How $4B in Fuel Costs Erased American Airlines’ Record Q1

11 mins ago

Indonesia’s equity market has lost US$190 billion in market value since MSCI issued its warning in January 2026, the clearest indication yet that global index classification carries direct capital stakes. On Monday, MSCI removed Barito Renewables and Dian Swastatika Sentosa (DSS) from its Indonesia Index, triggering immediate passive outflows and intensifying scrutiny ahead of the June review that will determine whether Indonesia retains its emerging market status or faces reclassification to frontier.

The removals were not arbitrary. Both companies breached MSCI’s free float standards through concentrated ownership structures that left international investors with minimal tradeable shares. Indonesia’s regulators responded with fast-tracked reforms in early April, doubling minimum free float requirements and tightening disclosure thresholds. Whether these reforms satisfy MSCI’s standards, or merely delay the inevitable, remains the central question for investors holding Indonesian exposure.

MSCI’s Monday announcement removed two stocks from its Indonesia Index: Barito Renewables and DSS. The decision followed disclosure by the Indonesian Stock Exchange (IDX) on 2 April 2026, which flagged nine companies with ownership concentrations exceeding 95%. Only two of those nine companies sat in MSCI indices, making their removal mechanically inevitable once the ownership data became public.

The ownership structures tell the story:

Ownership Concentration Barito Renewables: 97.3% held by tightly concentrated group DSS: 95.76% held by controlling interests

When the stocks resumed trading post-holiday, the market reaction was immediate. Barito Renewables slumped to two-year lows. DSS dropped 14% on Tuesday, 6 April. The Jakarta Composite Index fell 1% the same day.

Passive outflows are estimated at approximately US$1 billion if both stocks are excluded from broader MSCI weight calculations. For global investors holding Indonesia exposure through MSCI-tracking funds, the removals force immediate rebalancing. The question is no longer whether ownership concentration matters to index providers. The data answered that.

Index inclusion mechanics operate identically whether the trigger is governance improvement (additions) or structural deficiency (removals), with passive fund rebalancing creating concentrated trading volume around reconstitution dates regardless of market or direction.

When you own shares, you own shares. That assumption holds for most equity markets, but MSCI applies a different lens: indices weight companies by shares actually available to international investors, not total market capitalisation.

The methodology is called free float weighting. A company with 100 million shares outstanding but 95 million shares held by insiders trades with only 5 million shares accessible to the market. MSCI’s indices reflect that scarcity. If insiders control nearly all shares, trading volume becomes illusory and price discovery unreliable. The share price may move, but the movement reflects internal positioning rather than external demand.

The concentration risk in cap-weighted indices, where a handful of large-cap positions dominate index returns and rebalancing flows, creates similar dynamics at the country level when a few tycoon-linked stocks represent outsized weight in emerging market benchmarks.

