Nvidia Set to Reveal First Windows PC Processors at Computex

54 mins ago

US digital health funding surged to $14.2 billion in 2025, a 35% year-over-year increase driven by AI mega-deals worth hundreds of millions of dollars each. Yet the companies capturing those rounds are already formed, already staffed, already producing revenue or clinical data. The researchers sitting on promising healthcare AI discoveries in university labs, the people who could become the next generation of founders, often never make it that far. The gap between a laboratory breakthrough and a company that venture capital will fund is not a minor inconvenience. It is a structural feature of the healthcare innovation funding ecosystem, one that the industry refers to as the “valley of death.” This explainer breaks down why early-stage healthcare ideas stall before reaching traditional investors, how pre-company investment models work, and what the launch of Treehub by AI Health Fund on 22 April 2026 reveals about where the market is heading.

A researcher develops a clinical AI model that shows early promise in a university setting. The natural next step, turning it into a product, requires capital, commercial guidance, and access to the healthcare operators who would eventually buy it. The researcher typically has none of these.

This is the valley of death: the period between an academic discovery and a startup that is structured enough for traditional venture capital to consider funding it. The gap exists not because the research is weak, but because the infrastructure connecting research to commercialisation is absent at the earliest stage.

NIH translatability research on biomedical AI, published in JAMA Network Open, found that the majority of NIH-funded studies applying artificial intelligence to clinical problems did not produce outputs that moved into practical healthcare use, providing peer-reviewed confirmation that the translation gap is a documented structural phenomenon rather than an anecdotal concern.

An investor panel at the Advanced Therapies 2026 conference noted that this gap is “particularly acute in biotech, where early planning and investor trust are essential to bridge academic research to viable ventures.”

The problem compounds across three dimensions:

Roughly $60 billion has flowed into healthcare AI over the past decade, with approximately $30 billion deployed in the last three years alone. Capital at later stages is abundant. Capital at the moment a researcher needs it most is not.

