain Omega-3 fatty acids, was never in question. What broke was the execution chain: production economics, commercial readiness, and inventory management. The credibility collapse was severe, but the bar for recovery was operational, not structural. Management needed to demonstrate that the programme could produce and sell at commercially viable economics, not that the science worked. That reframing is where the recovery thesis begins.

The mechanics of inventory writedown and turnaround sequencing follow a recognisable pattern across ASX-listed food and agri businesses: the accounting charge crystallises the prior execution failure, a phased operational reset follows, and the market withholds a valuation rerating until at least two or three reporting periods confirm the new trajectory, a dynamic visible in Synlait Milk’s three-stage recovery roadmap after its own $80.6 million loss and $472 million debt position.

When big ASX news breaks, our subscribers know first

The mechanics of the recovery: South America, fish oil prices, and bp carinata

The first lever was geographic. Nufarm shifted Omega-3 canola production operations to South America, a move that addressed the production cost and agronomic challenges that had undermined the programme’s prior economics. South American growing conditions and cost structures improved the unit economics sufficiently to narrow the programme’s losses, a necessary precondition before any revenue recovery could be credible.

The second lever was external. Fish oil prices have been elevated and structurally tight since 2022, driven by Peruvian anchovy quota cuts and sustained aquaculture demand. According to public commentary from IFFO (The Marine Ingredients Organisation), global fish oil supply has remained constrained, with projected 2025 production of approximately 1.2-1.3 million tonnes. When the price of wild-caught fish oil rises, the competitive economics of a land-based, plant-derived Omega-3 substitute improve proportionally. Nufarm did not create this tailwind, but the programme is positioned to capture it.

IFFO global fish oil production data published in November 2025 projects 2025 output at approximately 1.2-1.3 million tonnes, with Peru’s declining anchovy yields identified as a primary contributor to the structural tightness that has kept prices elevated since 2022.

The third lever was contractual.

The bp carinata agreement and what a 2050 horizon means commercially

Nufarm’s expanded agreement with bp carinata, disclosed in the HY26 ASX release, extends the partnership to 2050 with milestone-based funding. In practical terms, milestone-based funding means that payments are tied to specific production or commercialisation achievements rather than a flat offtake price, reducing bp’s capital exposure while aligning both parties’ incentives around delivery.

The 2050 extension transforms what was previously a trial-phase arrangement into a long-duration commercial partnership. For analysts modelling the Seed Technologies segment, a 2050 horizon provides a revenue floor that can be projected across decades rather than quarters, a material change in how the segment’s forward contribution is valued.

The HY26 materials confirm an expected A$40 million improvement in EBITDA from Emerging Platforms (carinata and Omega-3 reset combined), underpinning the upgraded Seed Technologies segment guidance. The three recovery levers in summary:

- Production geography shift to South America: Improved unit economics and resolved prior agronomic constraints

- Elevated fish oil prices: Structural supply tightness since 2022 strengthened the competitive position of a plant-derived alternative

- bp carinata agreement extended to 2050: Milestone-based funding and long-duration offtake commitment established a modellable revenue floor

Each lever operates independently. The recovery does not depend on any single factor holding, and the convergence of all three simultaneously is what underpins the confidence embedded in the upgraded guidance.

Why Omega-3 canola exists and what it is trying to replace

Long-chain Omega-3 fatty acids, specifically DHA and EPA, are compounds required for human brain function, cardiovascular health, and as a feed ingredient in aquaculture (fish farming). The primary commercial source of DHA and EPA is fish oil, extracted from wild-caught fish, predominantly anchovies harvested off the coast of Peru.

The problem is supply. There is a ceiling on how much fish oil the world’s oceans can sustainably produce. Peruvian anchovy quotas have been cut repeatedly in response to stock depletion concerns, and the fishing regulation environment continues to tighten. At the same time, global aquaculture production continues to grow, creating persistent demand pressure on a supply base that cannot expand.

| Supply Constraints | Demand Drivers |

|---|---|

| Peruvian anchovy quota cuts | Aquaculture feed demand growth |

| Fishing regulation tightening globally | Human nutrition and supplement markets |

| Finite marine biomass harvesting capacity | Food ingredient demand in processed foods |

Nufarm’s Omega-3 canola is a genetically modified canola plant engineered to produce DHA and EPA in its seeds, offering a land-based alternative to a marine resource that is structurally constrained. The programme is not a speculative bet on a niche ingredient; it is positioned into a measurable and widening supply gap. When fish oil prices are high, as they have been since 2022, the economic case for a plant-derived substitute strengthens. An investor who understands this structural context can assess the programme’s long-term optionality independently of near-term quarterly earnings.

