Nvidia Set to Reveal First Windows PC Processors at Computex

7 hrs ago

Wall Street initially saw a 4% revenue decline, but beneath the surface of the first-quarter 2026 earnings lies a record-breaking $9.3 billion project pipeline and the highest profit margins in the company’s history. Released on 29 April 2026, the latest financial disclosures from the defence and critical infrastructure contractor present a complex analytical challenge for investors. A single classified agreement skewed the headline sales figures, masking significant organic growth across key sectors like space, missile defence, and transportation.

A detailed Parsons stock analysis reveals the mechanics behind an unprecedented 1.4x book-to-bill ratio, demonstrating how the company continues to outpace its burn rate. Evaluating the $6.6 billion in funded commitments clarifies what the firm’s forward pipeline signals for its long-term market position. The initial market reaction often heavily weights top-line contraction when evaluating quarterly performance. However, looking deeper into the operational metrics provides a clearer picture of enterprise health and margin expansion.

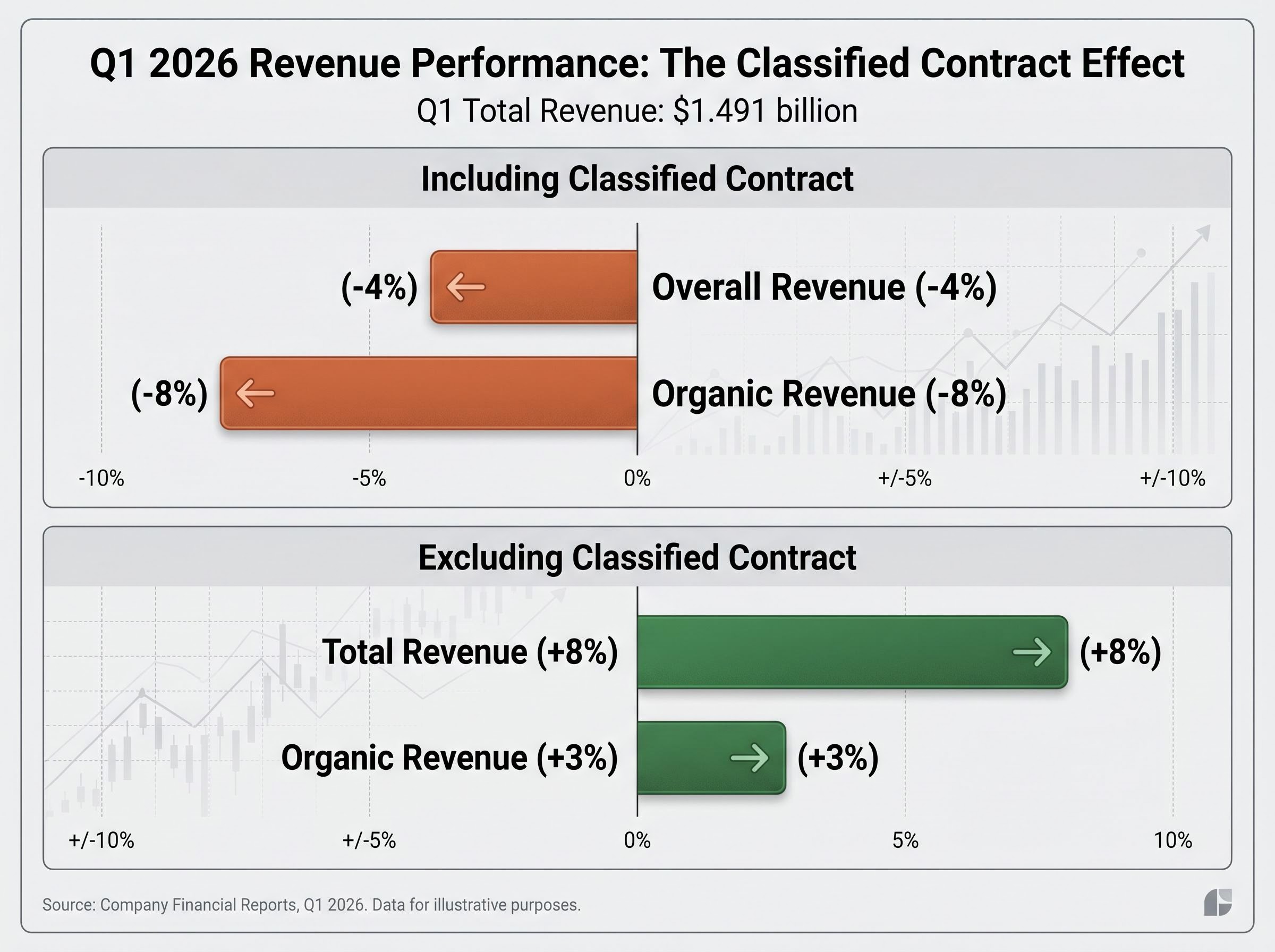

The headline figures from the first quarter present an apparent contraction that requires careful disaggregation. The company reported $1.491 billion in total revenue, representing a 4% year-over-year overall decline and an 8% organic contraction. However, these surface-level metrics reflect the distortion of a single fixed-price confidential contract rather than a broad operational slowdown.

Lower volume on this specific classified agreement temporarily compressed both operating income and overall top-line intake. Capital continues to flow toward the firm’s primary growth drivers, with transportation, space, missile defence, and critical infrastructure recording steady volume increases. These sectors represent long-term strategic priorities for federal spending, offering a more reliable growth baseline than isolated confidential projects.

Macroeconomic forecasts in Deloitte’s 2026 aerospace and defense outlook project sustained capital flows into these specific domains, reinforcing the commercial viability of contractors capable of executing complex public sector mandates.

Investors evaluating the true operational health of the business must separate the broader enterprise performance from the accounting effect of this specific classified work. The performance divergence becomes clear when comparing the metrics directly:

Overall revenue including the classified contract fell 4% year-over-year. Organic revenue including the classified contract declined 8%. Total revenue excluding the classified contract grew 8%. Organic revenue excluding the classified contract increased 3%.

This gap between the shock of a revenue miss and the underlying organic growth reveals a temporary distortion rather than a fundamental business flaw. The core operational units continue to expand their market share across strategic federal and civilian sectors.

