Record Revenues, Falling EPS: the AI Capex Effect Explained

11 hrs ago

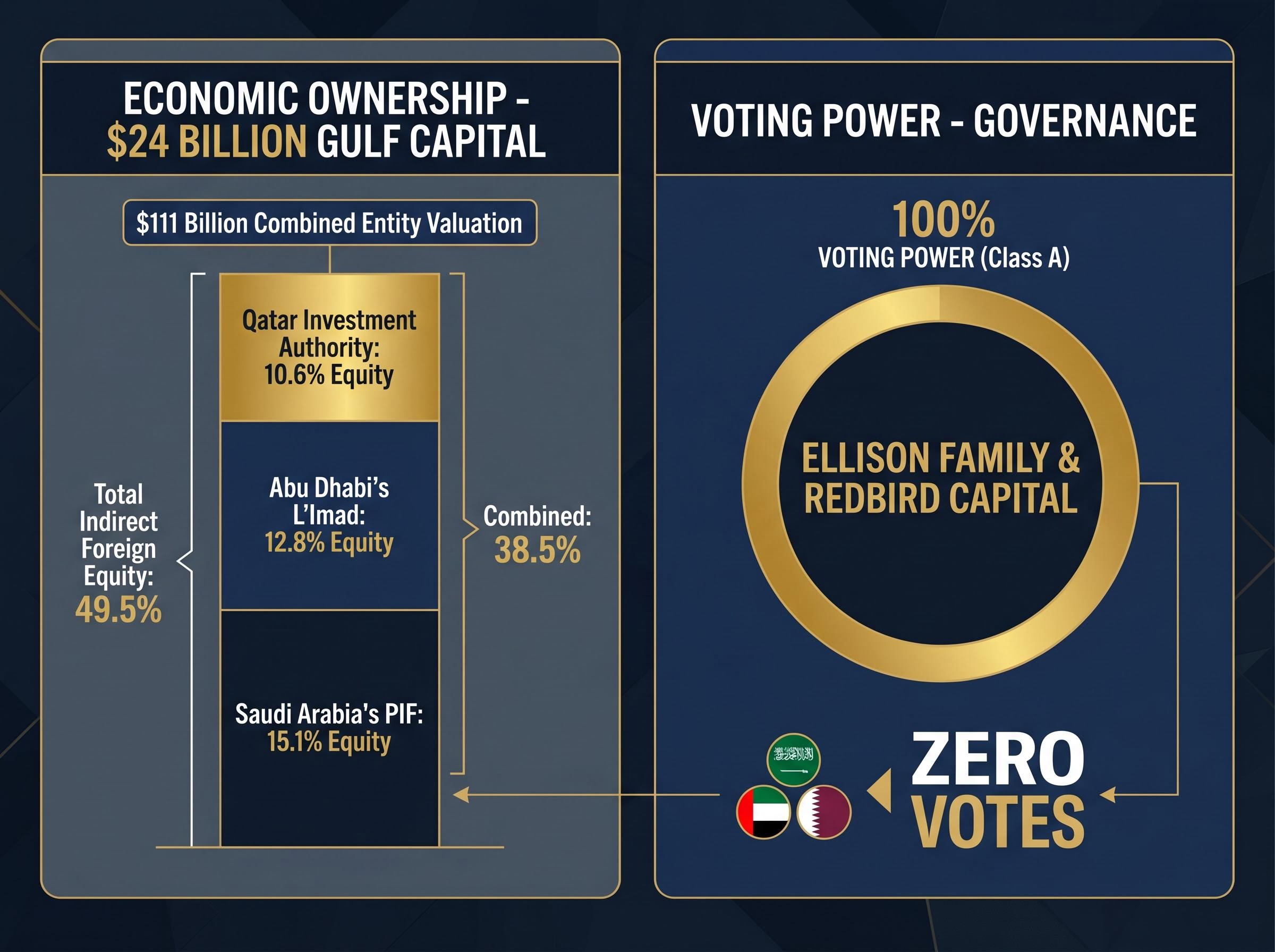

Saudi Arabia’s Public Investment Fund is set to hold 15.1% of a combined media entity valued at approximately $111 billion, yet it will have zero say in a single board decision. That is not an oversight. It is the architecture.