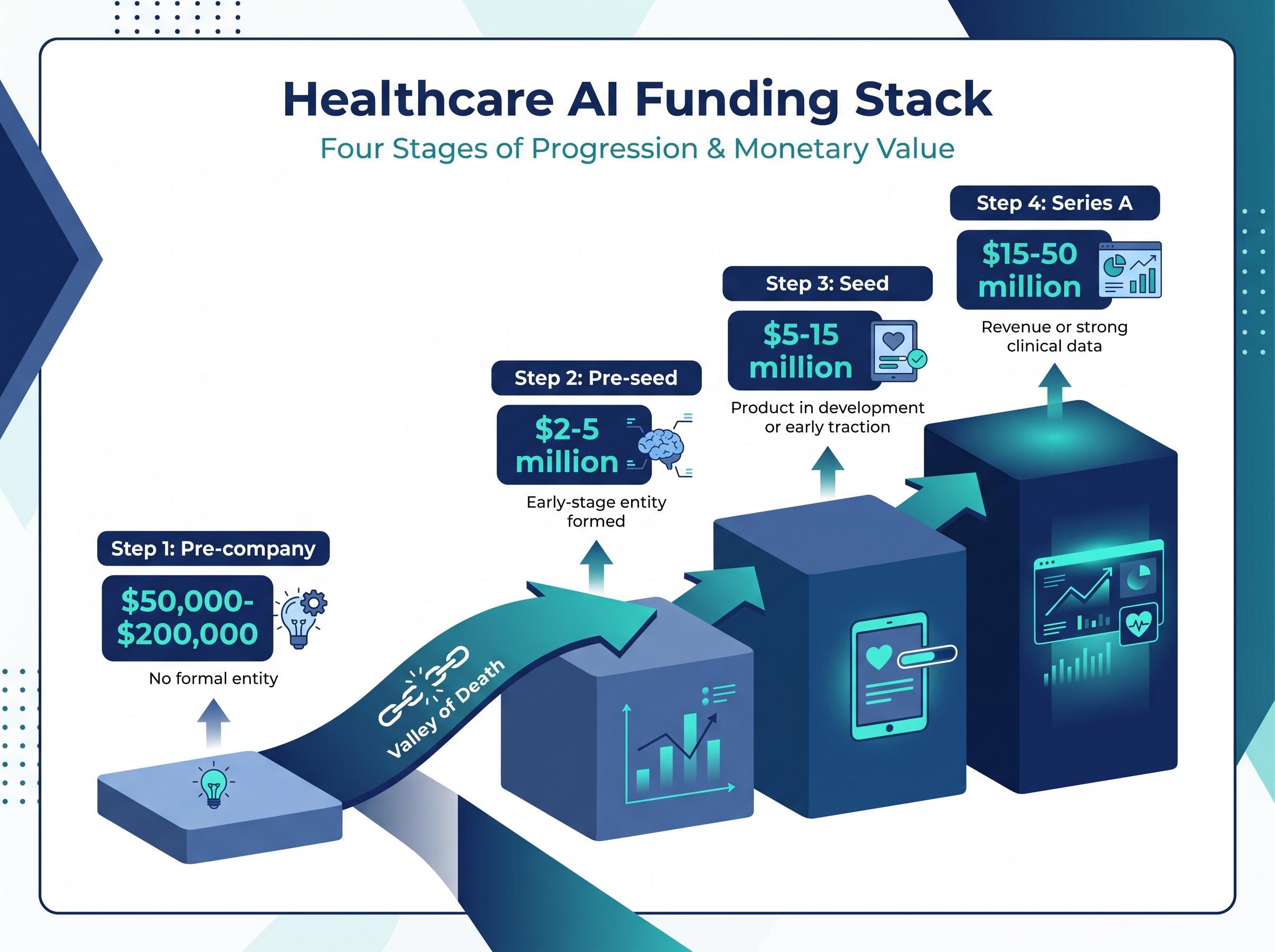

Pre-company investment is capital deployed before a formal entity exists. There is no incorporated startup, no cap table, no legal structure. The money funds the transition from research concept to something that could become a company, which distinguishes it from a pre-seed round, where at least a minimal corporate entity is already in place.

A $100,000 check at this stage is not arbitrarily small. Pre-company bridging checks typically fall in the $50,000-$200,000 range, making this figure calibrated to the stage rather than a token gesture. The scale gap becomes visible when compared to pre-seed rounds in US healthcare AI, which averaged $2-5 million in 2024-2025 according to CB Insights Q3 2025 data.

The table below maps where pre-company capital sits relative to the stages that follow it.

| Stage | Typical Check Size | Company Status | Primary Capital Source |

|---|---|---|---|

| Pre-company | $50,000-$200,000 | No formal entity | Bridging funds, specialised programmes |

| Pre-seed | $2-5 million | Early-stage entity formed | Angel investors, micro-VCs |

| Seed | $5-15 million | Product in development or early traction | Seed-stage venture capital |

| Series A | $15-50 million | Revenue or strong clinical data | Institutional venture capital |

The $14.2 billion that flowed into US digital health in 2025 concentrated overwhelmingly in post-formation, post-product companies, confirming that the early pre-company stage remains systemically undercapitalised relative to the overall market.

Pre-company checks may or may not take equity, and the terms vary significantly from traditional accelerator models. Accelerators typically invest in exchange for a fixed equity percentage in an existing company. The AI Health Fund model is designed for pre-formation participants, positioning it closer to a research grant with commercial intent than to a conventional equity-for-access arrangement.

