Atomos Ltd Cuts FY26 Revenue Outlook to ~$40m as Margins Improve

Atomos flags ~$40m FY26 revenue amid softer consumer demand and new product launches

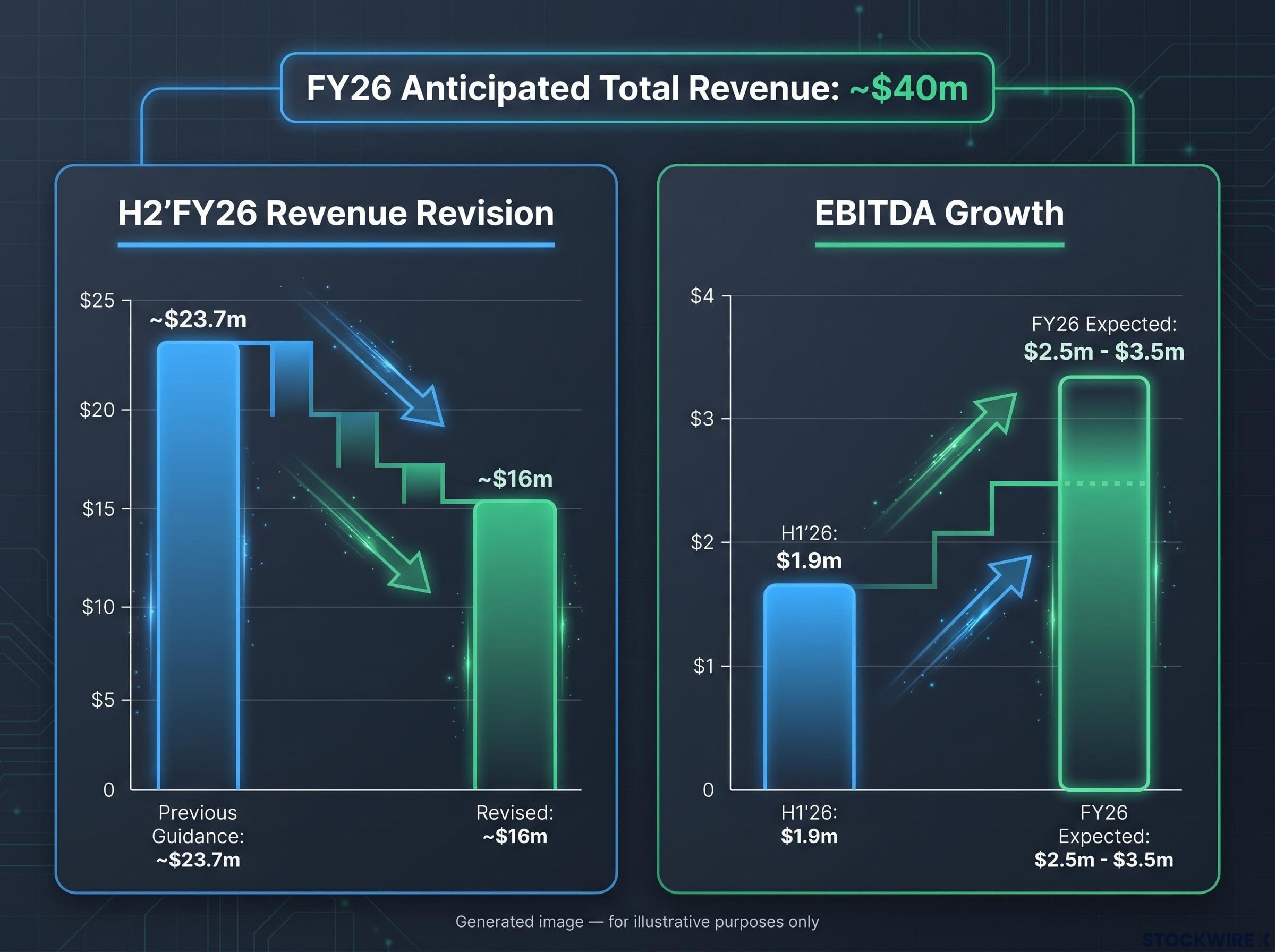

Atomos Limited (ASX:AMS) has issued an FY26 trading update revising its full-year guidance, with total sales now anticipated at ~$40m, subject to year-end audit adjustments. The update, released on 6 July 2026, reflects softer end-consumer demand across the second half.

H2’FY26 revenue is expected to land at ~$16m, well below previous guidance of ~$23.7m, with the majority of that half arriving in Q4. The picture is mixed, however. FY26 EBITDA is anticipated at $2.5m – $3.5m, up from H1’26 EBITDA of $1.9m, supported by improved contribution margins.

The result frames a period of contrasting outcomes for the company, pairing a clear revenue shortfall against a strengthened operational base and favourable tariff changes.