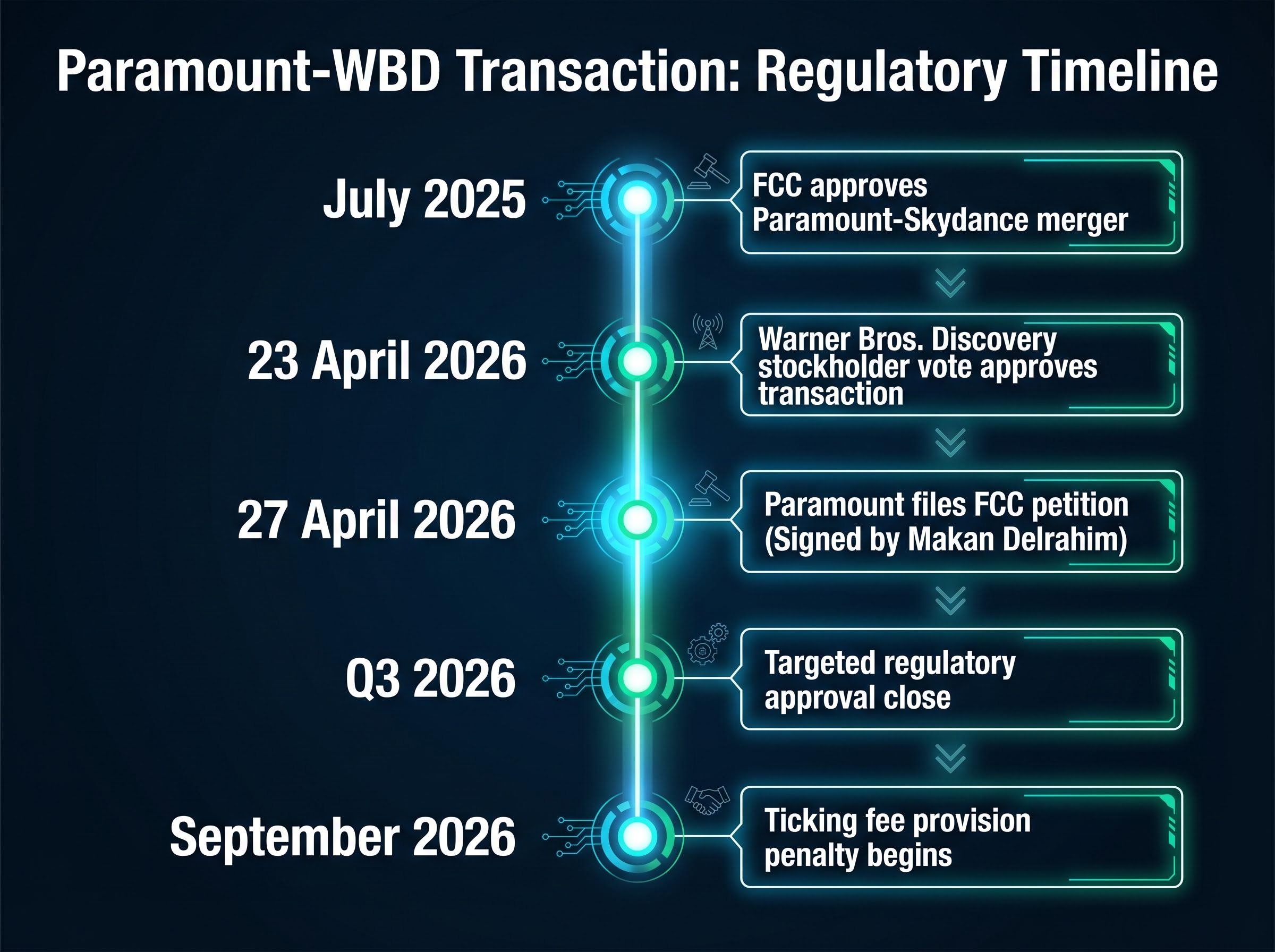

On 27 April 2026, Paramount filed a declaratory ruling petition with the Federal Communications Commission (FCC) seeking clearance for roughly $24 billion in capital from three Gulf sovereign wealth funds: Saudi Arabia’s PIF, Abu Dhabi’s L’Imad, and the Qatar Investment Authority. The filing was notable not for what the foreign investors would receive, but for what they explicitly would not: no voting shares, no board seats, no governance rights. The Ellison family and RedBird Capital hold 100% of Class A Common Stock, and therefore 100% of voting power in the combined entity. This article explains how dual class shares work, why the Paramount-WBD deal applies the mechanic at an unprecedented scale, and what the regulatory logic behind separating economic ownership from voting control reveals about how large US media companies are structuring foreign capital in 2026.

Most investors assume that owning a share means owning a vote. For roughly 90% of S&P 500 companies, that assumption holds. For the other 10%, according to 2023 ISS Governance data, it does not.

Dual-class share structures allow a company to issue multiple classes of stock with different voting rights attached to each class. Economic ownership and decision-making power become legally separable. The typical arrangement: Class A shares carry superior or exclusive voting rights and are retained by insiders; Class B shares carry limited or zero votes and are sold to outside investors seeking returns.

| Attribute | Class A shares | Class B shares |

|---|---|---|

| Voting rights | Superior or exclusive | Limited or zero |

| Typical holder | Founders, families, strategic operators | Public or passive investors |

| Primary purpose | Governance control retention | Capital access and financial returns |

The structure exists specifically to let a company raise large amounts of capital without diluting the control of founders, families, or strategic operators. Google (now Alphabet) adopted a multi-class structure at its IPO, setting a landmark precedent. Snap Inc. pushed the mechanic to its extreme.