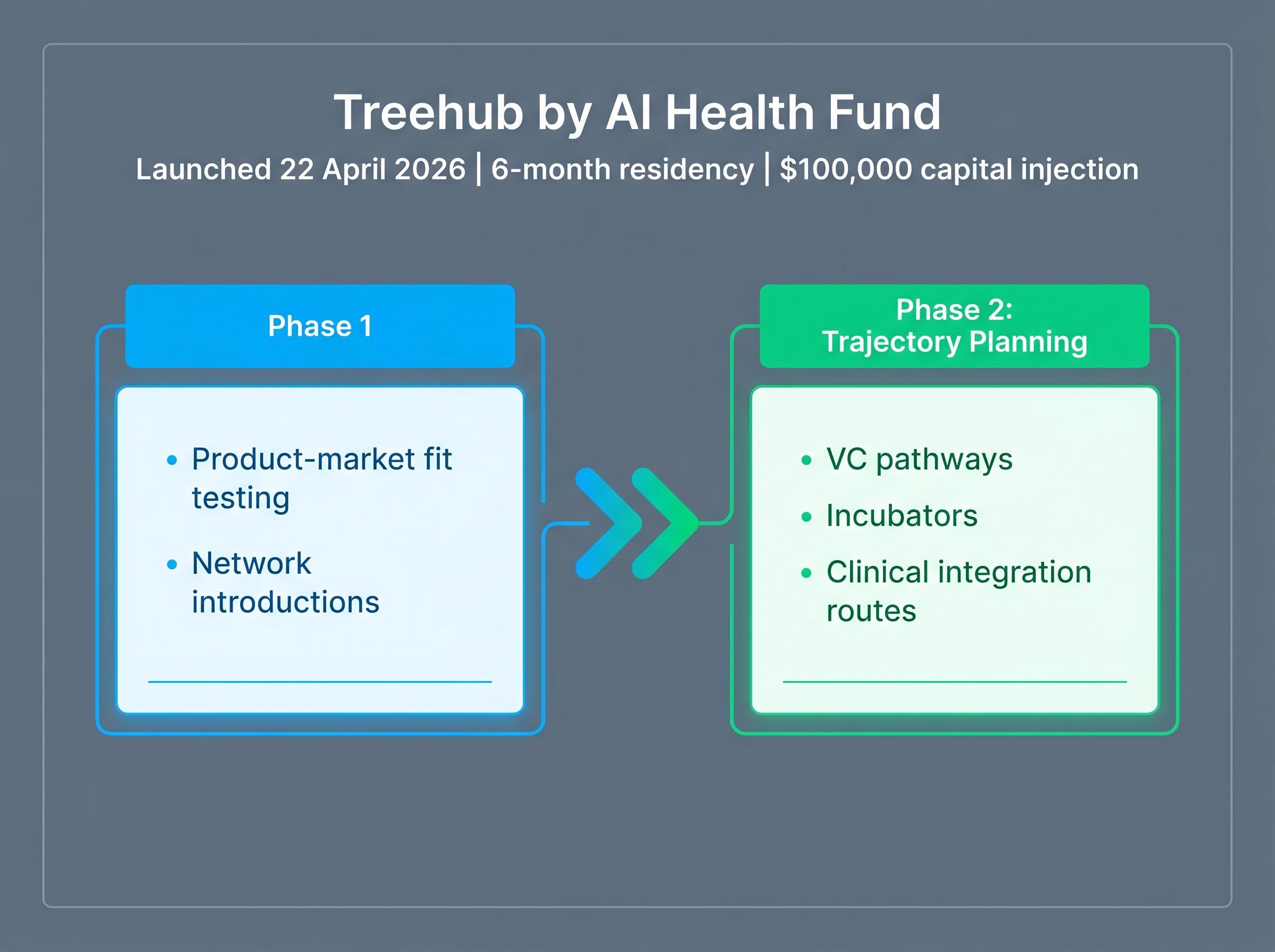

Treehub by AI Health Fund launched on 22 April 2026 with a structure built around quarterly cohorts, each running for six months. Participants receive a $100,000 early capital injection from the fund. The programme unfolds in two distinct phases.

Founding partner Mary Minno, a former Google employee, designed the programme as a structural response to systemic healthcare inefficiencies she identified during her time in technology. Her background shaped a model that emphasises operational infrastructure alongside capital, rather than treating funding as the sole barrier.

The programme’s backers reflect a specific thesis about healthcare innovation. Tim Draper commented publicly in September 2025 on systemic flaws in US healthcare spending and the pharmaceutical market, aligning with the fund’s premise that incumbent structures fail early-stage innovators. Anne Wojcicki provided written testimony before a House oversight committee in June 2025 on biotech investments and healthcare innovation policy, reflecting continued engagement with early-stage ecosystems.

Four companies currently sit in the AI Health Fund portfolio. Each illustrates a different dimension of what healthcare AI looks like at the pre-formation stage.

| Company | Focus Area | Stage Description |

|---|---|---|

| Diggy | Behavioural tracking for clinical autism intervention | Expanding Dennis Wall’s academic research into a platform |

| Clair Health | Continuous hormonal monitoring | Pre-formation, technology in early development |

| Nestwell | Residential environment health assessment | Pre-formation, evaluating how living spaces affect physical health |

| Korda | Predictive patient health trajectory modelling | Pre-formation, software identifying potential long-term complications |

The thematic thread connecting these four is breadth within clinical AI rather than concentration in a single subsector. Diagnostics, behavioural tracking, hormonal monitoring, environmental health, and predictive modelling all appear, suggesting the fund’s thesis is stage-specific (pre-formation healthcare AI) rather than disease-specific.

These companies cannot be independently verified through public sources. They represent early-stage ventures not yet publicly announced, consistent with the pre-formation positioning the fund is designed to serve.

