Affirm Stock Forecast: Analyst Upgrades Signal 27% Upside Ahead

Key Takeaways

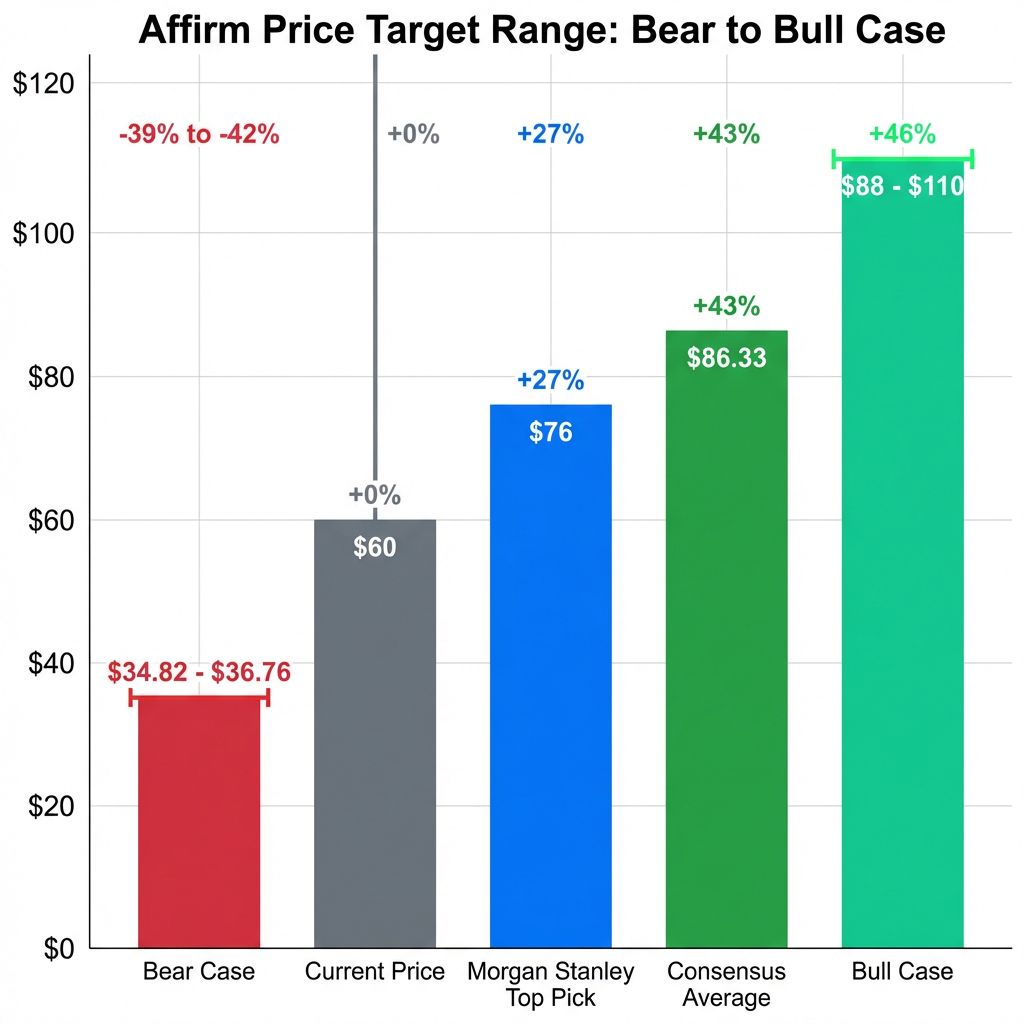

- Morgan Stanley elevated Affirm to Top Pick status with a $76 price target, implying 27% upside potential from current levels as of 17 April 2026.

- Affirm posted its first-ever GAAP profit in Q1 2026, recording $130 million net income on $1.1 billion revenue, validating its shift to profitable expansion.

- Q2 FY26 gross merchandise volume reached $13.8 billion, representing 36.6% year-over-year growth, with Morgan Stanley expecting 30%+ rates to persist through fiscal 2027.

- The Amazon partnership, extended through January 2031, eliminates near-term renewal risk and anchors a substantial portion of Affirm's GMV growth trajectory.

