Aland Equity Group Ltd Locks in Chinnerys Funding Rights Over 3,200 Lots

AEG locks in funding rights over 3,200-lot Chinnerys development in Canberra growth corridor

Aland Equity Group Limited (ASX: AEG) has executed a Property Funding Deed over the Chinnerys master-planned residential development in Bungendore, NSW, described in the announcement as “the largest and most strategically significant asset in AEG’s property pipeline.”

The deal provides long-term property funding rights over approximately 3,200 mixed residential lots across a 1,000 acre landholding. It replaces the Heads of Agreement announced on 19 May 2026, and remains subject to shareholder approval under ASX Listing Rule 10.1.

The land is owned by an entity associated with AEG Chairman, Mr. Alex Brinkmeyer. As consideration, 60 million AEG shares are to be issued to Mr. Brinkmeyer, contingent on that shareholder approval being obtained.

Deal at a glance

-

10 + 10 year exclusive term secured by mortgage, caveat and power of attorney

-

30% gross profit margin (Development Margin) incorporated into Fund acquisition pricing

-

Equates to approximately $174,000 per lot based on comparable sales over the last five years

-

60 million AEG shares to be issued to Mr. Brinkmeyer as consideration, subject to shareholder approval under ASX Listing Rule 10.1

-

AEG acts solely as fund manager and co-investor, with development executed by experienced external development groups

When big ASX news breaks, our subscribers know first

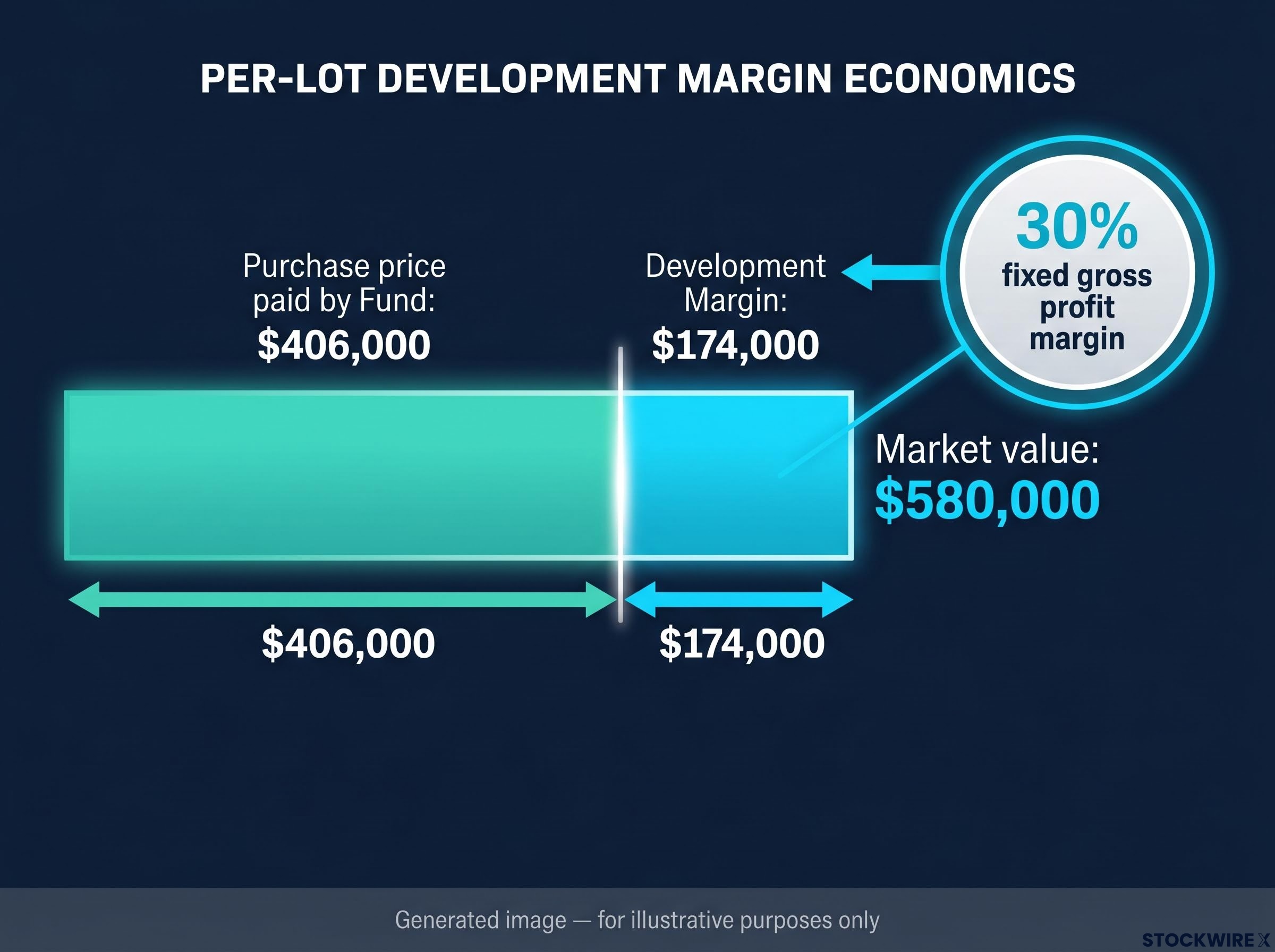

How the Development Margin works for AEG Funds

The acquisition price for each residential stage is determined by an independent valuer using a methodology that incorporates a Development Margin of 30% of gross profit per lot for AEG Funds. This valuation is undertaken at the time each stage is acquired over the term.

