APA Group lifts earnings and margins in strong 1H26 performance

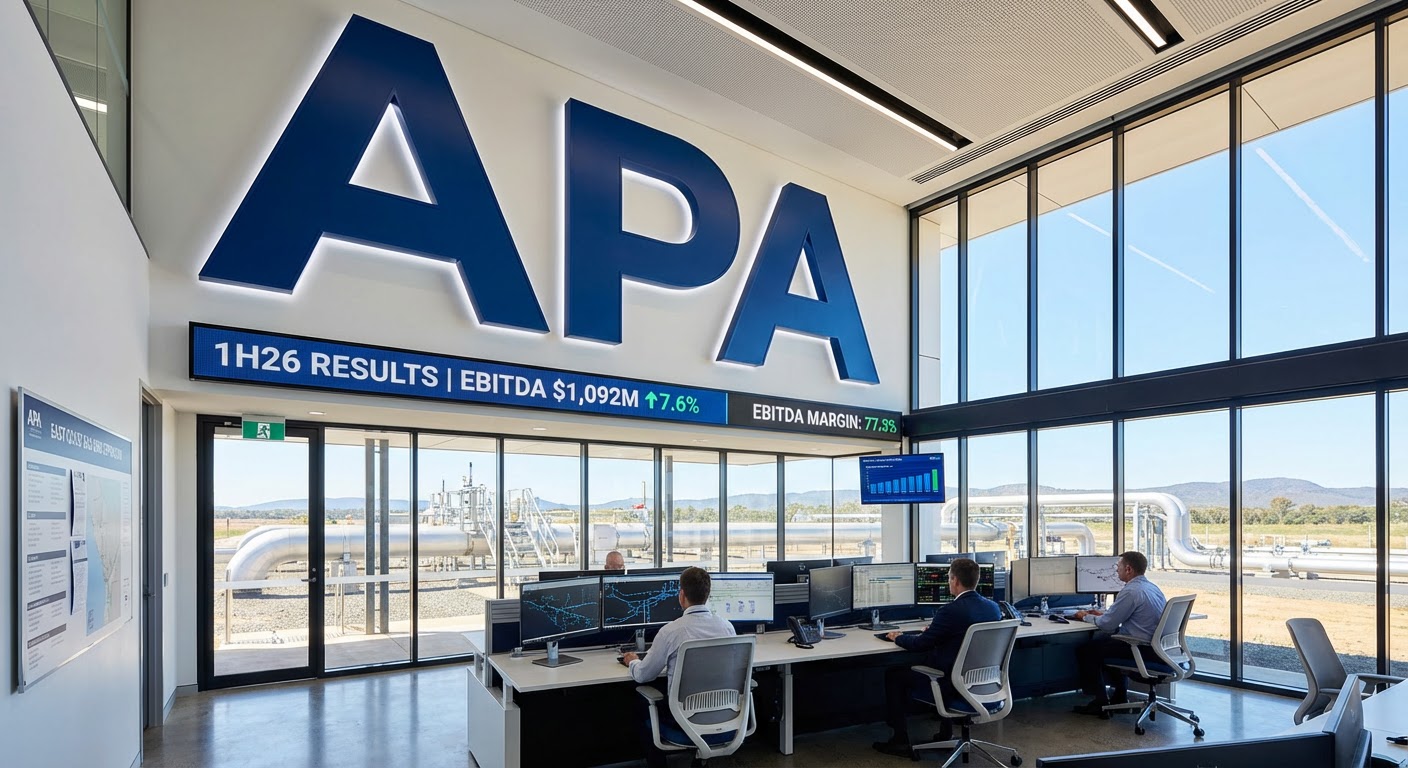

APA Group (ASX: APA) has reported APA Group 1H26 Financial Results that demonstrate strong operational execution, with Underlying EBITDA rising 7.6% to $1,092 million for the half year ended 31 December 2025. The result was driven by inflation-linked tariff escalation, contributions from recently commissioned assets, and enterprise-wide cost reduction initiatives that saw corporate costs fall 13.6% compared to the prior corresponding period.

EBITDA margins expanded to 77.3%, an increase of 280 basis points on 1H25, reflecting the company’s disciplined cost management and the high-margin nature of its infrastructure assets. Total statutory revenue (excluding pass-through revenue) increased 2.0% to $1,391 million, whilst statutory net profit after tax lifted to $95 million from $34 million in 1H25, supported by EBITDA growth and lower net interest expense.

New asset contributions came from the Kurri Kurri Lateral Pipeline, Port Hedland Solar and Battery Project, and the Atlas to Reedy Creek Pipeline, all of which commenced operations during the reporting period.

| Metric | 1H26 | 1H25 | Change |

|---|---|---|---|

| Underlying EBITDA | $1,092 million | $1,015 million | +7.6% |

| EBITDA Margin | 77.3% | 74.5% | +280bps |

| Statutory Revenue | $1,391 million | $1,364 million | +2.0% |

| Statutory NPAT | $95 million | $34 million | +179% |

| Corporate Costs | Not disclosed | Not disclosed | -13.6% |

When big ASX news breaks, our subscribers know first

What drives APA’s earnings? Understanding inflation-linked infrastructure

For investors unfamiliar with the energy infrastructure sector, APA’s business model centres on owning and operating critical gas transmission pipelines and electricity assets that benefit from long-term contracted revenue streams. The company operates more than 15,000 kilometres of gas pipelines, delivering approximately half of Australia’s domestic gas supply.