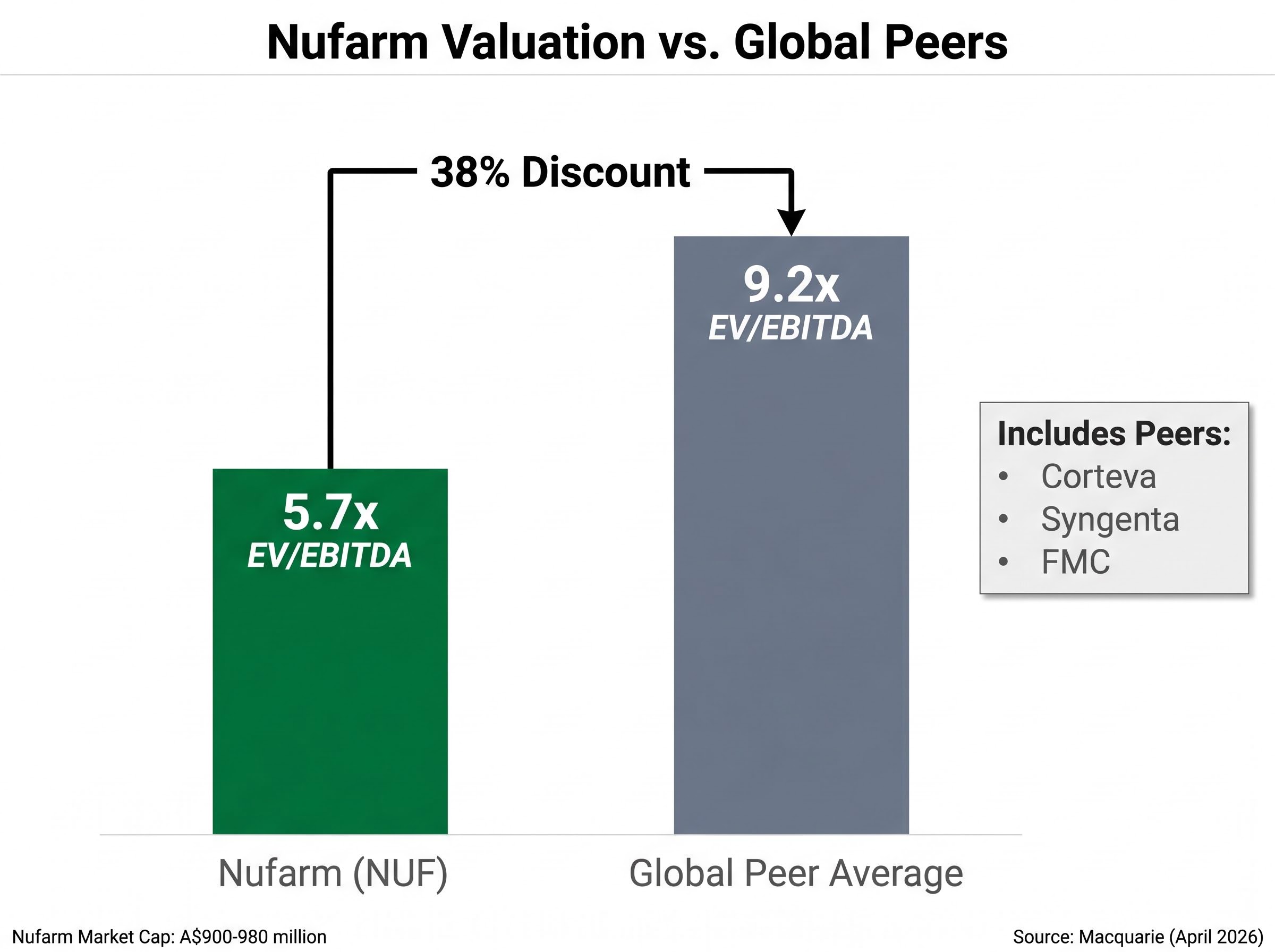

The valuation discount and what an earnings inflection point could mean for NUF

According to a Macquarie analyst note from April 2026, Nufarm trades at an EV/EBITDA multiple of 5.7x, against a global agrochemical peer average of 9.2x. That is a 38% discount.

Nufarm EV/EBITDA: 5.7x vs. global peer average: 9.2x (Macquarie, April 2026)

Named global peers in the agrochemical space, including Corteva, Syngenta, and FMC, typically trade at premiums that reflect more diversified and stable earnings profiles. Nufarm’s discount is not simply a market oversight. It reflects accumulated execution risk, most visibly from the Omega-3 programme collapse, and the company must sustain consistent delivery across multiple reporting periods to earn a rerating. Analysts covering the stock have noted this explicitly.