Critically, the 30% gross profit margin is fixed throughout the life of the developments. Rather than retaining value at the project level, this structure embeds margin directly into Fund pricing, which the Company positions as supporting the attractiveness of its Funds to investors.

The table below sets out an illustrative example for a hypothetical fund of 100 lots.

| Metric | Per Lot | Total (100 lots) |

|---|---|---|

| Market value (independent valuation) | $580,000 | — |

| Purchase price paid by Fund | $406,000 | — |

| Development Margin / value to Fund | $174,000 | $17,400,000 |

Market value per lot is based on comparable sales in Bungendore over the last five years, including Stage 2 of the adjacent Elm Grove Estate. This is an illustrative example only.

What a property funds management model means for AEG investors

A property funds management business sees AEG establish Funds that finance the acquisition and development of property stages. AEG earns management fees and can also co-invest its own capital to capture direct returns. The announcement states AEG “may co-invest in its Funds up to 100%, participating in both investment returns and investment management fees.”

This dual revenue framing is a defining feature of the model. AEG acts “solely as fund manager and co-investor,” while all development execution sits entirely outside the AEG group, undertaken by experienced external development groups.

AEG’s funds management model is structured to generate three revenue streams across each project: investment management fees, development management fees, and sales and marketing fees, all without the company carrying direct construction or development balance-sheet risk.

In structural terms, AEG positions itself as an arranger and facilitator and not as the developer.

Chairman Alex Brinkmeyer

“Historically, value created through residential development projects would generally be retained at the project level. Under this structure, value is intended to be shared with the AEG Funds… I believe the long-term value created through a successful property funds management business has the potential to exceed the value that would otherwise be realised through a traditional development model.”

Brinkmeyer noted that as AEG’s largest shareholder, his interests are directly aligned with those of all shareholders.

Why Chinnerys sits in a strategic growth corridor

The Company believes Chinnerys represents one of the largest remaining residential development opportunities within the Canberra-Bungendore growth corridor. The site sits immediately north of the established Elm Grove and Elmslea communities, approximately 30 minutes from Canberra.

A current rezoning application covers approximately 300+ acres, expected to yield over 1,200 mixed residential lots. The remaining master-planned land may yield up to an additional 2,000 lots, subject to future zoning and the size of the property.

Beyond housing, the project is intended to deliver seniors living, build-to-rent, retail and commercial development.

Defence and population demand drivers

The Company believes demand for new residential housing in the region is supported by several factors:

-

Proximity to Headquarters Joint Operations Command (HQJOC), Australia’s primary military operational headquarters, located approximately 15 kilometres from the project and described as the closest residential land to HQJOC.

-

One of Australia’s largest concentrations of defence and national security employment, including Russell Offices, HMAS Harman, the Australian Defence Force Academy and Royal Military College Duntroon.

-

Continued population growth and lifestyle migration from Canberra to surrounding regional centres.

-

Limited availability of new residential land supply in the region.

-

The Australian Government’s long-term commitment to increased defence expenditure.

These demand drivers underpin the Company’s thesis for the long-term pipeline value embedded in the landholding.

The next major ASX story will hit our subscribers first

Deal structure, security and next steps

The Funding Deed is between Aland Equity Land Pty Limited, a subsidiary of AEG (AE Landco), and Share Star Holdings Pty Limited, an entity associated with Mr. Brinkmeyer (Landowner). It carries substantially similar terms to the Cowra Property Funding Deed announced to ASX on 19 May 2026.

The Chinnerys Funding Deed upgrades what was previously a Heads of Agreement, slotting the project into a broader AEG property pipeline that already includes the Yarrabilly development in Cowra and the BITF business park project, collectively spanning more than 4,200 mixed residential lots and 100,000sqm of industrial NLA under 10 + 10 year exclusivity terms.

Key terms and secured protections include:

-

Initial 10-year term plus an option for AE Landco to extend for a further 10 years

-

Exclusive appointment of AE Landco to collaborate with the Landowner on facilitating financing and development of stages

-

The Landowner cannot engage third parties for competing development proposals during the term

-

A first right of refusal over any sale of the land

-

Security via mortgage, caveat and irrevocable power of attorney

-

An additional 1% of Gross Realisation payable to the Landowner or its nominee on acquisition of each stage

AE Landco acts only as an arranger and facilitator and not as the developer of the land, retaining discretion over the nature, timing and design of development stages.

Conditions and timeline

The Deed is conditional on required ASX and shareholder approvals. The 60 million share consideration will only be issued once the Deed becomes unconditional, subject to shareholder approval under ASX Listing Rule 10.1 at a general meeting to be held at a later date.

Managing Director David Nolan

“The Chinnerys Funding Deed is the most significant step in building out AEG’s property funds management business, giving AEG long-term funding rights over 3,200 residential lots within one of Australia’s most attractive regional growth corridors.”

Ready to Explore AEG’s 3,200-Lot Chinnerys Development in the Canberra Growth Corridor?

Aland Equity Group’s Property Funding Deed over the Chinnerys master-planned community secures long-term funding rights across approximately 3,200 mixed residential lots in one of Australia’s most strategically positioned regional growth corridors. With a fixed 30% gross profit Development Margin embedded into Fund pricing and a 10 + 10 year exclusive term, the structure is designed to generate multiple revenue streams without direct development balance-sheet risk.

To learn more about AEG’s property funds management model and its expanding pipeline, visit the Aland Equity Group investor centre for the latest announcements and project details.