Snap’s zero-vote structure: When Snap Inc. went public, it issued shares to the public with zero votes per share, one of the most aggressive implementations of dual-class architecture on record. Public shareholders received full economic exposure and zero governance influence.

The legal foundation for these structures sits in Delaware corporate law, where most major US companies incorporate. Understanding this mechanic is the prerequisite for everything that follows. Without it, the Paramount deal reads as unusual; with it, the deal reads as a deliberate, well-established playbook executed at scale.

The common assumption is that regulators care about who owns a company. The more precise reality: they care about who controls one.

FCC Section 310 restricts foreign ownership of broadcast licences. The statute evaluates whether foreign parties exercise voting control or governance influence over licence holders, not merely whether they hold equity. That distinction is what makes the Paramount structure viable rather than merely clever.

The FCC Section 310 foreign ownership restrictions on broadcast licences set a 20% direct and 25% indirect statutory ceiling on foreign capital stock and voting control — the specific thresholds that make separating economic ownership from governance rights not merely a structural preference but a regulatory necessity for any transaction of this scale.

The Committee on Foreign Investment in the United States (CFIUS) adds a second layer. CFIUS reviews transactions for national security risks, and the exclusion of foreign parties from voting rights in the Paramount-WBD structure was explicitly designed to preempt both CFIUS and Team Telecom (the Committee for the Assessment of Foreign Participation in the United States Telecommunications Services Sector) scrutiny. Paramount submitted responses to Team Telecom alongside its FCC petition, framing the non-voting structure as the mechanism that makes the foreign capital compatible with US broadcast ownership rules.

Paramount has characterised the non-voting structure as improving regulatory approval odds compared to competing proposals, including Netflix’s rival approach.

The FCC approved the Paramount-Skydance merger in July 2025, establishing regulatory precedent for structures that limit foreign voting influence while permitting foreign equity. Paramount’s current petition requests authorisation for up to 100% of equity to potentially be held by foreign parties, described in the filing as a procedural measure rather than an indication of future intentions. Senators have urged CFIUS review specifically because of the scale of Gulf sovereign fund involvement, but the governance firewall is not optional window-dressing. This structural separation is what allows $24 billion in Gulf sovereign capital to remain legally and regulatorily consistent with US broadcast licence ownership requirements.

The deal architecture separates capital flows from governance rights with a precision that reads like it was designed for a regulatory filing, because it was.

Three Gulf sovereign wealth funds provide $24 billion in non-voting equity. Their projected stakes in the combined entity:

| Sovereign fund | Projected equity stake | Voting rights |

|---|---|---|

| Saudi Arabia’s PIF | 15.1% | Zero |

| Abu Dhabi’s L’Imad | 12.8% | Zero |

| Qatar Investment Authority | 10.6% | Zero |

Combined, the three funds hold 38.5% of equity in the combined entity, with total indirect foreign equity estimated at 49.5%. Class B non-voting shares are backed at $16.02 per share. Additional passive investors in RedBird funds and Form 13F filers also hold non-voting equity positions.

Class A Common Stock is held solely by the Ellison family and RedBird Capital, representing 100% of voting power. No foreign partner, regardless of equity stake size, has any path to governance influence under this structure.

The Warner Bros. Discovery stockholder vote on 23 April 2026 approved the transaction overwhelmingly. Regulatory approvals are targeting a Q3 2026 close. Paramount’s chief legal officer Makan Delrahim signed the FCC petition filed 27 April 2026.

The regulatory path is not a single-track process: Senate opposition, a CFIUS petition, and Team Telecom review are all active simultaneously, and Team Telecom’s 120-day window with a possible 30-day extension means its conclusions could impose conditions on the deal regardless of what the FCC decides on the foreign equity question alone.

A Paramount spokesperson described the structure as “a clear separation between financial investors and decision-making authority.” That separation is not a side detail of a $111 billion deal. It is the entire structural premise.

The Paramount-WBD structure is not an invention. It is an adaptation of a governance tool that US media and technology companies have relied on for decades.

The NYSE and Nasdaq adopted rules in 2017 requiring “one share, one vote” for newly listed companies, though pre-existing dual-class structures are grandfathered. The CFA Institute and Harvard Law School’s Corporate Governance Forum have both published substantial analysis on the governance implications for readers seeking deeper institutional perspectives.