The question for Australian investors is whether the earnings inflection now visible in FY26 can begin to close that gap. The convergence of the Seed Technologies upgrade, a cost reduction programme on track (with the initial A$50 million tranche delivering as expected), and confirmed Crop Protection margin improvement means FY26 is the first year where multiple segments are simultaneously moving in the right direction.

ASX agribusiness share price reactions to operational results have repeatedly shown that headline revenue and EBIT growth can coexist with severe single-session falls when per-share earnings disappoint, as Elders demonstrated in H1 FY26 when a 32% revenue rise and 33% EBIT expansion still produced a 21% share price decline on results day.

| Metric | Nufarm (NUF) | Global Peer Average |

|---|---|---|

| EV/EBITDA multiple | 5.7x | 9.2x |

| Approximate market cap | A$900-980 million | Varies by peer |

| Seed Technologies FY26 EBITDA guidance | A$40 million | N/A |

The share price traded in the range of approximately A$2.42-A$2.56 in late May 2026. Whether the discount narrows depends less on the guidance numbers themselves, which are now public, and more on whether management can deliver against them consistently. A single upgraded half-year does not erase years of execution doubt; sustained delivery across FY27 and beyond is the test that analysts and institutional investors will apply.

The 2028 regulatory timeline and the size of the prize if Europe and China approve

Management has targeted 2028 for regulatory deregulation of Omega-3 canola in both Europe and China. If achieved, approval in each market would unlock commercial access for a non-fish-derived Omega-3 source across food ingredients, dietary supplements, and aquaculture feed products, markets where the structural fish oil supply gap is most acute.

The regulatory uncertainty, however, is genuine. No public 2025 or 2026 document from EFSA (European Food Safety Authority), the European Commission, or China’s MARA/MOA specifically advancing Omega-3 canola approval has been located. The 2028 timeline remains management’s internal target rather than a confirmed regulatory milestone.

The EFSA GMO application procedure requires applicants to pass a completeness check, a six-month scientific risk assessment, and a post-adoption phase before the European Commission can issue a formal approval decision, a multi-step timeline that explains why the 2028 target remains contingent on dossier submission occurring well in advance.

For an investor pricing in the optionality, the sequential milestones required before the 2028 scenario can be evaluated are:

- Regulatory submission or dossier acceptance by the relevant authority

- Scientific opinion or safety assessment (EFSA in Europe, biosafety review in China)

- Formal approval decision by the European Commission or MARA

- Commercial scale-up readiness to supply approved markets at volume

The combined European and Chinese aquaculture and food ingredient markets represent significant addressable demand for a plant-derived Omega-3 source. If the approvals materialise, the programme’s commercial scope expands from early-stage trials to full-scale ingredient deployment in two of the world’s largest consumer markets. If they do not, the base case earnings recovery still stands on the operational improvements already delivered in Seed Technologies and the broader cost programme.

These statements regarding the 2028 regulatory timeline are speculative and subject to change based on regulatory developments and company performance.

Nufarm’s recovery is real, but the re-rating still has conditions attached

The three threads of Nufarm’s recovery story are now quantified in the guidance: the Omega-3 operational turnaround, the Seed Technologies EBITDA upgrade to A$40 million for FY26, and the cost reduction programme executing on schedule. The HY26 results confirmed that each thread is contributing simultaneously, a first for the company in several reporting periods.

The conditions for the valuation discount to close materially remain specific and testable:

- Consistent earnings delivery across at least two more reporting periods, demonstrating that FY26 is a trajectory rather than a one-off

- Confirmed regulatory progress toward the 2028 European and Chinese deregulation targets, with visible submission or assessment milestones

- Sustained fish oil price support for the Omega-3 programme’s competitive position relative to marine-derived alternatives

- Second cost tranche execution, with the additional A$50 million run-rate savings targeted for completion by end of FY27 and full benefit expected in FY28

UBS and RBC Capital Markets are among the brokers actively covering Nufarm, though specific 2026 price targets are not available on the open web. The recovery thesis is coherent, and the evidence is now embedded in upgraded guidance. But the 38% valuation discount to global peers reflects real historical execution risk, and re-rating requires sustained delivery that has not yet been demonstrated across multiple cycles. FY27 and FY28 are the years when the second cost tranche delivers and the 2028 regulatory calendar either advances or stalls.

For investors wanting to model what a rerating might require across multiple macro environments, our full explainer on the conditions for a valuation discount to close examines how execution consistency, earnings guidance delivery, and macro risk resolution have historically interacted across equities trading at historically wide discounts to fair value, with worked analysis of the specific variables that have preceded sustainable gap closures.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.