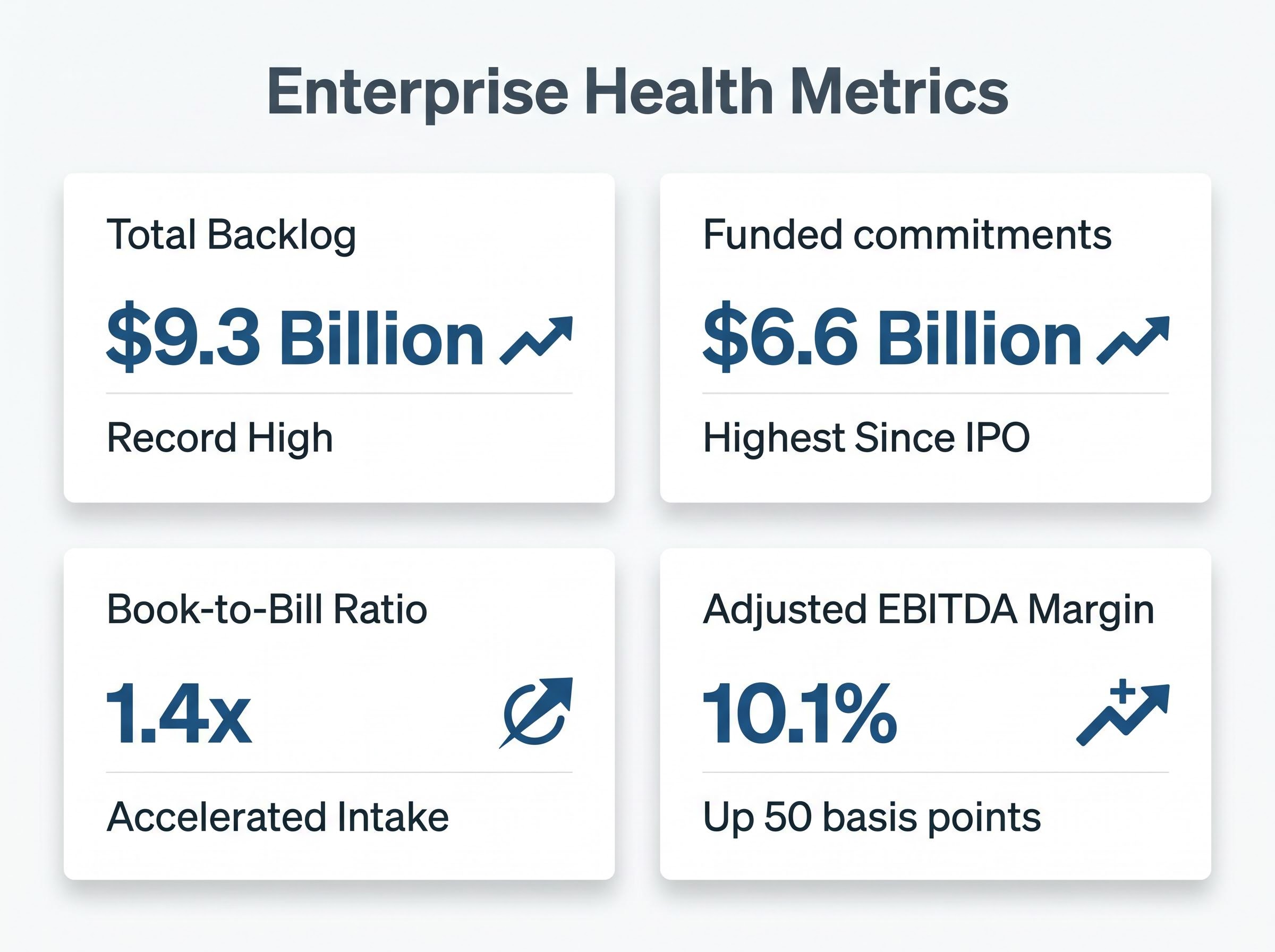

The contraction in immediate revenue pairs directly with an aggressive contract acquisition velocity that secures future cash flows. Management secured $2.1 billion in new first-quarter bookings, pushing the total backlog to a record $9.3 billion. This intake rate supports a multiple of 1.4x book-to-bill, demonstrating that the firm is capturing new work significantly faster than it burns through existing obligations.

A massive backlog provides limited value without execution security, making the composition of these awards highly material to investors. The first-quarter bookings maintain a deliberate balance across both the Federal Solutions and Critical Infrastructure segments. Four single-award contracts, each exceeding $100 million, anchor this pipeline and validate the company’s ability to win large-scale government mandates.

The formal announcement of the Federal Aviation Administration contract extension highlights this procurement momentum, securing a multi-year commitment that immediately strengthens the predictability of the federal solutions segment.

| Project Name | Segment | Total Value | Q1 Booked Value |

|---|---|---|---|

| FAA TSSC 5 Extension | Federal Solutions | $593 million | $410 million |

| U.S. Cyber Command Joint Cyber Hunt Kit | Federal Solutions | $500 million | $250 million |

| Middle East Transportation Project | Critical Infrastructure | >$340 million | >$300 million |

| GARDEM Task Orders | Federal Solutions | >$145 million | $38 million |

The aggressive acquisition strategy extended immediately past the close of the first quarter, proving that the bidding apparatus remains highly active. Forward-looking wins secured after the reporting period validate the ongoing momentum of the pipeline.

Management secured $400 million in Other Transaction Agreements alongside a separate $184 million classified indefinite-delivery/indefinite-quantity contract. These subsequent awards confirm that the first-quarter intake was not an isolated spike. They represent a sustained capture strategy targeting high-priority federal spending allocations.

Evaluating defence and infrastructure equities requires a specific framework for measuring future revenue visibility. The total project backlog represents the maximum potential value of all awarded contracts, but it includes unappropriated government spending that remains subject to future budget approvals. In federal contracting, these unappropriated funds carry inherent political and legislative risk.

Funded commitments provide a far more rigorous metric, representing the exact dollar amount that clients have legally authorised and financed for immediate work. The firm’s achievement of $6.6 billion in funded commitments marks its highest level since the initial public offering. This distinction between theoretical backlog and actual funded commitments allows investors to accurately model near-term cash flow predictability without overvaluing unappropriated federal contracts.

The Book-to-Bill Multiplier A book-to-bill ratio measures the amount of new orders received relative to the amount of work billed during a specific period. Achieving a 1.4x multiple across all operating units signals highly bullish commercial expansion, indicating the company adds $1.40 in new contract value for every $1.00 of completed work.

