Under 1% of OBDC II Shareholders Accepted Saba’s $3.80 Offer

15 hrs ago

Domino’s Pizza just delivered its worst single-day share decline in recent memory. DPZ fell 9.57% to $332.63 on 27 April 2026, touching a fresh 52-week low after Q1 2026 results missed on every major metric: revenue, earnings per share, and same-store sales. The miss lands at a sensitive moment for consumer-facing equities. Domino’s is among the first major quick-service restaurant (QSR) names to report Q1 2026 results, making its commentary on consumer behaviour and full-year guidance an early data point for the broader earnings season.

What follows walks investors through every key metric from the Q1 2026 print, explains what drove the shortfall, situates the result within the QSR category, and lays out what the revised guidance means for shareholders holding or evaluating DPZ.

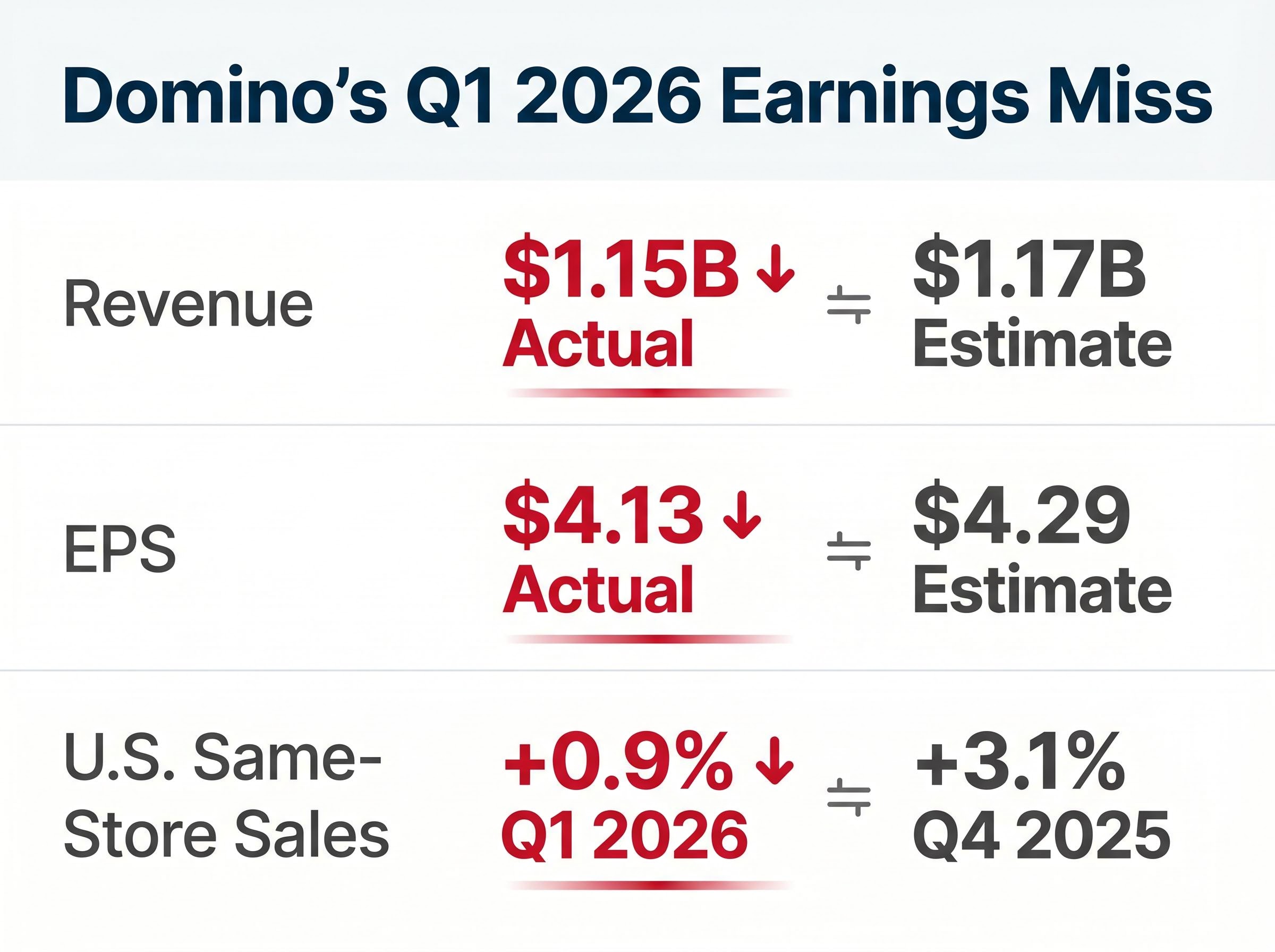

Revenue came in at $1.15 billion against estimates of $1.17 billion. Earnings per share landed at $4.13 versus a consensus estimate of $4.29, a miss of approximately 3.82% and a 4.6% decline year over year. U.S. same-store sales grew just +0.9% in Q1 2026.

That same-store sales figure is the number that stung most. In Q4 2025, U.S. same-store sales grew +3.1%. For full-year fiscal 2025, the figure was +3.0%. A deceleration to +0.9% in a single quarter signals a sharp shift in store-level momentum, and for a franchise-heavy model where revenue is tied to royalty streams from store-level performance, that metric is the core health signal.

International same-store sales added further pressure, declining -0.4% on an ex-foreign-exchange basis in Q1 2026.

| Metric | Q1 2026 Actual | Estimate / Prior Period |

|---|---|---|

| Revenue | $1.15B | $1.17B (est.) |

