Two company-specific events landed on 27 May 2026 inside a sector that, by most conventional readings of the macro backdrop, should have offered investors a quieter session. The Federal Court of Australia ordered Westpac Banking Corporation to pay a $26 million civil penalty for systemic hardship failures spanning nearly six years. Separately, ASX Ltd. continued a severe multi-day sell-off triggered by a shock capital expenditure upgrade disclosed the previous day. Both events hit the ASX Financials sector, the largest sector by weight in the S&P/ASX 200, at a moment when bond yield movements consistent with easing credit stress would ordinarily have provided a constructive backdrop for bank earnings and credit growth. The gap between what macro conditions implied and what the sector actually delivered is the analytical engine of this piece. What follows is a breakdown of the two confirmed events, the concept of sector-level divergence, and what the pattern may signal for observers of Australian financial markets.

What the Federal Court found against Westpac, and why the $26 million figure understates the significance

The headline number is $26 million. The finding behind it carries considerably more weight.

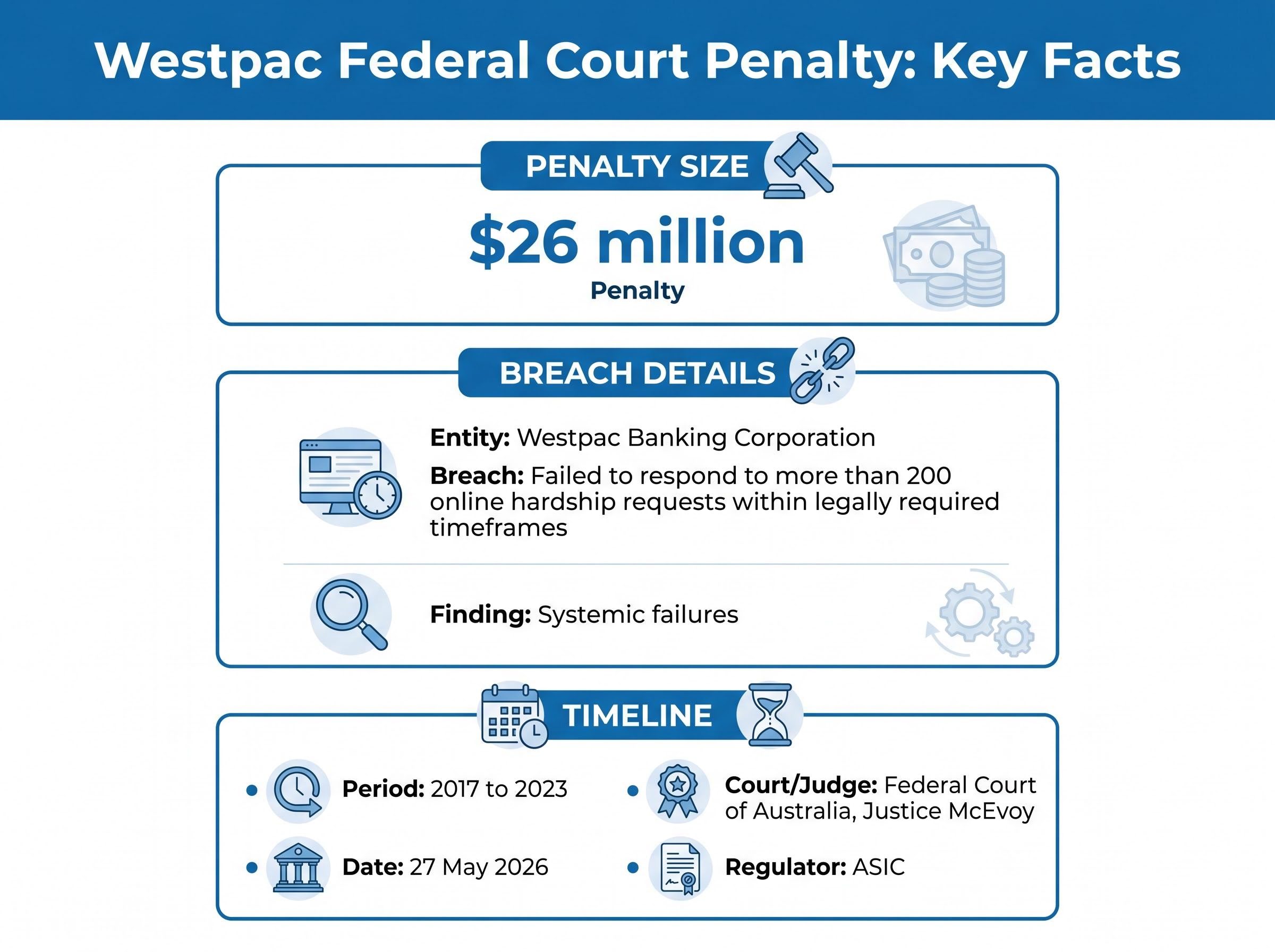

On 27 May 2026, Justice McEvoy of the Federal Court of Australia ordered Westpac to pay the penalty in proceedings brought by the Australian Securities and Investments Commission (ASIC), as detailed in ASIC media release 26-107MR. The core facts are straightforward:

The ASIC media release 26-107MR confirms that Justice McEvoy characterised the conduct as systemic across the full period under review, a description that carries specific legal weight distinct from findings of isolated or administrative non-compliance.

- Penalty: $26 million civil penalty ordered by the Federal Court

- Breach: Westpac failed to respond to more than 200 online hardship requests within legally required timeframes

- Conduct period: 2017 to 2023, spanning approximately six years

- Court finding: Systemic failures in complying with financial hardship obligations

- Bank response: Westpac apologised and committed to implementing reforms

The court characterised Westpac’s conduct as “systemic failures” in its hardship obligations, a phrase that distinguishes this from an isolated compliance lapse and places the finding in the category of institutional failure.

That language is where the analytical weight sits. A one-off processing error carries a fine and a news cycle. A finding of systemic failure across nearly six years carries reputational and operational cost implications that extend well beyond the penalty itself. For investors assessing whether the $26 million represents closure or a continuing overhang, the distinction between “isolated” and “systemic” is the one that matters.

The customers affected by Westpac’s failures to meet its financial hardship obligations included domestic abuse survivors, natural disaster victims, and seriously ill individuals, a population profile that shaped the court’s characterisation of the conduct as grossly negligent rather than merely procedurally deficient.

When big ASX news breaks, our subscribers know first

ASX Ltd.’s capex shock and what a multi-day collapse says about market conviction