A key characteristic of APA’s revenue base is inflation-linked tariff escalation. Many of the company’s contracts contain clauses that automatically adjust tariffs in line with inflation indices, providing earnings visibility and natural protection against rising costs. This mechanism explains why periods of elevated inflation can support margin expansion, particularly when combined with operational efficiency gains.

The gas transmission business also typically features “take-or-pay” contract structures, where customers commit to paying for pipeline capacity regardless of whether they fully utilise it. This creates a stable, predictable cash flow profile that is less exposed to volume fluctuations than many other infrastructure businesses.

Investment significance: APA’s regulated and contracted revenue base provides defensive earnings characteristics with built-in inflation protection, a key consideration for income-focused investors seeking exposure to essential infrastructure with predictable distributions.

Organic growth pipeline expands to approximately $3 billion

APA’s organic growth pipeline for FY26-FY28 has increased from $2.1 billion to approximately $3 billion, reflecting accelerated momentum in the company’s growth strategy. The expansion includes progression of Stage 3 of the East Coast Gas Grid Expansion Plan, with Stage 3A reaching final investment decision and Stage 3B subject to final board approval.

The company is also developing the Brigalow Peaking Power Plant in partnership with CS Energy, though this project remains conditional and subject to necessary external and government approvals, finalisation of development matters, and entry into full form documentation.

A positive regulatory outcome was achieved for the Bulloo Interlink, a critical component of the East Coast Gas Grid Expansion Plan. The asset will be subject to a lighter form of regulation upon commissioning and is exempt from heavy regulation for at least 10 years, supporting the project’s commercial returns.

Funding for the growth pipeline will come from existing balance sheet capacity and the Distribution Reinvestment Plan (DRP). A recent S&P rating agency threshold modification has provided more than $1 billion of funding capacity, with the FFO/Net Debt threshold modified from 9.5% to 8.5%. APA’s BBB (stable) long-term credit rating was confirmed as part of this review.

Key growth projects:

- Kurri Kurri Lateral Pipeline (commissioned)

- Port Hedland Solar and Battery Project (commissioned)

- Atlas to Reedy Creek Pipeline (commissioned)

- Brigalow Peaking Power Plant (in development)

- East Coast Gas Grid Expansion Plan Stage 3 (progressing)

Simplification strategy progresses

APA has made progress on its simplification strategy, agreeing to divest its Networks business and its 20% interest in GDI. Both transactions remain subject to conditions precedent. The divestments align with management’s stated focus on core infrastructure assets that deliver returns well above APA’s cost of capital, improving portfolio quality and freeing up capital for higher-return opportunities.

The next major ASX story will hit our subscribers first

Distribution and outlook for FY26

The Board has resolved to pay an interim distribution for 1H26 of 27.5 cents per security, representing a 1.9% increase on the 1H25 interim distribution of 27.0 cents per security. The distribution comprises 21.42 cents per security from APA Infrastructure Trust (including a fully franked profit distribution of 6.30 cents and a capital distribution of 15.12 cents) and 6.08 cents per security from APA Investment Trust (including an unfranked profit distribution of 1.10 cents and a capital distribution of 4.98 cents).

The distribution is expected to be paid on 18 March 2026. The Distribution Reinvestment Plan operated at a discount of 1.5% for this interim distribution.

FY26 distribution guidance has been reaffirmed at 58.0 cents per security, representing a 1.8% increase on FY25. FY26 Underlying EBITDA guidance remains unchanged at $2,120 million to $2,200 million, with management now expecting to exceed the midpoint of this range.

Free Cash Flow for 1H26 was $556 million, up 0.7%, with growth in Underlying EBITDA partly offset by higher interest and tax, and one-off timing impacts related to the divestment of the Networks business.

Adam Watson, CEO and Managing Director

“Today’s result demonstrates that APA is delivering on commitments, while simultaneously positioning the business to play a central role in the energy transition. This result highlights APA’s disciplined execution against our strategy and the sustained focus on long-term value creation for our securityholders.”

Investment thesis: why this matters for APA shareholders

The APA Group 1H26 Financial Results demonstrate the company is executing on multiple fronts simultaneously: delivering earnings growth and margin expansion whilst scaling its growth pipeline and strengthening its balance sheet. The 280 basis point margin improvement validates management’s cost reduction programme, which is on track to achieve the full year target of $50 million in savings.

The S&P threshold modification is particularly significant, providing validation of APA’s earnings quality whilst creating more than $1 billion in additional funding capacity without requiring equity issuance. This positions the company to pursue growth opportunities on its own terms, maintaining financial flexibility as the organic pipeline scales.

For investors, the result reinforces APA’s positioning as a defensive infrastructure play with growth optionality. The company’s gas transmission assets remain critical during Australia’s energy transition, providing baseload capacity whilst renewable generation scales. The expanded growth pipeline, supported by a strengthened balance sheet, provides confidence in the sustainability of distribution growth beyond FY26.

Investment significance: APA’s 1H26 result demonstrates the company is executing on cost reduction while simultaneously scaling its growth pipeline, supported by an enhanced balance sheet capacity that provides optionality for capital deployment without compromising the BBB credit rating or distribution trajectory.

Stay Ahead on Utilities and Infrastructure News

Join 20,000+ investors receiving FREE breaking ASX news delivered within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at Big News Blast to get real-time alerts on market-moving announcements the moment they break.