| EPS | $4.13 | $4.29 (est.) |

| U.S. Same-Store Sales | +0.9% | +3.1% (Q4 2025) |

| International SSS (ex-FX) | -0.4% | N/A |

Supporting metrics reinforced the softness:

Management pointed to a consumer environment that had deteriorated to levels not seen since the COVID-19 pandemic. CFO Sandeep Reddy cited the macro backdrop as the primary driver behind the full-year guidance revision, framing the quarter’s weakness as demand-led rather than operational.

The consumer sentiment divergence from equity market performance has been one of the defining analytical puzzles of 2026, with the University of Michigan Consumer Sentiment Index at a record low of 49.8 even as the S&P 500 held near record highs, a tension that makes management commentary like Domino’s pandemic-era confidence comparison harder to dismiss as company-specific hyperbole.

Management commentary: Consumer confidence was characterised as falling to levels comparable to COVID-19 pandemic lows, a framing that signals management views the pullback as systemic rather than temporary.

March was the quarter’s fault line. Management acknowledged that performance in the final weeks of Q1 did not meet expectations, establishing that the quarter worsened as it progressed rather than starting soft and stabilising. That trajectory matters: a deteriorating trend into March raises the question of whether April has improved or continued to soften.

Four factors contributed to the miss:

When consumers pull back on an affordable meal like pizza delivery, one of the lowest-cost discretionary purchases available, it carries weight as a signal about household budget tightening. The investment question is whether this is a category-wide problem or a Domino’s-specific execution issue. The answer determines the recovery timeline.

