Tabcorp Holdings has successfully extended its $980m syndicated term loan facility on improved pricing terms, reducing refinancing pressure and extending its average debt maturity to 4.4 years. The announcement, made on 16 June 2026, signals lender confidence in the company’s credit profile and provides greater balance sheet flexibility as management progresses strategic priorities.

Tabcorp secures extended debt facility with improved pricing

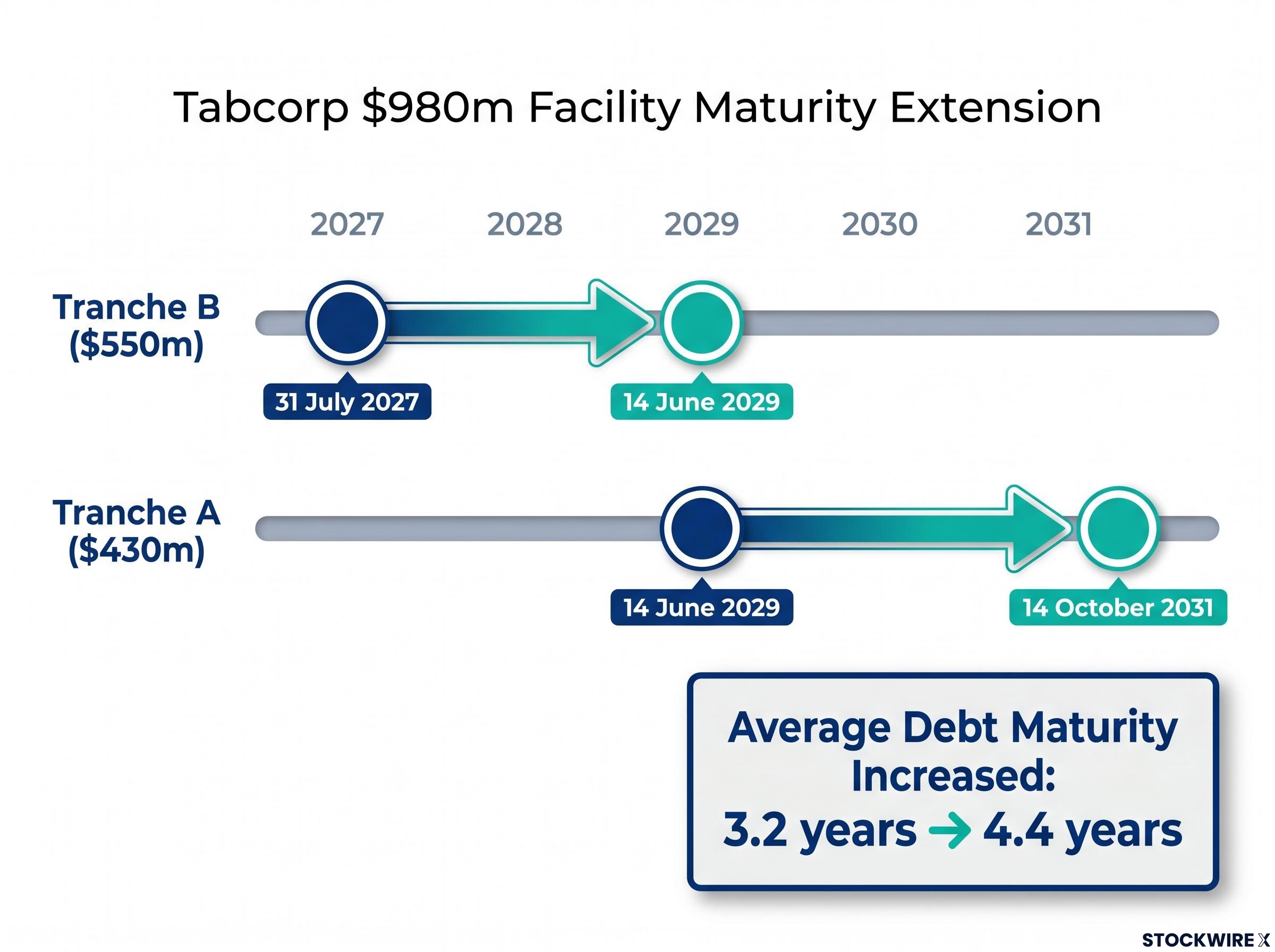

The extension restructures the facility across two tranches with staggered maturities. Tranche B ($550m) has been extended from 31 July 2027 to 14 June 2029, while Tranche A ($430m) has been extended from 14 June 2029 to 14 October 2031.

