Vanguard VIHY Declares First Distribution at 49.49 Cents per Unit

1 hr ago

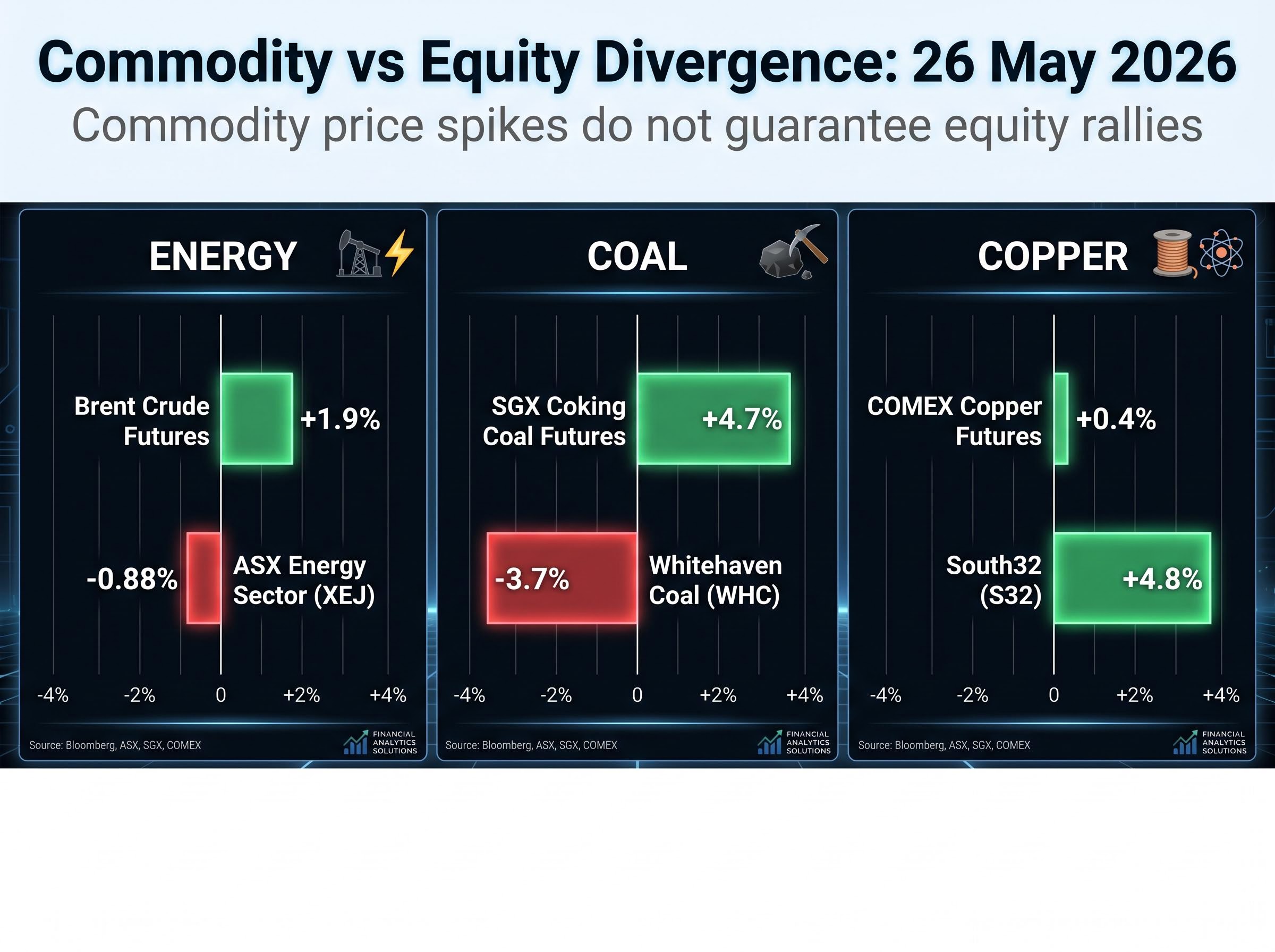

On 26 May 2026, copper stocks posted their fourth straight daily advance while energy equities fell, even as Brent crude climbed 1.9% to US$95.15 a barrel. The contradiction sat inside a single ASX session, triggered by the same geopolitical catalyst: US military strikes on Iranian missile facilities. The S&P/ASX 200 fell 34.2 points (0.39%) to 8,657.8, but within that headline decline, the Materials sector was the sole sector in the green. ASX commodity stocks were not moving as a bloc. Copper, energy, and coal each responded to the same event in structurally different ways, and the reasons behind that divergence matter for anyone holding or watching Australian resource names. What follows is a sector-by-sector breakdown of what moved, by how much, and why, finishing with a repeatable framework for reading commodity-equity divergence during Middle East tension events.