- The wide analyst price target range of $50 to $110 reflects genuine uncertainty about valuation multiples and growth sustainability, warranting careful position sizing.

Affirm Holdings stock surged 3.5% in premarket trading on 17 April 2026 after Morgan Stanley elevated the buy now pay later provider to Top Pick status with a $76 price target. Analyst James Faucette’s upgrade signals growing institutional confidence in Affirm’s ability to sustain 30%+ growth rates whilst dismissing private credit concerns as overblown. The $76 target implies 27% upside potential from current levels, representing one of Wall Street’s most bullish near-term endorsements for the recently profitable fintech.

The upgrade adds institutional weight to an already constructive analyst consensus. With 24 Buy ratings and an average price target of $86.33, Wall Street broadly expects continued appreciation for AFRM shares. Morgan Stanley’s Top Pick designation distinguishes Affirm from peers, positioning the company as a preferred vehicle for capturing growth in the digital lending space.

> Morgan Stanley’s $76 price target implies 27% upside potential for Affirm shareholders, with the firm designating AFRM as a Top Pick for 2026.

The premarket gain reflects immediate investor response to Morgan Stanley’s validation of Affirm’s transition from growth-at-any-cost to profitable expansion. Markets appear increasingly willing to reward the company’s demonstrated ability to balance rapid gross merchandise volume growth with improving unit economics.

Understanding Affirm’s Buy Now Pay Later Business Model

Affirm generates revenue through two primary channels: merchant fees charged at point of sale and interest payments from consumers who select instalment plans. The company differentiates itself through transparent pricing with no late fees, contrasting with traditional credit card models that rely on penalty charges and revolving balances.

The CFPB interpretive rule establishing BNPL consumer protections requires companies like Affirm to provide the same safeguards as traditional credit card issuers, including dispute resolution and refund rights. This regulatory framework reinforces Affirm’s positioning as a compliant and consumer-protective alternative to traditional revolving credit models.

Gross Merchandise Volume (GMV) serves as the key growth metric, representing the total dollar value of transactions processed through Affirm’s platform. The Amazon partnership, extended through January 2031, provides significant revenue visibility and validates Affirm’s competitive positioning. This long-term commitment with one of the world’s largest e-commerce platforms anchors a substantial portion of GMV growth, reducing execution risk for investors evaluating the Affirm stock forecast.

When big ASX news breaks, our subscribers know first

Wall Street Price Targets and Analyst Consensus

The analyst community shows broad bullish conviction, with 24 firms maintaining Buy ratings on Affirm shares. The consensus $86.33 price target sits well above current levels, though the wide range of $50 to $110 reflects genuine disagreement about appropriate valuation multiples for a newly profitable BNPL company. Recent rating activity tilts decisively positive, with 4 upgrades versus 1 downgrade over the prior 90 days.

Morgan Stanley’s $76 target implies approximately 24x fiscal year 2028 GAAP earnings per share, a methodology that applies traditional valuation frameworks to Affirm’s improving profitability trajectory. The firm’s analysis suggests the market underappreciates the company’s ability to expand margins whilst maintaining elevated growth rates.

| Forecast Scenario | Price Target | Implied Change | Timeframe |

|---|---|---|---|

| Morgan Stanley Top Pick | $76 | +27% | 2026 |

| Consensus Average | $86.33 | +43% | 2026 |

| Bull Case | $88 | +46% | June 2028 |

| Bear Case | $34.82-$36.76 | -39% to -42% | End 2026 |

The $50 to $110 range illustrates fundamental uncertainty about sustainable growth rates and appropriate valuation frameworks. Bears question whether 30%+ GMV expansion can persist beyond 2026, whilst bulls argue the Amazon partnership and improving unit economics justify premium multiples.

Growth Catalysts Supporting the Bullish Thesis

Affirm achieved a watershed moment in Q1 2026 by posting its first GAAP profit, recording $130 million net income on $1.1 billion revenue. This profitability inflection validates the business model and fundamentally alters the investment thesis, shifting the narrative from speculative growth story to established fintech with proven unit economics. The milestone demonstrates Affirm can scale whilst improving margins, addressing longstanding investor concerns about path to profitability.

