How $4B in Fuel Costs Erased American Airlines’ Record Q1

6 mins ago

Jakarta’s Composite index shed roughly $190 billion in value following MSCI’s downgrade warning in early 2025, the kind of market shock that forces regulators to confront concentrated ownership structures they had previously tolerated. What followed was an 18-month arc from crisis to partial rehabilitation, a test case for emerging market governance that moved through stock removals, regulatory reforms, and progressive re-inclusions. Indonesia’s journey from MSCI exclusion notices to gradual index reinstatement offers lessons for investors navigating markets where ownership transparency remains contested, and where investability standards can shift abruptly under global scrutiny.

This analysis traces the full timeline from MSCI’s initial removals through regulatory response and gradual rehabilitation, examining what the episode reveals about emerging market investability standards and where unresolved risks remain.

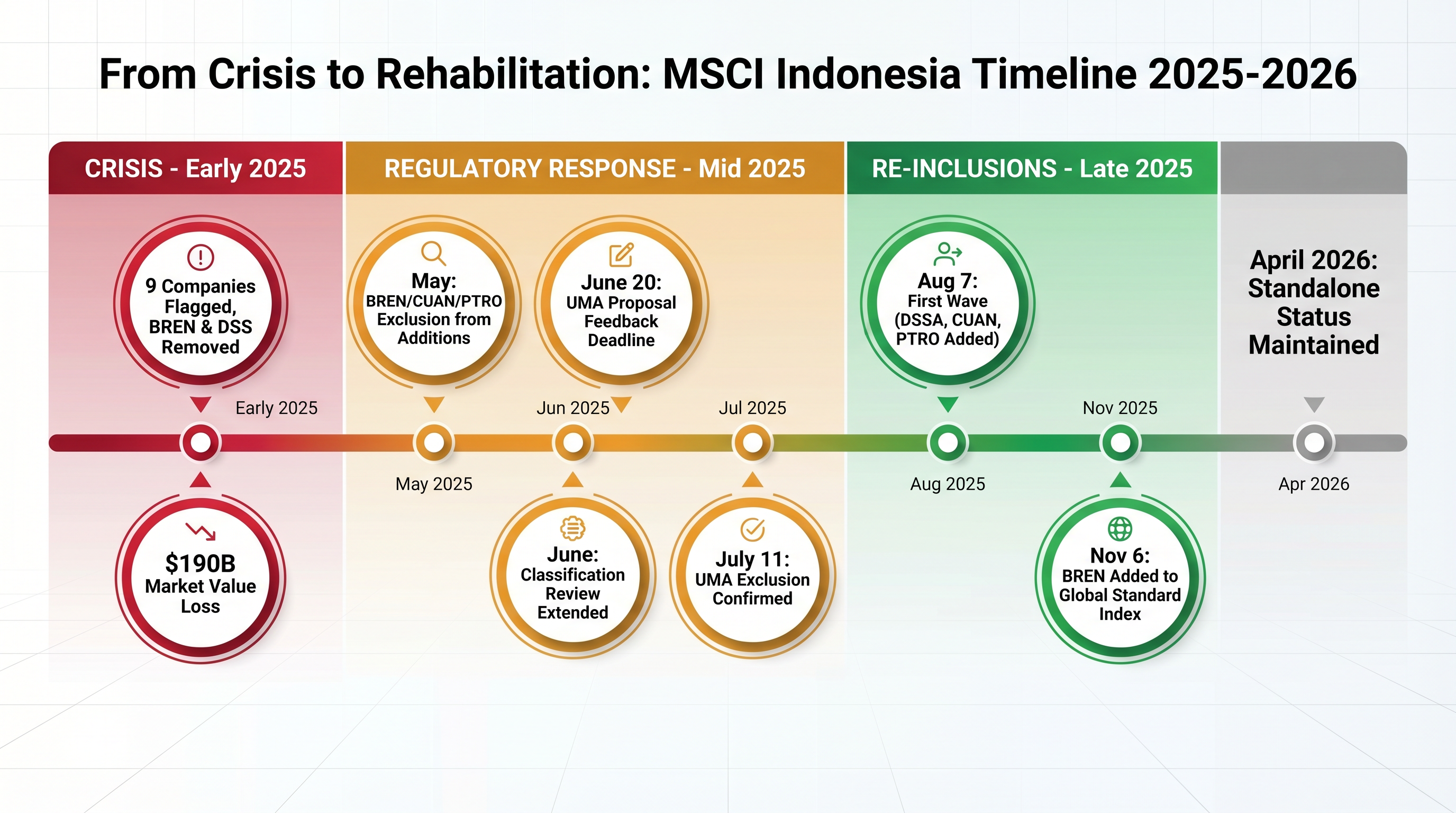

The catalyst was ownership concentration that reached levels incompatible with passive fund mandates. Indonesia’s stock exchange flagged nine companies for disclosure irregularities in early 2025, but only two faced actual MSCI removal because they were the only flagged entities included in MSCI’s Indonesia indices at the time: Barito Renewables Energy (BREN) and Dian Swastatika Sentosa (DSS).