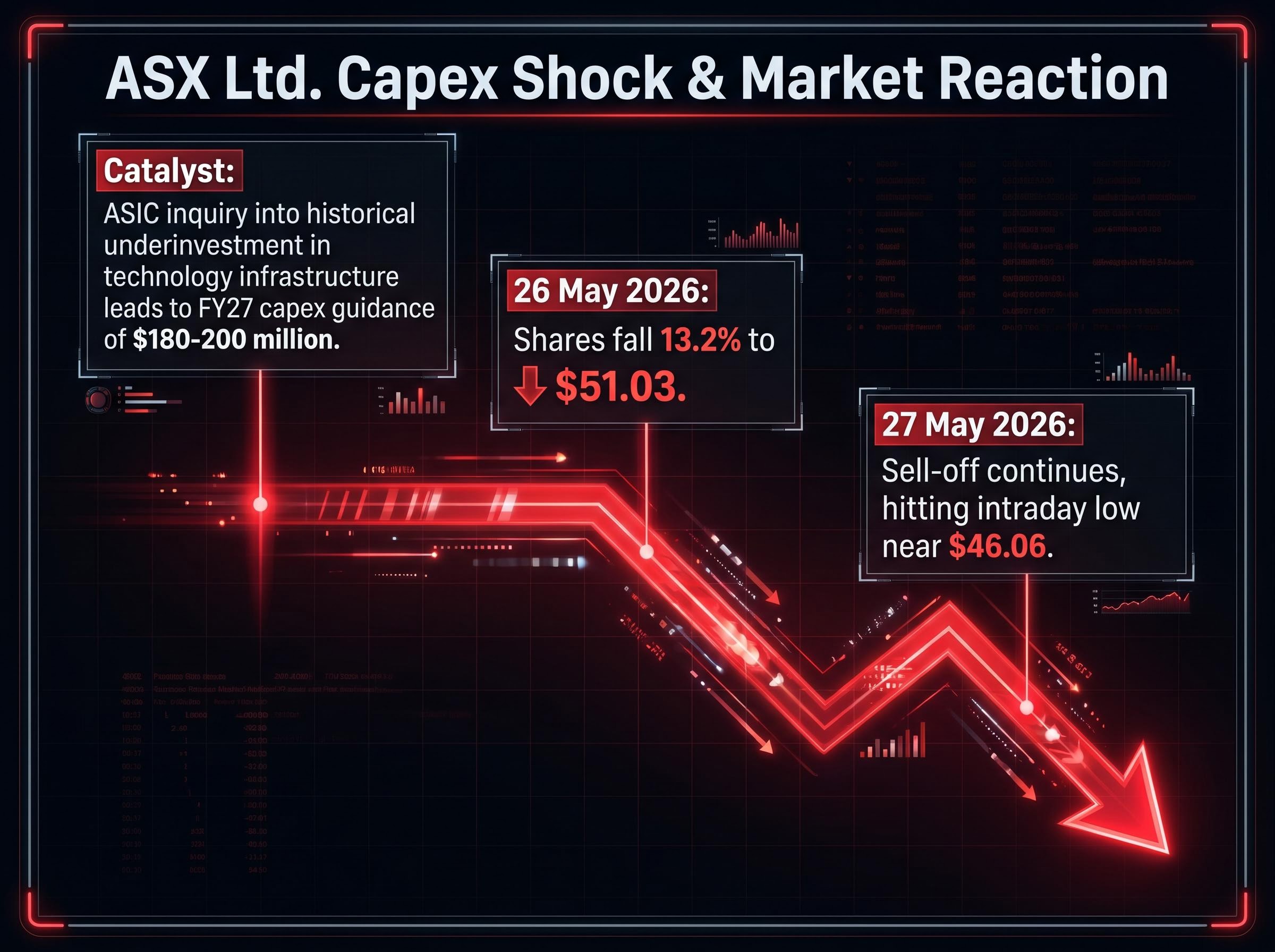

The sell-off in ASX Ltd. (ASX: ASX) began on 26 May 2026, when the company’s trading update disclosed higher FY27 capital expenditure guidance, reported at approximately $180-200 million. The revision was attributed to technology cost inflation and product development needs, following an ASIC inquiry into historical underinvestment in the exchange’s technology infrastructure.

The market’s response was immediate. On 26 May, ASX Ltd. shares fell approximately 13.2% to around $51.03, according to market data (though this figure has not been independently confirmed via a named primary source). Selling pressure continued into 27 May, with an intraday low near $46.06 reported in subsequent sessions.

A single-day decline of that magnitude in a name of this profile is not a reaction to a headline. It is a repricing of a structural cost story.

The 13.2% decline on 26 May 2026 was reportedly ASX Ltd.’s record single-day loss, and the cost structure behind it is not a short cycle: FY28 capex guidance was simultaneously set at $170-190 million, signalling that elevated spending extends well beyond the current financial year.

Why the ASIC inquiry matters to the capex story

The capex revision did not arrive in isolation. The sequence that made it so damaging to investor confidence follows a clear logic chain:

- ASIC conducted an inquiry into ASX Ltd.’s historical underinvestment in technology infrastructure

- The inquiry’s findings created a regulatory backdrop in which the company could not defer spending further

- The resulting capex guidance revision forced investors to reprice earnings expectations against a structurally higher cost base

Without the ASIC inquiry, a capex upgrade of this size might have been absorbed as a growth investment. With the inquiry as context, the market read it as catch-up spending on deferred obligations, a cost that delivers no new revenue but compresses margins. That reading explains why selling persisted across multiple sessions rather than stabilising after the initial shock.

ASX Ltd. is the operator of Australia’s primary exchange infrastructure. A collapse of this scale in this name carries sector-level symbolism that extends beyond its index weighting.

When supportive macro conditions fail to lift a sector: an explainer on divergence signals

The conventional expectation is intuitive. When long-term bond yields decline, credit stress signals ease, loan demand can improve, and bank earnings benefit from a more supportive funding environment. In late May 2026, Australian 10-year government bond yields sat near 4.86% (based on broader market data, though no named primary source has confirmed the precise figure for 27 May 2026). That level, and the direction of recent movement, would ordinarily provide a constructive backdrop for financial sector performance.

The Financials sector did not respond accordingly.

When a sector fails to respond to macro conditions that should theoretically support it, that non-response itself becomes an informational signal for market observers.