The timing of Treehub’s launch is not coincidental. Three macro conditions are converging to create demand for pre-company programmes in healthcare AI.

AI-enabled startups captured approximately 54% of all US digital health venture funding on a full-year 2025 basis, according to Rock Health and Fierce Healthcare.

That concentration makes the structural gap more visible, not less. When the majority of capital flows to companies that already have products, clinical data, and revenue trajectories, the distance between a promising research concept and a fundable startup widens.

Three factors are sharpening the problem simultaneously:

The valuation pressure at later stages is creating a secondary incentive for institutional investors to move earlier: pre-incorporation models in healthcare VC allow funds to secure intellectual property positions before formal corporate structures exist, bypassing the 19% AI valuation premium that defined 2025 deal pricing.

STAT News reporting on the early-stage biotech funding gap noted that seed and Series A capital in life sciences fell to its lowest level in a decade during 2025, a contraction that occurred simultaneously with record aggregate investment totals, illustrating precisely how later-stage concentration can coexist with acute scarcity at the formation stage.

No comparable accelerator models featuring quarterly cohorts with explicit pre-company investments in healthcare AI were identified in available sources, positioning Treehub as early in an emerging niche rather than entering a crowded category.

Investors exploring how the capital concentration described above is playing out across the broader market in real time will find our full breakdown of Q1 2026 health tech investment trends, which examines the $4 billion raised in the quarter, the subsectors attracting the earliest-stage dollars, and the clinical validation benchmarks investors are now applying at entry.

Treehub launched eight days ago. Its portfolio companies are pre-public. The model’s effectiveness at bridging research to commercial healthcare AI has not yet been demonstrated at scale, and honest assessment requires acknowledging this directly.

Roughly $30 billion has flowed into healthcare AI over the past three years, yet clinical AI subsectors still show low commercial maturity. That unresolved tension is precisely what programmes like this are positioned to address. Tim Draper’s September 2025 commentary on systemic flaws in US healthcare spending provides context for why investor-backed, operationally focused pre-company programmes represent a different bet than pure capital deployment. The premise is that the problem is not just money; it is infrastructure, guidance, and structured access to the commercial healthcare system.

Clinical AI deployment at scale, illustrated by ventures like Echo IQ embedding decision-support software into major US health systems, represents the commercial endpoint that pre-formation companies are ultimately building toward, and the gap between a researcher’s prototype and that level of institutional integration is precisely what programmes like Treehub are designed to close.

If the model works, it represents a structural fix for the valley of death that philanthropy and government grants have historically struggled to deliver. If it does not, the gap between research and commercialisation remains as wide as it was before $14.2 billion flowed into the sector last year.

Two measurable outcomes will determine whether the model delivers on its premise. The first is the proportion of cohort companies that proceed to formal VC rounds, the clearest signal that pre-company capital and guidance translated into investor-ready ventures. The second is whether clinical outcomes data from portfolio companies eventually satisfies the ROI demands that later-stage investors now require.

Comparable data from Y Combinator and Techstars healthcare tracks exists but lacks verified post-2025 figures confirming this specific pre-company structure. Treehub operates without an established benchmark, which means its early cohorts will effectively create one.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and company performance.

The valley of death refers to the funding gap between an academic research breakthrough and a startup structured enough for traditional venture capital to consider investing in it. It exists because pre-formation researchers typically lack capital, commercial guidance, and access to healthcare operators who would buy their product.

Pre-company investing deploys capital before any formal entity exists, meaning there is no incorporated startup, cap table, or legal structure in place. A pre-seed round, by contrast, already involves at least a minimal corporate entity and typically raises $2-5 million, far above the $50,000-$200,000 range of pre-company bridging checks.

Treehub provides a six-month residency structured in two phases: the first focuses on product-market fit testing and introductions to health networks, payers, and operators, while the second covers VC pathways, incubator options, and clinical integration routes. Each participant also receives a $100,000 capital injection from the fund.

The largest 2025 rounds, including Abridge at $300 million and OpenEvidence at $210 million, went to companies with existing products, clinical data, and revenue. AI companies also commanded a 19% valuation premium over non-AI digital health rounds in 2025, further directing capital toward established ventures rather than early-stage researchers.

The two clearest indicators are the proportion of cohort companies that proceed to formal VC rounds and whether portfolio companies eventually generate clinical outcomes data that satisfies the ROI demands of later-stage investors. Treehub launched in April 2026 and its early cohorts will effectively establish the benchmark, as no directly comparable model with verified post-2025 data currently exists.