The concentration figures were stark:

97.3% of Barito Renewables shares were held by a small shareholder group, while 95.76% of DSS shares showed similar concentration.

These disclosures triggered immediate market repricing. Barito Renewables declined 8% on the announcement day, DSS dropped 14%, and the Jakarta Composite index fell 1% in the same session. The removals were not arbitrary. Concentration at these levels made the stocks mechanically incompatible with index fund mandates requiring tradeable float, directly affecting eligibility for passive investment vehicles that track MSCI benchmarks.

The individual stock removals escalated into a broader threat. MSCI warned that Indonesia’s entire emerging market classification could face downgrade if ownership transparency issues persisted across the market. Two stocks had become a systemic concern.

Indonesia’s frontier downgrade risk following the $190 billion market rout created immediate pressure for regulatory reforms that the Indonesian Financial Services Authority had previously resisted, setting the stage for the ownership transparency requirements introduced in mid-2025.

Index funds cannot hold shares that are not genuinely available for trading. Passive funds tracking MSCI benchmarks require sufficient free float to enter and exit positions without moving prices, a mechanical necessity that breaks when ownership is concentrated in the hands of a small shareholder group. MSCI defines free float as shares available to international investors, excluding strategic holdings, cross-holdings, and shares held by controlling shareholders.

The passive fund mechanics driving index addition flows work symmetrically in reverse during exclusions, as funds tracking MSCI benchmarks face mandate-driven selling regardless of fundamental views on the excluded stocks, a mechanical dynamic that amplified the price impact on BREN and DSS.

Indonesia’s regulatory framework had permitted free float as low as approximately 7.5% prior to the crisis. When BREN and DSS disclosed concentration above 95%, the remaining tradeable float fell below levels MSCI considers investable. The index provider responded with “exceptional treatment”, a mechanism that excluded certain stocks from scheduled additions even when they met size and liquidity thresholds.

Concentrated ownership was not the sole red flag. MSCI’s exceptional treatment in the May 2025 Index Review excluded three stocks from additions: BREN, CUAN (Petrindo Jaya Kreasi), and PTRO (Petrosea). The exclusions cited three conditions:

UMA listings flag stocks for abnormal price movements under Indonesia’s Kriteria 10 framework. PTRO and BRPT had been placed on UMA watch in December 2024 following unexplained volatility. Global investors alleged the volatility stemmed from nominee structures and wash trading, accusations that prompted an investigation by Indonesia’s Financial Services Authority (OJK). The UMA history compounded concentration concerns, signalling to MSCI that price discovery mechanisms were compromised.

For investors exploring emerging market exposures through online platforms after reading about Indonesia’s nominee structure issues, our comprehensive walkthrough of how to identify fraudulent trading platforms covers the specific red flags around nominee arrangements, wash trading indicators, and regulatory verification steps that protect against the opacity concerns highlighted in Indonesia’s MSCI case.

MSCI proposed a methodology update to exclude UMA-listed stocks from index additions, with a feedback deadline of 20 June 2025. The proposal created indirect pressure for market reforms by making clear that UMA listings would block index eligibility regardless of concentration improvements.

Indonesia’s regulatory changes arrived as a direct response to MSCI pressure, not as proactive governance improvements. The reforms addressed the concentration and transparency gaps MSCI had flagged, but the sequence reveals reactive rather than anticipatory policymaking.

The key reforms doubled free float requirements and tightened disclosure thresholds:

| Reform Measure | Old Threshold | New Threshold | Implementation Timeline |

|---|---|---|---|

| Free Float Requirement | ~7.5% | 15% | 3-year transition period |

| Ownership Disclosure Threshold | 5% | 1% | Immediate |

The 15% free float requirement represented a doubling of the previous standard, a material increase but one that still left Indonesia below the 20-25% thresholds common in more developed emerging markets. The lowered disclosure threshold from 5% to 1% aimed to surface nominee structures and hidden beneficial ownership, the opacity that had enabled concentration to reach 97% without earlier regulatory intervention.

MSCI clarified its methodology update on 11 July 2025, confirming that UMA-listed stocks would face exclusion. The timing mattered. MSCI had extended its review of Indonesia’s market classification in June 2025, delaying any upgrade decision. The extension kept pressure on regulators, and the market had already lost $190 billion in value since the initial downgrade warning. The three-year compliance window granted for the 15% free float requirement signalled regulatory seriousness, but it also meant structural changes would remain incomplete until 2028.

MSCI’s concerns proved addressable, but the timeline for rehabilitation stretched across five months of progressive re-inclusions. The sequence demonstrated that index exclusions are not permanent sentences when underlying investability issues are resolved.