Affirm’s achievement mirrors a broader industry trend, with multiple consumer lending platforms reaching profitability in 2026. Wisr’s recent cash NPAT profit demonstrates that the path from growth-focused to earnings-positive operations is achievable across geographies and market segments, reinforcing that Affirm’s milestone reflects sector-wide unit economics maturation rather than an isolated event.

Multiple near-term catalysts support continued upside potential:

- Sustained GMV expansion: Q2 FY26 GMV reached $13.8 billion, representing 36.6% year-over-year growth, with Morgan Stanley expecting 30%+ growth rates to persist through fiscal 2027

- Margin improvement trajectory: Potential guidance increase to 3.5%-4.0% retained loan/transaction margin would signal operational leverage gains

- FY2028 earnings visibility: Expected GAAP EPS target of $2.50-$3.00 provides medium-term profitability framework, which Morgan Stanley views as notably conservative

- May Investor Forum catalyst: Upcoming management presentation represents near-term opportunity for guidance updates and strategic clarity

- Amazon partnership security: Extension through 2031 eliminates material partnership renewal risk and ensures GMV foundation

Collectively, these factors create a compelling case for multiple expansion. The combination of first GAAP profit with sustained 30%+ growth addresses the primary valuation debate, potentially justifying premium multiples historically reserved for mature profitable tech companies.

Private Credit Concerns: Separating Fact from Fear

Morgan Stanley explicitly characterised private credit concerns as exaggerated, directly challenging the primary bear case against Affirm shares. Some investors worried that tightening credit conditions could restrict Affirm’s ability to fund consumer loans through asset-backed securities markets, potentially constraining growth or forcing margin compression.

Understanding how other fintech lenders structure funding provides context for Affirm’s capital strategy. Plenti’s recent $400 million ABS transaction demonstrates continued investor appetite for consumer lending asset-backed securities despite macro concerns, with the deal achieving record-low pricing and the highest investor turnout in the company’s history.

> Asset-backed securities market data shows stable funding conditions: 2-year spreads remain steady at 80 basis points, whilst 3-year spreads narrowed from 100 to 95 basis points.

Morgan Stanley’s counterargument emphasises that competitors with weaker credit track records successfully secured forward flow funding arrangements, demonstrating the market remains accessible to well-positioned BNPL providers. According to the firm’s analysis, Affirm’s improving credit performance and established funding relationships position the company favourably relative to sector peers. Whilst funding risks exist in any credit-dependent business model, current market evidence doesn’t support positioning for material capital access constraints.

The Federal Reserve analysis of BNPL credit performance provides institutional research on borrower financial health and default trends across the sector. This data offers authoritative context for evaluating the asset-backed securities funding mechanisms and credit quality metrics that underpin lending operations for companies like Affirm.

Investment Considerations and Risk Factors

Despite bullish catalysts and improving fundamentals, investors should weigh material risks that could derail the positive thesis. The $50 to $110 price target range reflects genuine analyst disagreement about sustainable growth rates, appropriate valuation multiples, and execution risk on margin expansion targets.

Key risk factors include:

- Valuation uncertainty: Bear case scenarios project -39% to -42% downside by end of 2026, suggesting some analysts view current levels as overvalued relative to growth sustainability

- Macroeconomic sensitivity: Consumer credit performance could deteriorate if unemployment rises or discretionary spending weakens, impacting both GMV growth and credit losses

- Competitive pressure: Klarna and Block’s Afterpay possess significant resources and merchant relationships, potentially constraining Affirm’s market share gains

- Amazon concentration risk: Whilst the partnership extends through 2031, material dependence on a single merchant creates strategic vulnerability

- Execution risk: Achieving 3.5%-4.0% margin targets requires successful operational improvements that may prove challenging at scale

The competitive landscape continues evolving rapidly, with some BNPL players like Ovanti pivoting beyond single-product offerings toward broader financial services platforms. These strategic shifts illustrate how competitors are adapting to market pressures and seeking differentiation through multi-product expansion versus focused specialization.