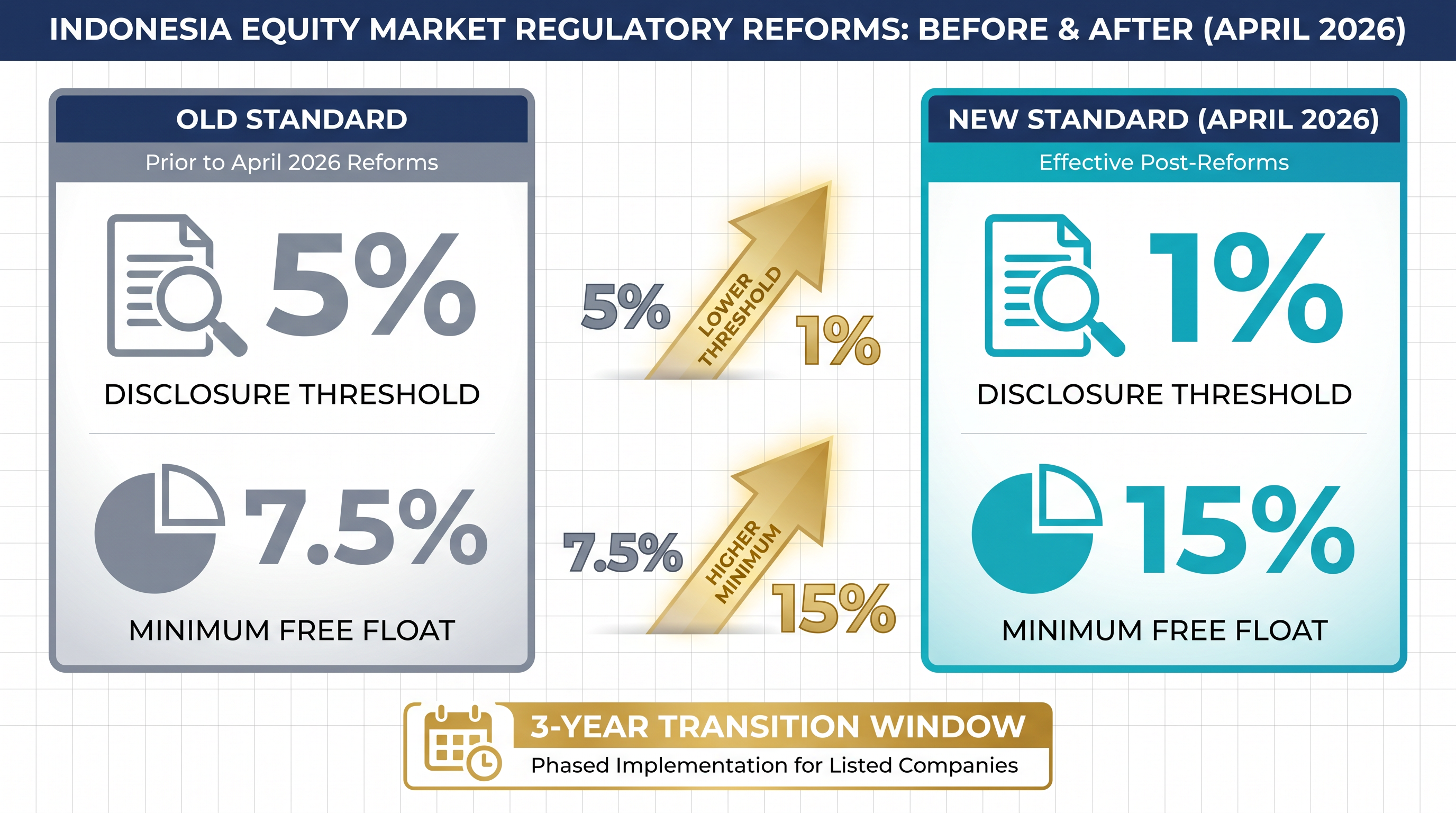

Indonesia’s previous disclosure rules compounded the problem. The old threshold required ownership disclosure only at 5%. Insiders could hold positions below that level without public visibility. The new regulation, issued in early April 2026, tightened the threshold to 1%, forcing transparency on far smaller stakes.

| Requirement | Old Standard | New Standard (April 2026) |

|---|---|---|

| Disclosure Threshold | 5% | 1% |

| Minimum Free Float | 7.5% | 15% |

| Compliance Timeline | Immediate | 3-year transition window |

The broader accusation facing Indonesian equities extends beyond the numbers. Global investors have highlighted allegations that insiders hold shares via nominee structures and trade among themselves to simulate liquidity. If those allegations hold, the market’s apparent activity masks a closed system. MSCI’s free float standards are designed to exclude precisely that scenario.

Indonesia’s regulatory response arrived in early April 2026, clearly timed to address MSCI’s pressure. The reforms contain three core components:

The doubling of the free float threshold signals intent. A company with 100 million shares must now ensure at least 15 million shares trade freely, up from 7.5 million under the old regime. The tighter disclosure rule forces transparency on smaller positions, closing the nominee structure loophole that allowed insiders to obscure control.

The three-year window is the negotiation point. It gives companies runway to restructure ownership without forcing immediate delisting, but it also creates a gap between reform announcement and actual compliance. MSCI’s June decision will not wait three years. The question is whether the reforms themselves, independent of company-level execution, satisfy MSCI’s standards enough to retain emerging market classification.

A May deadline referenced in reports is driving urgency, though specific details of what must be achieved by May remain unclear in available data.

No specific companies have publicly reported achieving the 15% free float threshold as of mid-April 2026. Barito Renewables has claimed compliance with existing requirements, but the existing requirements were the problem. Compliance rates for the new 1% disclosure rule remain unquantified in available reports.

The reforms signal regulatory willingness to engage with global standards. Whether they signal actual structural change depends on execution data that has not yet materialised.

Beyond index mechanics, Indonesia faces a governance investigation that remains unresolved. Indonesia’s Financial Services Authority (OJK) is examining potential market manipulation and suspicious trading patterns, particularly allegations that insiders designed trades to create misleading impressions of activity.