This is the concept of sector-level divergence. The table below illustrates the framework:

Sector-level stress signals had been accumulating across the ASX 200 before 27 May, with 22 index constituents hitting 52-week lows in the week ending 1 May 2026 even as the headline index fell just 0.65%, a divergence between surface calm and underlying breadth deterioration that the Financials sector’s behaviour on 27 May extended rather than initiated.

| Macro Signal | Expected Sector Reaction | What Happened on 27 May 2026 |

|---|---|---|

| Bond yields consistent with easing credit stress | Support for bank earnings and loan demand | Stock-specific drags from Westpac penalty and ASX Ltd. sell-off appeared to weigh on the sector despite the supportive yield environment |

| Yield curve dynamics supportive of net interest margins | Positive for bank profitability outlook | Institutional selling pressure linked to company-specific events may have overwhelmed the macro tailwind |

The fund flows interpretation explains the mechanics. Institutional money that is already underweight or actively selling a sector can overwhelm macro tailwinds, producing flat or negative sector performance even when the backdrop is positive. This “macro-positive, stock-specific-negative” pattern is a recognised dynamic in sector analysis, and it provides a reusable lens for interpreting future sessions where a sector’s performance appears to contradict the prevailing conditions.

The broader broker action landscape and what selective upgrades reveal

A comprehensive picture of broker actions across the major Australian banks on 27 May 2026 is not available from named primary sources. No dated broker round-ups in major financial publications documented rating changes, upgrades, downgrades, or fresh price targets for Commonwealth Bank of Australia, National Australia Bank, ANZ, or Westpac on that date.

The verification status of broader broker activity on the day is worth stating plainly:

- Confirmed: Westpac Federal Court penalty; ASX Ltd. capex-driven sell-off

- Not confirmed from named primary sources: Broker rating actions on major banks; reported upgrades of Fisher & Paykel Healthcare; reported initiation of Goodman Group coverage

- Not found: CLSA downgrade of ASX Ltd. referenced in some market commentary

How to read selective conviction in a negative sector session

The absence of confirmed broker activity on the major banks does not mean no broker activity occurred elsewhere. On days when major sector names face headwinds, where brokers choose to signal conviction in adjacent or non-correlated names reveals where institutional confidence may be migrating.

This matters for readers assessing whole-market sentiment. A negative session for the Financials sector does not necessarily translate to uniformly bearish positioning across the market. Understanding that distinction helps avoid the cognitive error of reading one sector’s weakness as a signal about the broader direction of the S&P/ASX 200.

The next major ASX story will hit our subscribers first

Two events, one sector, and what the day’s pattern means for how investors read Financials going forward

The coincidence of timing amplifies the signal. A $26 million penalty for systemic hardship failures at Westpac and a multi-day, double-digit percentage collapse in ASX Ltd. shares are each individually material. Arriving on the same day, inside the same sector, they produce a combined weight on sentiment that exceeds what either event would generate alone.

The implication for how market observers weigh company-specific risk against macro conditions is direct. When two of the sector’s prominent names face simultaneous headwinds, the macro backdrop, however constructive, struggles to offset the drag. The Financials sector’s weight in the S&P/ASX 200 means this is not a contained problem; it has index-level implications.

If the Financials sector repeatedly fails to respond to supportive macro conditions, that pattern, should it persist, becomes a weight on sentiment that is harder to reverse than any single negative headline.

Whether the sector recovers from this session will depend less on bond yields or credit conditions and more on whether ASX Ltd. and Westpac can credibly address the structural issues their disclosures have surfaced. Westpac’s commitment to reform and ASX Ltd.’s technology investment programme are the starting points for any recovery narrative; the market will assess execution, not intention.

Investors wanting to separate the penalty’s financial materiality from its market signal will find our deep-dive into the Westpac share price reaction, which weighs the $26 million figure against Westpac’s $3.4 billion first-half profit, examines the 1H26 mortgage delinquency trend, and assesses whether the gross negligence classification changes the forward risk profile for holders.

The story the numbers tell about Australia’s financial sector in late May 2026

Company-specific events of sufficient severity can neutralise macro tailwinds at the sector level. 27 May 2026 provides a clear case study: the Westpac penalty and ASX Ltd.’s capex-driven sell-off each carried enough weight to offset conditions that would ordinarily have supported financial sector performance.

The evidence base should be read honestly. Two confirmed events anchor this analysis. Broader characterisations of sector performance, bond yield levels, and broker actions remain less fully verified and should be treated with appropriate caution.

The forward question is whether the Financials sector’s response to supportive macro conditions normalises in the sessions ahead, or whether the structural issues surfaced by these disclosures continue to weigh on investor positioning. Readers tracking Australian equities may find value in monitoring related coverage of the Westpac penalty proceedings, ASX Ltd.’s technology investment commitments, and the broader Reserve Bank of Australia and bond yield context shaping the outlook for Australian banks.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

These statements are speculative and subject to change based on market developments and company performance. Past performance does not guarantee future results.