Position sizing should reflect this uncertainty. The May Investor Forum may provide clarity on several risk factors, particularly regarding margin trajectory and FY2028 earnings visibility.

The next major ASX story will hit our subscribers first

Bottom Line: What the Affirm Stock Forecast Means for Investors

Morgan Stanley’s upgrade to Top Pick with a $76 target adds meaningful institutional validation to an already constructive Wall Street consensus. With 24 Buy ratings averaging $86.33, analyst sentiment strongly favours continued appreciation for Affirm shares. The company’s first GAAP profit in Q1 2026 combined with 36.6% GMV growth in the most recent quarter supports the case for sustained upside, whilst the extended Amazon partnership through 2031 provides revenue foundation. The May Investor Forum represents the next near-term catalyst for guidance updates and strategic clarity. However, the wide $50 to $110 forecast range illustrates genuine uncertainty about valuation multiples and growth sustainability, suggesting position sizing should account for material risk alongside compelling reward potential.

Frequently Asked Questions About Affirm Stock

What is the average analyst price target for Affirm stock in 2026?

The consensus price target from 24 analysts stands at $86.33, with individual forecasts ranging from $50 to $110. Morgan Stanley’s recent Top Pick upgrade established a $76 target, representing 27% upside potential from current levels. The $86.33 average implies 43% appreciation from the $60 reference price, though the wide range reflects genuine disagreement about appropriate valuation multiples for a newly profitable BNPL company.

Is Affirm profitable?

Affirm achieved its first GAAP profit in Q1 2026, recording $130 million net income on $1.1 billion revenue. This profitability milestone represents a fundamental inflection point for the investment thesis, validating the business model’s ability to generate earnings whilst maintaining 30%+ revenue growth. The achievement shifts analyst focus from path-to-profitability concerns to margin expansion trajectory and sustainable earnings power, materially improving institutional sentiment.

What are the main risks to Affirm’s stock forecast?

Primary risks include valuation uncertainty, with bear case scenarios projecting -39% to -42% downside by end of 2026. Private credit funding concerns persist despite Morgan Stanley’s dismissal of these fears, as tightening capital markets could constrain growth. Competitive pressure from Klarna and Block’s Afterpay represents ongoing market share risk. Macroeconomic sensitivity creates vulnerability to consumer spending weakness or rising unemployment, potentially impacting both GMV growth and credit performance.

When is Affirm’s next major catalyst event?

The May 2026 Investor Forum represents the next significant catalyst, providing management opportunity to update GMV guidance, margin targets, and strategic priorities. Analysts expect potential announcements regarding the fiscal year 2028 GAAP EPS target of $2.50-$3.00, which Morgan Stanley views as conservative. The forum may also address private credit market conditions and competitive positioning, offering investors clarity on key thesis debate points.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

What is the Affirm stock forecast for 2026?

The consensus price target from 24 analysts stands at $86.33, implying approximately 43% upside, with individual forecasts ranging from $50 to $110. Morgan Stanley's Top Pick upgrade set a $76 target, representing 27% upside from current levels.

Why did Morgan Stanley upgrade Affirm stock to Top Pick?

Morgan Stanley analyst James Faucette upgraded Affirm to Top Pick status with a $76 price target, citing the company's ability to sustain 30%+ growth rates, its first GAAP profit of $130 million in Q1 2026, and dismissing private credit funding concerns as overblown.

Is Affirm stock profitable?

Yes, Affirm achieved its first GAAP profit in Q1 2026, recording $130 million net income on $1.1 billion in revenue, representing a major inflection point that shifts the investment narrative from speculative growth to proven unit economics.

What are the biggest risks to the Affirm stock forecast?

Key risks include bear case price targets projecting 39% to 42% downside by end of 2026, macroeconomic sensitivity to consumer spending, competitive pressure from Klarna and Block's Afterpay, and concentration risk from the Amazon partnership accounting for a significant share of GMV.

What is the next major catalyst for Affirm stock?

The May 2026 Investor Forum is the next significant near-term catalyst, where management is expected to update GMV guidance, margin targets, and potentially clarify the fiscal year 2028 GAAP EPS target of $2.50 to $3.00, which Morgan Stanley views as conservative.