The specific claims centre on nominee structures obscuring true ownership and coordinated trades among affiliated parties to simulate liquidity. If proven, these practices would undermine the transparency reforms at a fundamental level. The reforms change the rules; the investigation examines whether the old rules were being actively circumvented.

Manipulation Allegations “Global investors have highlighted allegations that insiders hold shares via nominee structures and engage in trades among themselves to simulate liquidity.”

As of 6 April 2026, no outcomes, penalties, or enforcement actions from the OJK investigation have been announced. No companies or individuals have been formally named beyond general references to tycoon-linked firms like Barito Renewables and DSS. The investigation is an open question mark, not a closed chapter.

The outcome, or lack thereof, will shape whether Indonesia’s reforms are read as substantive or cosmetic. Transparency rules matter only if enforcement follows.

MSCI’s June review carries direct stakes: Indonesia’s classification as an emerging market versus reclassification to frontier market status. The distinction determines whether Indonesia remains in indices that drive billions in passive allocation or shifts to a lower tier with reduced investor access.

Analyst Wilbert Arifin at Mirae Asset Sekuritas Indonesia characterised the reforms as a “modest net positive” that lowers the risk of downgrade. The phrasing is careful. The reforms signal constructive regulatory engagement, but they do not guarantee retention. MSCI’s decision will weigh the regulatory framework against actual compliance and enforcement.

The US$190 billion market value lost since January reflects capital already repositioning. Active selling of tycoon-linked stocks occurred throughout Q1 2026, according to available reports. The June decision determines whether that selling was premature or prescient.

Three potential outcomes frame the decision:

Investors with Indonesian exposure face asymmetric information. Active managers have already repositioned away from tycoon-linked stocks. Passive funds tracking MSCI indices will rebalance mechanically based on the June outcome, creating a timing gap between active and passive flows.

No comprehensive Q1 2026 capital flow data is available in current reports, limiting visibility into the scale of repositioning already completed. The distinction between passive outflow risk (index-driven) and active reallocation (discretionary) matters for timing. Passive outflows arrive in concentrated waves tied to index reconstitution dates. Active reallocation happens continuously as managers reassess risk.

The June announcement is the definitive moment, but the capital movement surrounding it has already begun.

For investors holding Indonesian exposure who need to assess whether the June MSCI decision warrants portfolio adjustments, our comprehensive guide to investing during market volatility walks through rebalancing frameworks, country risk assessment criteria, and tactical allocation strategies for navigating index-driven price dislocations.

MSCI’s removal of Barito Renewables and DSS reflects mechanical application of free float standards, not arbitrary punishment. The 97.3% and 95.76% ownership concentrations left no discretion once the data became public. Indonesia’s regulatory package, doubling free float requirements to 15% and tightening disclosure thresholds to 1%, demonstrates willingness to engage with global standards.

Whether that engagement translates to actual compliance remains the question the June review will answer. The three-year transition window gives companies runway, but MSCI’s decision will assess the framework itself, not wait for company-level execution. The US$190 billion market value erosion since January signals that capital is not waiting either.

The capital reallocation between developed and emerging markets accelerated in Q1 2026 as geopolitical risk and governance concerns shifted flows toward US and European equities, with emerging market outflows concentrating in countries facing index reclassification risk.

Investors holding Indonesian exposure through MSCI-tracking funds should monitor the June announcement and assess their positions in context of the three classification scenarios. The reforms reduce downgrade risk. They do not eliminate it.

MSCI is reviewing whether Indonesia should be reclassified from emerging market to frontier market status, a change that would remove the country from indices tracking trillions in passive capital and trigger broad outflows from Indonesian equities.

Both companies breached MSCI's free float standards due to extreme ownership concentration, with Barito Renewables at 97.3% and DSS at 95.76% held by controlling interests, leaving international investors with virtually no tradeable shares.

In early April 2026, Indonesia doubled its minimum free float requirement from 7.5% to 15%, tightened ownership disclosure thresholds from 5% to 1%, and granted existing listed companies a three-year window to comply with the new standards.

Indonesia's equity market has lost approximately US$190 billion in market value since MSCI issued its warning in January 2026, reflecting capital repositioning ahead of the June review decision.

MSCI could maintain Indonesia's emerging market status under ongoing watch, remove additional stocks from indices without a full downgrade, or fully reclassify Indonesia to frontier market status, with the last scenario triggering the most severe passive outflows.