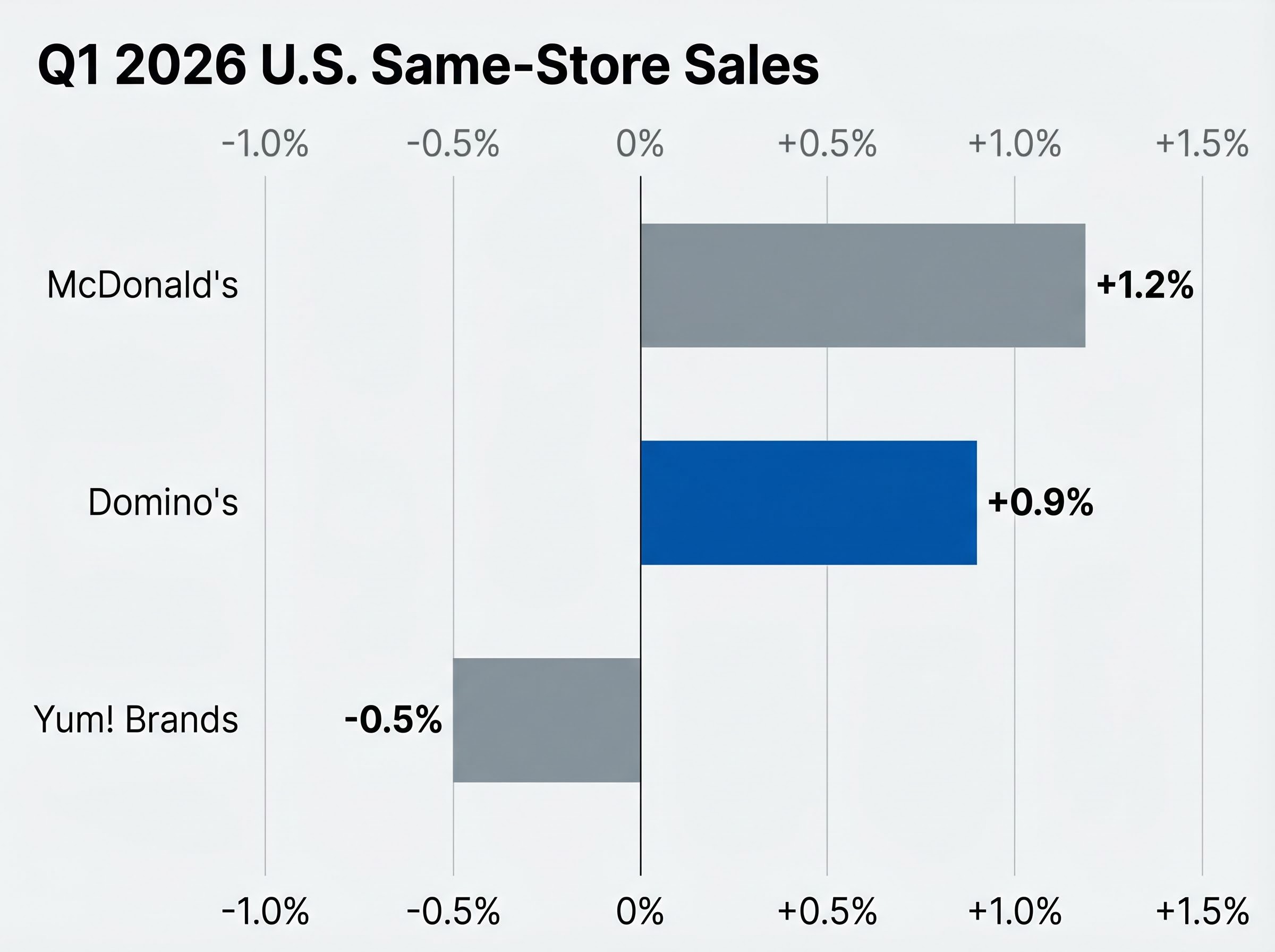

Peer results offer the fastest way to separate a company story from a category story. Same-store sales (SSS) measure revenue growth at locations open for at least a year, stripping out the effect of new store openings. For QSR investors, it is the clearest gauge of whether existing customers are spending more or less.

| Company | Q1 2026 U.S. SSS | Q4 2025 U.S. SSS |

|---|---|---|

| McDonald’s (MCD) | +1.2% | N/A |

| Domino’s (DPZ) | +0.9% | +3.1% |

| Yum! Brands (YUM) | -0.5% | N/A |

Domino’s Q1 result sits between McDonald’s modest positive and Yum! Brands’ outright decline. The category is under pressure. Inflation and competitive dynamics have been cited across multiple QSR operators this earnings season, confirming that the consumer pullback is not isolated to a single name.

The distinguishing factor for DPZ is the magnitude of deceleration. Moving from +3.1% in Q4 2025 to +0.9% in Q1 2026 represents a sharper sequential drop than peers have reported. That gap leaves a company-specific question mark hanging alongside the category-wide headwinds. Investors in QSR names broadly should note the pattern; DPZ holders specifically should watch whether Q2 data narrows or widens that gap.

Delivery channel economics in franchise QSR models have become a competitive differentiator as operators seek margin improvements that do not require same-store sales acceleration, with some chains locking in exclusive third-party partnerships to lower per-order costs and improve franchisee unit economics in a period of softening traffic.