Dual-class contracting is the subject of substantial peer-reviewed analysis by the Harvard Law School Forum on Corporate Governance, which examines how proportional voting inequalities are structured across share classes and the long-running institutional debate over whether founder control mechanisms serve or undermine shareholder interests — providing the academic foundation for the governance critique that organisations like BlackRock have formalised into voting policy.

The newer application is more specific. Dual-class structures are increasingly being deployed not merely to protect founder vision from activist investors, but to enable large passive capital injections from sovereign wealth funds who seek financial returns without governance entanglement. The Paramount-WBD deal represents this pattern at its largest scale to date: sovereign fund investors providing $24 billion in capital with no expectation of, and no structural path toward, governance influence.

The counterargument carries genuine institutional weight.

Organisations including BlackRock argue that dual-class shares undermine the accountability mechanism at the heart of public company governance. The three strongest arguments against dual-class structures:

BlackRock’s policy position identifies dual-class structures as a governance concern, arguing that they weaken the link between economic ownership and accountability that underpins effective corporate oversight.

The three strongest arguments in favour:

The SEC has scrutinised dual-class structures for investor protection purposes, and the 2017 NYSE/Nasdaq rule change reflects regulatory concern about new dual-class listings. There is a structural irony in the Paramount case specifically: the sovereign fund investors are not being disenfranchised against their wishes. They are, by design, passive capital sources who seek returns rather than control, making the governance critique more relevant to other non-voting share classes than to the sovereign fund stakes in this transaction.

The Paramount-WBD architecture demonstrates something more durable than a single deal structure. It demonstrates a repeatable template.

For this template to work in future transactions, three conditions must be met:

Makan Delrahim argued in the FCC filing that broader foreign capital access would strengthen broadcast operations, local news, technology infrastructure, and programming diversity. The filing cited the UFC broadcast rights deal as a specific example of content expansion enabled by foreign capital at scale.

Paramount’s affirmative case for why Gulf capital strengthens US broadcasting centres on the structural decline of linear TV revenue, with cable subscribers falling from approximately 105 million in 2010 to around 68.7 million in 2026, and the argument that sovereign capital at this scale is the mechanism available to sustain broadcast investment in a contracting market.

Netflix has taken an active opposition stance against the merger, and a ticking fee provision penalising delays past September 2026 means the transaction timeline carries tangible financial consequences for all parties. As traditional broadcasters and linear pay-TV operators face structural revenue pressure, the ability to access sovereign capital at scale, without triggering foreign ownership restrictions, may become a significant competitive differentiator for companies that can architect this separation cleanly.

According to Paramount’s filings, the non-voting structure is designed to deliver stronger regulatory approval prospects than rival approaches. If the FCC and CFIUS approve the transaction as structured, it establishes a precedent that other US media companies could follow when seeking large-scale passive foreign investment.

These statements are speculative and subject to change based on market developments, regulatory decisions, and company performance.

The Ellison-RedBird voting control structure is not incidental to the Paramount-WBD deal. It is the mechanism that makes $24 billion in Gulf sovereign capital legally and regulatorily compatible with US broadcast ownership.

The article has covered three distinct layers: the mechanical (how dual-class shares separate votes from equity), the regulatory (why the FCC and CFIUS evaluate voting control rather than economic ownership), and the strategic (why this template is positioned to recur in US media and entertainment finance as sovereign capital becomes a larger feature of industry deal-making). Each layer reinforces the same structural insight: in US media, the question is not who provides the capital. The question is who holds the vote.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

For further reading, related explainers on corporate governance structures, FCC broadcast ownership rules, and CFIUS review mechanics offer additional depth on the regulatory and structural dimensions covered here.

—

Dual class shares allow a company to issue multiple classes of stock with different voting rights, so economic ownership and decision-making power become legally separate. Insiders retain Class A shares with superior or exclusive votes, while outside investors receive Class B shares with limited or zero votes.

Saudi Arabia's PIF, Abu Dhabi's L'Imad, and the Qatar Investment Authority hold non-voting equity specifically to comply with FCC Section 310, which restricts foreign parties from exercising voting control over US broadcast licence holders. The Ellison family and RedBird Capital retain 100% of Class A voting shares.

FCC Section 310 sets a 20% direct and 25% indirect statutory ceiling on foreign capital stock and voting control in entities holding US broadcast licences. The non-voting share structure in the Paramount-WBD deal is designed to keep the $24 billion in Gulf sovereign capital legally compatible with these restrictions.

Saudi Arabia's PIF holds 15.1%, Abu Dhabi's L'Imad holds 12.8%, and the Qatar Investment Authority holds 10.6%, for a combined total of 38.5% of equity in the combined entity, with total indirect foreign equity estimated at 49.5%.

Paramount's filings argue the non-voting structure offers stronger regulatory approval prospects than rival approaches, and if the FCC and CFIUS approve the transaction, it would establish a precedent that other US media companies could follow when seeking large-scale passive foreign investment.