The Materials sector closed up 0.15% at 24,750.2, its fourth consecutive session of gains. No other sector finished positive.

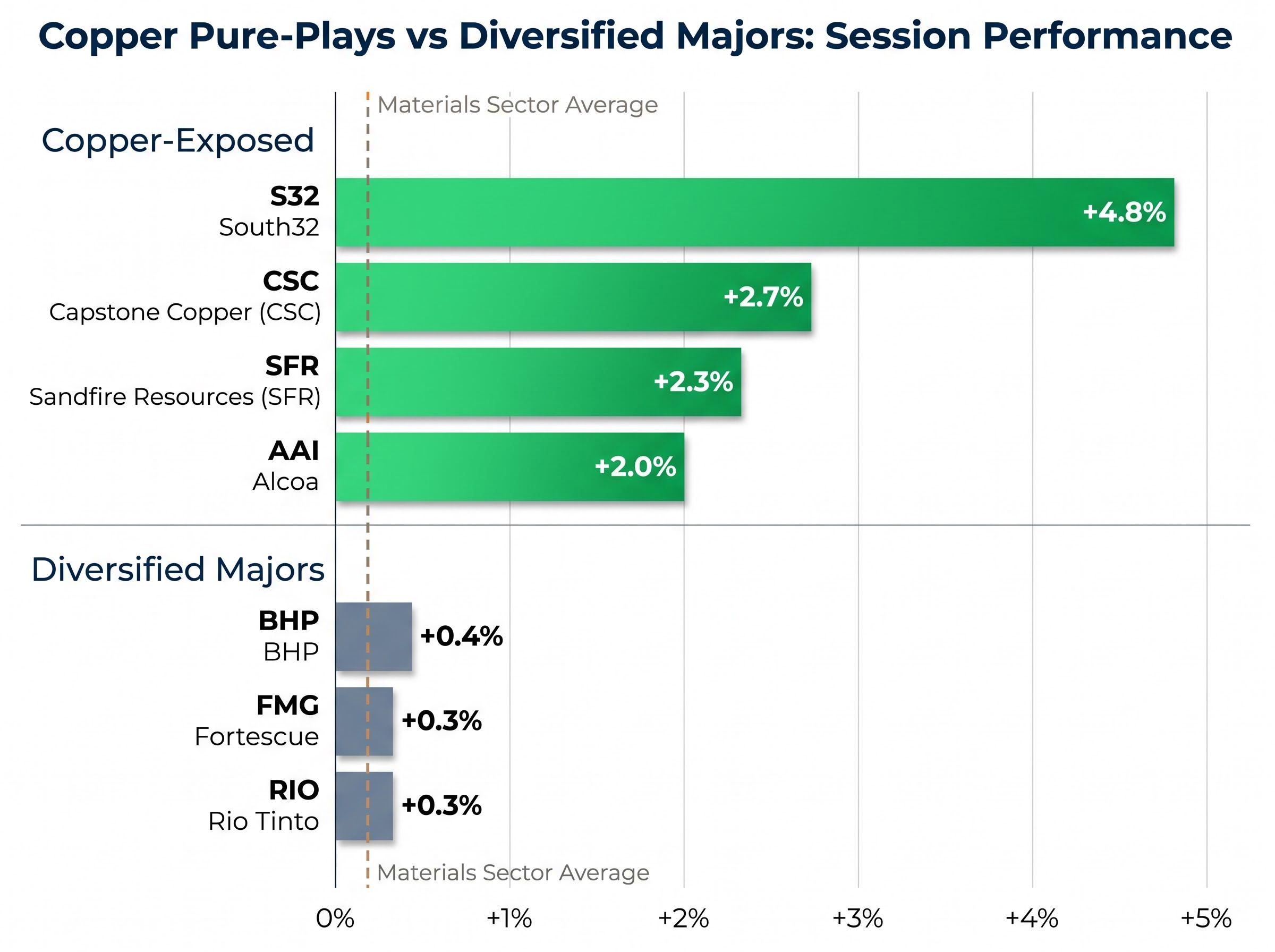

The outperformance was not broad. It was copper-specific. The gap between pure-play copper names and diversified miners told the real story.