Domino’s revised its full-year 2026 U.S. same-store sales guidance to low single digits, down from prior guidance of approximately 3%. The revision acknowledges what the Q1 print made clear: the original target is no longer credible.

The arithmetic problem is straightforward. Q1 delivered +0.9%. To hit even a 2% full-year figure, the remaining three quarters would need to average roughly 2.4% or higher. That implies a meaningful sequential acceleration from the trend that was still deteriorating in March. Management provided no specific Q2 2026 guidance on the earnings call, leaving the path to that acceleration unclear.

Street consensus: The mean analyst price target sits at approximately $464, implying roughly 39% upside from the 27 April close of $332.63. That gap is wide, but it reflects pre-earnings targets that may face further revision.

Three forward-looking considerations for investors:

Guidance credibility is the central question. The revised guide is lower, but it still requires improvement that Q1’s trajectory does not yet support.

The trading session on 27 April 2026 told a clear story of conviction:

From its 52-week high of $499.08, DPZ has now fallen approximately 33.4% to the 27 April close. More than a third of the stock’s peak value has been erased.

Volume tells as much of the story as price. Nearly three times the average daily volume traded on the session, a pattern more consistent with institutional repositioning than retail-driven panic. When elevated volume accompanies a new 52-week low, it signals that larger holders are adjusting their exposure with conviction rather than waiting for a bounce.

The broader market session on 27 April 2026 was already under pressure before the Domino’s print landed, with Brent crude at approximately $100 per barrel following the collapse of U.S.-Iran peace talks, a macro backdrop that compounded the selling pressure across consumer-facing equities.

The market cap of approximately $12 billion frames the dollar magnitude: a 9.57% single-day move on a company of this size represents more than $1 billion in value destroyed in a single session.

The question for investors evaluating whether to add, hold, or reduce DPZ exposure is whether this repricing has fully absorbed the guidance risk, or whether the stock is now positioned at a valuation entry point. The gap between the current price and the street mean target of $464 suggests the analyst community, at least before post-earnings revisions, sees value at these levels. Whether that view holds depends on the next quarter’s data.

The three layers of this story are clear: an operational miss across revenue, EPS, and same-store sales; a macro backdrop in which consumer confidence has fallen to pandemic-era levels; and a market verdict delivered through a new 52-week low on nearly triple average volume. The forward-looking question is whether Domino’s can deliver the sequential same-store sales acceleration its revised low single-digit full-year guide requires, and whether broader QSR category data from remaining Q1 reporters will corroborate or contradict the consumer weakness narrative. Investors seeking the full picture should monitor the official Q1 2026 earnings call transcript on Domino’s Investor Relations, the Q1 2026 10-Q filing on SEC EDGAR, and post-earnings analyst notes as they are published in the coming days.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Forward-looking statements, including guidance targets and analyst price targets, are subject to change based on market developments and company performance.

Domino's Q1 2026 earnings missed on every key metric: revenue came in at $1.15 billion versus the $1.17 billion estimate, EPS was $4.13 against a $4.29 consensus, and U.S. same-store sales grew just 0.9%, down sharply from 3.1% in Q4 2025.

DPZ fell 9.57% to $332.63 on 27 April 2026, hitting a fresh 52-week low, as the earnings miss was compounded by a full-year guidance cut and management commentary comparing consumer confidence to pandemic-era lows, with nearly triple the average daily trading volume indicating institutional selling.

Same-store sales measures revenue growth at locations open for at least a year, stripping out the effect of new store openings; for Domino's, which operates a franchise-heavy model where revenue is tied to royalty streams from store-level performance, it is the core health signal for the business.

Domino's Q1 2026 U.S. same-store sales of 0.9% sat between McDonald's modest 1.2% gain and Yum! Brands' 0.5% decline, but the sharp sequential deceleration from Domino's own 3.1% Q4 2025 figure was steeper than peers, leaving a company-specific question mark alongside broader category headwinds.

Domino's revised its full-year 2026 U.S. same-store sales guidance down to low single digits from its prior target of approximately 3%, a cut that requires meaningful sequential acceleration from Q1's 0.9% pace across the remaining three quarters with no specific Q2 guidance provided.