The improved pricing terms reflect lender confidence in Tabcorp’s credit profile. Syndicated term loans are typically priced at a margin above a benchmark rate (such as the bank bill swap rate).

The dual extension pushes the company’s nearest major debt maturity beyond 2029, removing near-term refinancing risk and providing operational certainty through the next strategic planning cycle.

When big ASX news breaks, our subscribers know first

Average debt maturity extends to 4.4 years

The syndicated term loan extension, combined with Tabcorp’s existing US Private Placement (USPP) and Australian Medium Term Note (AMTN) debt, has increased the company’s average debt maturity from 3.2 years to 4.4 years, an increase of 1.2 years.

This improvement spreads refinancing obligations across a longer timeline, reducing the risk of concentrated maturities in any single period. Longer maturity profiles also provide management with greater flexibility to optimise capital structure decisions as market conditions evolve.

| Metric | Before Extension | After Extension |

|---|---|---|

| Tranche A Maturity | 14 June 2029 | 14 October 2031 |

| Tranche B Maturity | 31 July 2027 | 14 June 2029 |

| Average Debt Maturity | 3.2 years | 4.4 years |

The extended maturity profile reduces near-term refinancing pressure and provides greater certainty for strategic planning, allowing management to allocate capital without the constraint of imminent debt obligations.

What is a syndicated term loan facility?

A syndicated term loan facility is a large loan provided to a single borrower by a group of lenders, typically banks, who pool funds to share credit risk. This structure allows companies to access larger amounts of capital than any single lender would be willing to provide.

Facilities are often structured in tranches, each with different maturity dates. This approach reduces refinancing risk by spreading debt obligations across multiple years, avoiding a concentrated repayment burden in any single period.

Improved pricing terms typically refer to a reduction in the interest margin charged above a benchmark rate (such as the bank bill swap rate). A lower margin directly reduces interest expense, improving earnings and free cash flow.

Management commentary on balance sheet strength

Chief Financial Officer Mark Howell framed the extension as reinforcing Tabcorp’s financial position and strategic flexibility.

Mark Howell, Chief Financial Officer, Tabcorp

“This extension, along with our USPP and AMTN, reinforces the strength of our balance sheet and provides further flexibility as we progress our strategic priorities.”

The commentary links debt management directly to strategic execution, suggesting the extended facility provides capital allocation optionality without balance sheet constraints. The successful refinancing on improved terms also reflects lender confidence in the company’s credit profile.

Investment implications for Tabcorp shareholders

The syndicated term loan extension delivers several material benefits for investors:

- Extended debt maturities remove near-term refinancing risk, with the nearest major obligation now pushed to 2029.

- Improved pricing terms are expected to reduce interest expenses, enhancing free cash flow and earnings.

- Combined debt profile (term loan, USPP, AMTN) now averages 4.4 years maturity, providing greater certainty for strategic planning.

- Balance sheet flexibility supports ongoing strategic initiatives without the constraint of imminent debt obligations.

The extension provides Tabcorp with a stable funding base as it progresses its strategic priorities. While debt management is a defensive measure, it is material in removing financing uncertainty and potentially improving profitability through lower interest costs. The successful refinancing on better terms also signals continued lender confidence in the company’s credit profile.

Don’t Miss the Next Consumer Breakout

Join 20,000+ investors receiving FREE breaking ASX news delivered within minutes of release, complete with in-depth analysis. Get real-time alerts on consumer sector moves before the market reacts. Click the “Free Alerts” button at Big News Blast to start receiving expert coverage the moment announcements drop.