7 August 2025: MSCI added DSSA, CUAN, and PTRO to its indices, the first wave of re-inclusions following reforms.

6 November 2025: BREN was added to the MSCI Global Standard Index, completing the cycle for the highest-profile exclusion.

BREN’s price movement tracked the rehabilitation arc. The stock traded at Rp 7,950 on 8 August 2025 despite initial exclusion, then surged 9.66% on optimism around eventual inclusion. By 11 November 2025, the stock had reached Rp 10,000, posting an 8.40% gain in the week surrounding the inclusion announcement.

“MSCI’s decision to include BREN in the Global Standard Index demonstrates their trust in our commitment to financial and capacity improvements. We will continue to expand our operational footprint and maintain the transparency standards that earned this inclusion.” Tan Hendra Soetjipto, Chief Executive Officer, Barito Renewables Energy

The CEO’s statement on November 2025 inclusion framed the event as validation of governance improvements, citing the Salak Binary project’s addition of 16.6 MW in early 2025 as evidence of operational expansion alongside compliance progress.

Indonesian brokerages positioned the re-inclusions as catalysts for foreign capital inflows. KISI Sekuritas predicted that the August 2025 rebalancing would draw international funds back into Indonesian equities, a forecast supported by the progressive inclusion timeline. MNC Sekuritas issued a “buy on weakness” recommendation for BREN at Rp 7,425-7,800 following the August surge, viewing the stock as part of an upward wave that would continue through final inclusion.

Mirae Asset had predicted the August 2025 additions for BREN, PTRO, CUAN, and DSSA in advance, demonstrating that market participants understood the compliance trajectory. The re-inclusions delivered on those forecasts, but the five-month gap between initial reforms and final BREN inclusion showed the deliberate pace of MSCI’s validation process.

Indonesia’s progress from crisis to partial rehabilitation is visible in the stock-level re-inclusions, but the absence of certain data points means investors cannot yet confirm that structural risks have been resolved. Three key unknowns remain:

The re-inclusions demonstrate that stocks addressing investability concerns can regain index eligibility, potentially offering entry opportunities during exclusion periods. However, the absence of enforcement actions or comprehensive compliance data means the structural governance test remains incomplete.

Indonesia faced a governance crisis in early 2025 that threatened its emerging market status, implemented reforms under MSCI pressure, and achieved progressive re-inclusions by late 2025. The arc from $190 billion market value loss to stock-level rehabilitation demonstrates that concentrated ownership issues are addressable when regulatory will aligns with index provider standards. However, the absence of OJK investigation outcomes and quantified compliance progress means the structural test remains incomplete.

The three-year compliance window extends into 2028, positioning this as a multi-year reform story rather than a resolved episode. Investors should distinguish between individual stock re-inclusions, which signal specific investability improvements, and overall market classification advancement, which requires sustained progress across the broader equity universe. MSCI’s maintenance of Indonesia in the Standalone Markets category as of April 2026 indicates that classification upgrade remains contingent on further evidence.

Monitor upcoming MSCI review cycles and OJK enforcement announcements as the next decision points. The re-inclusions of BREN, DSSA, CUAN, and PTRO validate the reform trajectory, but whether Indonesia’s governance improvements produce lasting investability gains will be determined by compliance outcomes measured in 2027-2028, not by the optimism of late 2025.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

An MSCI index removal occurs when a stock or market fails to meet the index provider's investability standards, such as free float or ownership transparency requirements, triggering mandate-driven selling by passive funds that track MSCI benchmarks. In Indonesia's case, the removals of BREN and DSS escalated into a broader threat to the country's entire emerging market classification.

Barito Renewables Energy (BREN) and Dian Swastatika Sentosa (DSS) were removed because ownership concentration exceeded 95%, leaving tradeable free float well below MSCI's investability threshold. Additional stocks were excluded from index additions due to a history of Unusual Market Activity (UMA) listings and concerns about nominee structures and wash trading.

Indonesia's Financial Services Authority (OJK) doubled the free float requirement from approximately 7.5% to 15% and tightened the ownership disclosure threshold from 5% to 1%, with a three-year transition period extending to 2028. These reforms were reactive rather than proactive, introduced directly in response to MSCI pressure after the market had already lost around $190 billion in value.

DSSA, CUAN, and PTRO were added to MSCI indices on 7 August 2025, followed by BREN's addition to the MSCI Global Standard Index on 6 November 2025. The five-month gap between initial reforms and BREN's final inclusion reflects the deliberate pace of MSCI's compliance validation process.

As of April 2026, Indonesia remains in MSCI's Standalone Markets category with no confirmed upgrade to Secondary Emerging Market status, and the OJK investigation into nominee structures and wash trading has not produced documented enforcement outcomes. The three-year compliance transition extends to 2028, meaning the structural governance test remains incomplete.