This accelerated intake multiple ensures the business maintains a growing pipeline of funded, executable projects. Commercial searchers and analysts rely on this specific ratio to confirm that a defence contractor is expanding its market footprint rather than simply depleting its existing reserves.

For readers wanting to master these metrics, our full explainer on defence contractor backlogs breaks down how funded commitments and unappropriated obligations dictate long-term valuations across the sector.

High contract volume requires disciplined margin control to generate shareholder value in the defence sector. While the headline top-line sales faced temporary headwinds from the classified contract drawdown, management successfully converted the remaining revenue into record profitability. The company is extracting more profit from every dollar earned, proving that its operational leverage remains highly effective despite the top-line contraction.

The strong margin performance connects directly to efficient project execution and tight cost controls across the enterprise. This structural capability allowed the business to beat Wall Street earnings projections by a wide margin. The deliberate focus on high-margin space and cyber sectors actively improved the broader profitability profile.

Securing record adjusted first-quarter margins above 10 percent demonstrates how management has successfully pivoted toward operational efficiency to offset top-line headwinds.

The quarter delivered specific profitability milestones that underscore this operational efficiency:

While bottom-line net income dropped, the adjusted metrics confirm the underlying business is generating cash more efficiently. Management has successfully decoupled profit expansion from raw volume growth.

Management’s decision to reaffirm its full-year guidance suggests high confidence that the first-quarter revenue contraction will not define the annual trajectory. The projected timeline assumes the massive current backlog will convert to active billings over the coming quarters, offsetting the early-year volume declines. This stability in forecasting gives the market a clear baseline for evaluating the stock’s commercial trajectory moving forward.

On the morning of the earnings release, the stock price remained steady at $53.45 in pre-market trading. This stability indicates that institutional investors had largely priced in the temporary accounting distortions and remained focused on the margin expansion. Analysts will now watch the execution rate of the newly awarded cyber and transportation contracts as primary catalysts for the remainder of the year.

| Metric | Company Guidance Range | Market Consensus |

|---|---|---|

| 2026 Total Revenue | $6.5 billion to $6.8 billion | Not distinctly modelled |

| 2026 Adjusted EBITDA | $615 million to $675 million | Not distinctly modelled |

| Implied Revenue Midpoint | $6.65 billion | Not distinctly modelled |

By benchmarking these projections against current consensus estimates, investors gain a definitive forward-looking view. The narrow gap between company guidance and external models confirms a shared understanding of the firm’s earning potential.

Investors exploring the broader analyst consensus will find our detailed coverage of Parsons stock ratings, which examines why Wall Street maintains an outperform outlook and an average price target of $75.11 despite the recent revenue miss.

The core analytical thesis for this contractor rests on its unprecedented $9.3 billion backlog, which provides a massive structural cushion against short-term revenue fluctuations. While a single classified agreement skewed the early 2026 top-line figures, the underlying expansion in space, cyber, and transportation confirms a durable growth trajectory. The record 10.1% EBITDA margin proves the company’s operational leverage remains intact, capable of extracting higher yields from incoming contracts.

The firm’s expanding cyber footprint positions it to capitalise on accelerating artificial intelligence infrastructure spending, as securing massive federal data centers becomes a paramount national security priority.

Investors evaluating the stock’s risk profile should weigh the temporary accounting distortions against the highly secure nature of its U.S. federal and critical infrastructure pipeline. The accelerated booking velocity indicates long-term commercial leadership in high-barrier markets.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Parsons' first-quarter 2026 revenue decline was primarily due to the temporary distortion from a single fixed-price classified contract, not a broad operational slowdown. Excluding this contract, total revenue grew 8% and organic revenue increased 3%.

Parsons achieved a 1.4x book-to-bill ratio in Q1 2026, meaning it secured $1.40 in new contract value for every $1.00 of completed work. This ratio signals robust commercial expansion and a growing pipeline of future projects.

Funded commitments represent the exact dollar amount clients have legally authorized and financed for immediate work, offering reliable near-term cash flow predictability. Total project backlog includes unappropriated government spending, which carries inherent political and legislative risk.

Yes, Parsons' management reaffirmed its full-year 2026 financial guidance, indicating high confidence that the first-quarter revenue contraction will not define the annual trajectory. This stability provides a clear baseline for market evaluation.