| Company | ASX Code | Session Move (%) |

|---|---|---|

| South32 | S32 | +4.8% |

| Capstone Copper | CSC | +2.7% |

| Sandfire Resources | SFR | +2.3% |

| Alcoa | AAI | +2.0% |

| BHP | BHP | +0.4% |

| Fortescue | FMG | +0.3% |

| Rio Tinto | RIO | +0.3% |

COMEX copper futures rose 0.4% to US$6.407 per pound, providing the reference point with the London Metal Exchange closed for a UK public holiday. The copper-exposed names moved two to twelve times the magnitude of the diversified majors. This was a targeted rotation, not a broad materials bid.

SGX iron ore futures fell 1.5% to US$105.15 per tonne, yet BHP, Rio Tinto, and Fortescue each edged higher by 0.3%-0.4%. That modest positive move, against a falling underlying commodity, points toward passive index buying rather than commodity-price-led conviction, a secondary divergence worth noting inside the broader Materials outperformance.

Copper’s appeal during Strait of Hormuz disruptions rests on three structural pillars rather than a simple safe-haven reflex.

Copper is increasingly characterised as “policy-supported” while oil is seen as “policy-capped,” a distinction that determines which commodity equities attract capital during geopolitical supply shocks and which face selling pressure.

This framing explains the rotation logic: copper benefits from prolonged tension through a supply-risk premium and from swift resolution through a growth-linked demand rebound. Oil equities face a more asymmetric profile, with limited upside from price spikes due to policy caps and downside from de-escalation as risk premium unwinds. Understanding this distinction helps investors avoid treating “commodity stocks” as a single asset class.

Coal equities had their moment in the prior session. SGX Australian Premium Coking Coal futures surged 4.7% to US$247 per tonne, attributed to a Liushenyu-related supply development. On 26 May, that momentum reversed sharply:

The futures spiked. The equities sold off. The disconnect is not random.

UBS retained its Buy rating on Whitehaven with a $9.10 price target, indicating broker conviction exists even as the stock fell. Yet the selling pressure came from a different source than fundamental re-rating.

Many institutional funds carry formal mandates to reduce coal exposure over time. Price rallies accelerate exit rather than attract accumulation. Fund managers have been described as treating coal price surges during geopolitical events as “geopolitical premium” without corresponding upgrades to the long-term price decks used in valuation models.

Chinese demand and steel-cycle uncertainty cap medium-term earnings expectations regardless of spot price moves. When futures spike on temporary supply fears, equity investors discount the disruption as transient and sell into the strength rather than chase it.

ICE Brent futures rose 1.9% to US$95.15 per barrel. The Energy sector (XEJ) fell 0.88%, the steepest sectoral decline alongside Utilities (down 2.17%). The individual moves reinforced the disconnect: Santos (STO) fell 0.9%, Beach Energy (BPT) fell 1.8%, and Woodside (WDS) slipped 0.1%.

| Indicator | Session Move |

|---|---|

| ICE Brent Crude | +1.9% (US$95.15/bbl) |

| ASX Energy Sector (XEJ) | -0.88% |

| Santos (STO) | -0.9% |

| Beach Energy (BPT) | -1.8% |

| Woodside (WDS) | -0.1% |

Three structural factors explain why equities moved opposite to crude:

Santos separately flagged a $300 million capital expenditure reduction for 2027-2030, with a free cash flow break-even target of US$45-50 per barrel, evidence that operators themselves are planning conservatively at current price levels. Retail investors who buy energy stocks expecting a direct read-through from rising crude prices risk misreading how the market prices these assets.