When big ASX news breaks, our subscribers know first

What drove the revenue shortfall

Managing Director and CEO Peter Barber attributed the miss against guidance to a combination of timing and demand factors. Several were logistical, while others reflected the broader macroeconomic backdrop weighing on discretionary spending.

The specific drivers included:

-

Approximately $2m of product shipped prior to 30 June had not been received by customers at year-end and is not expected to be recognised in FY26.

-

The late shipment of the Sumo PRO 19, which shipped only in the final days of May, meant no re-orders landed within the financial year.

-

Sell-through of the new Ninja range and the June promotional campaign came in below expectations.

-

The ongoing conflict in the Middle East, coupled with rising US inflation and interest rate fears, subdued end-consumer demand and prompted destocking by key distributors and resellers.

Management also noted that Q3 is historically a softer period for global sales. The company had been optimistic of a stronger Q4 uplift driven by its refreshed portfolio, though the demand environment ultimately limited that recovery.

Margin strength cushions the earnings picture

Despite the lower revenue, earnings held up on the back of improved contribution margins in the second half, which management attributed to favourable tariff changes. This margin improvement is the key reason FY26 EBITDA is still expected to grow relative to the first half.

Importantly for investors, these improved contribution margins are expected to be maintained in future periods, providing a forward signal on profitability even as top-line demand remains under pressure. Second-half earnings remain subject to audit and the accounting treatment of the Flanders Scientific acquisition.

| Metric | Previous Guidance | Revised Expectation | Comparison Note |

|---|---|---|---|

| H2’FY26 Revenue | ~$23.7m | ~$16m | Majority expected in Q4 |

| FY26 Revenue | — | ~$40m | Subject to year-end audit |

| FY26 EBITDA | — | $2.5m – $3.5m | Up on improved margins |

| H1’26 EBITDA (reference) | — | $1.9m | Prior-half comparison |

Product refresh and Flanders acquisition strengthen the platform

Alongside the guidance revision, management flagged several operational milestones it expects to support medium and longer-term growth. In late Q3 and Q4, the company launched three new products from its core range:

-

Shogun AV-19

-

Ninja RAW

-

Sumo PRO 19

These were accompanied by a broader set of complementary ecosystem products. The Sumo PRO 19, although announced in April, shipped only in the final days of May, slightly later than originally anticipated.

The Sumo PRO 19 launch at NAB 2026 was accompanied by six other new products and multiple Best of Show awards, with the flagship 19-inch 4K HDR monitor recorder switcher priced at $4,399 and originally scheduled to ship in early June.

The company also completed the acquisition of Flanders Scientific in April, described as a leader in professional reference monitoring. Management noted the acquisition enables Atomos to service an increasingly larger portion of the end-to-end content creation process, expanding both product depth and addressable market.

The Flanders Scientific acquisition completed in late April for approximately $2.35 million cash plus 5.6 million AMS shares, with the deal funded through a $10 million Commonwealth Bank facility and structured to contribute $1 million in annual post-synergy EBITDA from the outset.

CEO Commentary

“The second half of FY26 has been one of mixed outcomes for the business. Operationally, we have delivered several major milestones which we expect will contribute materially to our medium and longer-term growth,” said Peter Barber, Managing Director and CEO.

What Atomos does

Atomos designs hardware devices for monitoring and recording, easy-to-use software tools, and cloud services aimed at filmmakers and video content creators. Its products support tasks such as recording cinema-quality footage, monitoring scenes with colour accuracy, and streaming live events.

The Flanders acquisition centres on reference monitoring. This capability positions the company deeper within the professional content-creation supply chain.

Atomos is based in Melbourne, Australia, with a distributed worldwide team and offices across the USA, UK, Germany, China, and Japan.

The next major ASX story will hit our subscribers first

What investors should watch next

The update leaves several factors open, and each will shape how the FY26 result is ultimately reported. Key watchpoints drawn from the announcement include:

-

Year-end audit adjustments and final accounting for the Flanders acquisition, both still to be confirmed.

-

The sustainability of improved contribution margins into future periods, which management expects to hold.

-

Whether re-orders for the Sumo PRO 19 and stronger sell-through across the refreshed range materialise as demand conditions evolve.

The company has not disclosed FY27 guidance or specific timelines, so investors will be assessing near-term demand pressure against a broadened, higher-margin product platform. The trading update presents a business navigating a clear revenue shortfall while pointing to structural improvements in margins and product range.

Don’t Miss the Next Consumer Tech Move on the ASX

Big News Blast delivers FREE breaking ASX consumer sector news to your inbox within minutes of release, complete with in-depth analysis already done for you. Join 20,000+ subscribers staying ahead of the market and click the “Free Alerts” button at StockWire X to start receiving alerts the moment news breaks.