Three sectors, three outcomes, one session. The unifying logic is that geopolitical risk premia no longer accrue uniformly to all resource equities. Capital flows most consistently toward assets that are either directly exposed to supply disruption risk (oil futures, not oil equities) or structurally supported by policy (copper). Assets in policy-capped or ESG-penalised sectors attract selling regardless of underlying commodity price moves.

| Sector | Session Direction | Key Driver |

|---|---|---|

| Copper / Materials | +0.15% (4th consecutive gain) | Transition-demand floor; supply-risk premium; policy-supported |

| Energy Equities | -0.88% | Forward curve fading; policy-cap risk; ESG selling into strength |

| Coal Equities | -1.6% to -3.7% | Institutional exit mandates; China demand uncertainty; geopolitical premium not re-rated |

Copper-exposed ASX names emerge as potential relative outperformers in both a prolonged-tension and a swift-resolution scenario, benefiting from supply-risk premium in the first and growth-demand rebound in the second.

Declining stocks outnumbered advancing ones 168 to 112 within the ASX 300, confirming that Materials outperformance was notable against a broadly negative session. The framework is not that copper is “safe” in absolute terms, but that its risk profile differs structurally from energy and coal equities when geopolitical risk premia are being distributed across commodity markets.

The 26 May session offers a repeatable mental model. When the next geopolitical headline hits commodity markets, three questions can help investors read the sector response before it plays out:

A recurring pattern sits beneath the day’s price action: futures markets price front-month supply risk, while equities price multi-year earnings expectations. These can move in opposite directions on the same day, and this is not a contradiction; it is how the market separates short-term supply disruption from long-term value.

Upcoming data releases may shift the framing:

The ASX 200 is operating within a supply zone at 8,674-8,740 and demand support at 8,262-8,379, a congested range where geopolitical headline risk can swing it in either direction. Macro data that supports or undermines the case for a rate-sensitive commodity rally will determine whether the copper rotation extends or fades.

Brent crude has already moderated from peaks above US$110-$118 per barrel during earlier tension periods toward US$94-$99 in late-May sessions, partially pricing in resolution expectations. The AUD/USD at 0.7166 (down 0.12% on 26 May) provides a secondary tailwind: a weaker Australian dollar supports Australian commodity exporters priced in US dollars.

In both a prolonged-tension and a swift-resolution scenario, copper-exposed ASX names carry a structural positioning advantage that the 26 May session made visible. The rotation into South32, Sandfire Resources, and Capstone Copper reads as a positioning choice rather than a day-trade.

| Scenario | Copper / Materials | Energy Equities | Coal Equities |

|---|---|---|---|

| Prolonged Hormuz tension | Supply-risk premium supports; transition demand intact | Crude rises but equities constrained by policy and ESG caps | Futures volatile but institutional exit pressure persists |

| Swift resolution | Growth-rebound narrative supports; risk-on bid lifts industrials | Risk premium unwinds; crude falls, equities follow | No structural re-rating catalyst; China demand remains key |

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding commodity prices, sector performance, and geopolitical outcomes are speculative and subject to change based on market developments.

Copper equities benefited from a policy-supported demand floor tied to energy-transition mandates and limited exposure to Strait of Hormuz supply disruption, while energy stocks fell because forward oil price curves faded the spike, and institutional funds used the price rally as an opportunity to reduce exposure amid ongoing decarbonisation policy risk.

Futures markets price front-month supply risk, while equities price multi-year earnings expectations; these can diverge on the same day because a short-term supply disruption does not necessarily change the long-term earnings outlook that equity valuations are based on.

Many institutional funds carry formal mandates to reduce coal exposure over time, so price rallies driven by geopolitical events are treated as exit opportunities rather than entry signals; fund managers discount the spike as transient and do not upgrade long-term price decks used in valuation models.

A weaker AUD against the US dollar acts as a secondary tailwind for Australian commodity exporters because their products are priced in US dollars, effectively boosting the Australian dollar value of their revenues without any change in the underlying commodity price.

Investors can ask whether the commodity is directly supply-disruption exposed, whether the equity faces policy-cap or ESG selling risk, and whether the demand driver is China-cycle dependent or tied to energy-transition mandates; these three filters help distinguish which sectors attract capital and which face selling pressure during Middle East tension events.