Adairs Ltd Flags Record FY26 Sales as Non Cash Impairment Drives Loss

Adairs flags higher Group sales but a non-cash impairment sends FY26 to a statutory loss

Adairs Limited (ASX: ADH) issued an FY26 trading update on 8 July 2026, flagging Group sales growth alongside a non-cash impairment of its Focus on Furniture business unit that is expected to push the Group to a statutory net loss. Full-year results are scheduled for release on 24 August 2026.

The update points to two contrasting stories. Group sales are guided to rise to $640.0m–$641.5m, up +3.7% at the midpoint on FY25, while an expected impairment charge of $62m–$68m ($56m–$60m after tax) drives an anticipated statutory net loss after tax of approximately $43m (indicatively $39m–$46m).

Group underlying EBIT is guided at $53.5m–$55.5m, down -1.3% at the midpoint. The picture beneath the headline loss is one of two brands growing strongly and one legacy brand under remediation, with the loss driven by accounting adjustments rather than cash outflows.

When big ASX news breaks, our subscribers know first

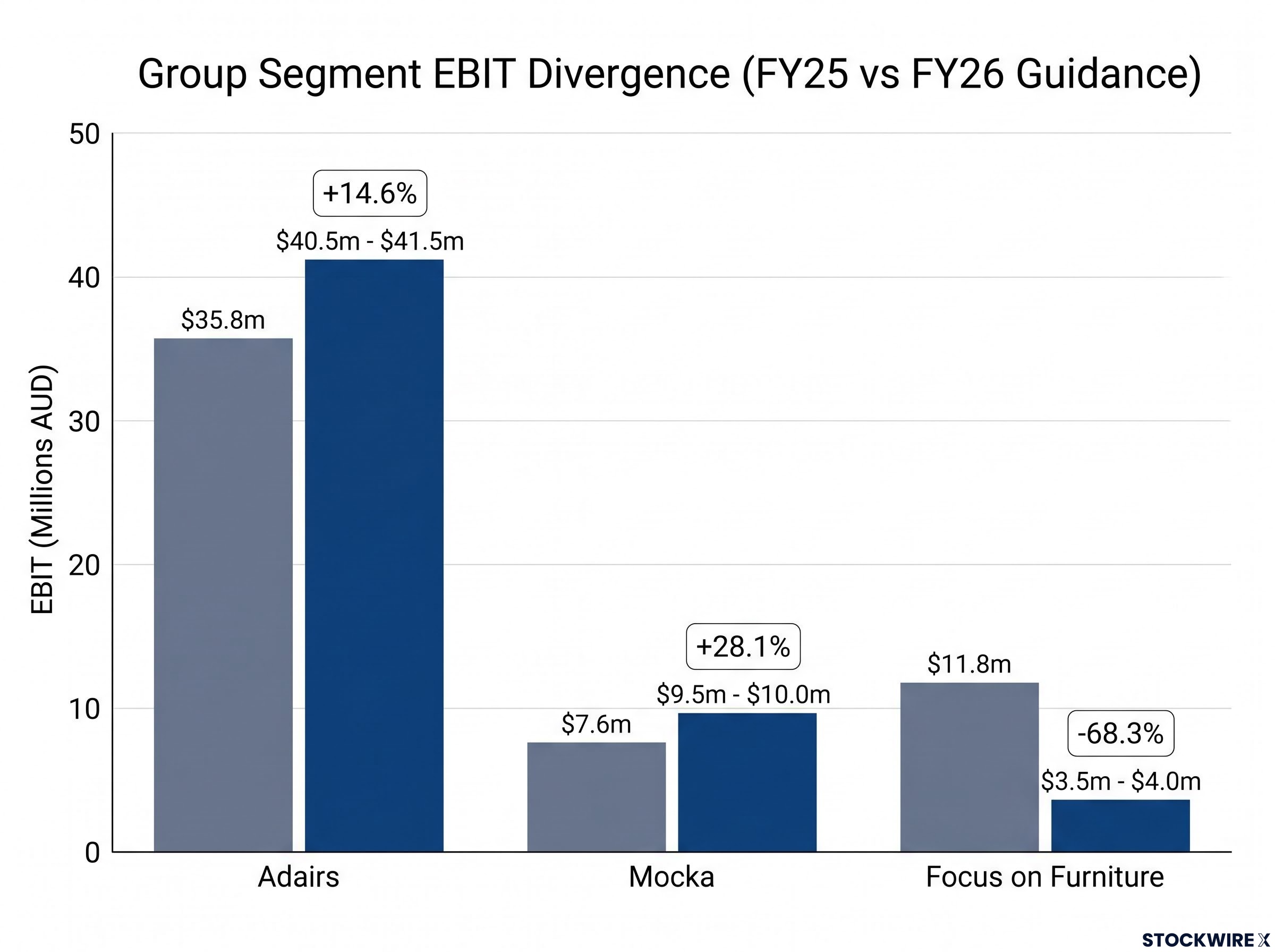

Segment performance — Adairs and Mocka growth offset Focus decline

The divergence across the Group’s three business units defines the FY26 result. The Adairs and Mocka brands delivered pleasing sales and earnings growth, while Focus on Furniture continued to decline through the second half.

The Adairs brand reported like-for-like sales growth of +3.8%, supported by product range enhancements, an improved in-store experience and continued online channel growth. Gross margin improved during H2 and is expected to be sustained into FY27. The new store concept launched at Bondi Junction delivered encouraging results, and the store renewal programme is expanding into a broader refurbishment programme across small, medium and large formats. A small number of underperforming stores were exited as planned, and the brand’s exit from the New Zealand market, a small, loss-making region, is now complete.

Mocka delivered another year of strong growth, driven by Australia where sales grew approximately 40%. The first standalone retail store opened in mid-June 2026 in Maroochydore. A second store is planned at Tower Junction, Christchurch in Q1 FY27, followed by a third at Mornington, Victoria in Q2 FY27. These three stores form the trial of physical retail for Mocka.

Focus on Furniture experienced continued decline in both sales and underlying EBIT, reflecting intense competitor promotional activity, conversion pressure, product underperformance and execution challenges. A new management team has been appointed progressively through the year and is rebuilding the business across product, marketing, retail execution and operating processes.

| Business Unit | FY26 Sales Guidance | FY26 EBIT Guidance | FY25 EBIT Actual | EBIT Change |

|---|---|---|---|---|

| Adairs | $458.5m–$459.0m | $40.5m–$41.5m | $35.8m | +14.6% |

| Mocka | $70.5m–$71.0m | $9.5m–$10.0m | $7.6m | +28.1% |

| Focus on Furniture | $111.0m–$111.5m | $3.5m–$4.0m | $11.8m | -68.3% |

| Group | $640.0m–$641.5m | $53.5m–$55.5m | $55.2m | -1.3% |

Understanding a non-cash impairment — what it means for investors

A goodwill and brand intangible impairment is an accounting write-down of the carrying value of an acquired business. Critically, an impairment is not a cash outflow. No money leaves the business. It is a paper adjustment that reduces the recorded value of an asset already on the balance sheet.

This is why the charge hits the statutory result but is excluded from underlying earnings, which aim to reflect the ongoing operating performance of the business.

The expected impairment reflects all of the goodwill ($40.9m) plus a substantial portion of the brand intangible. Following the write-down, the residual carrying value of the Focus business unit is expected to be approximately $25m–$31m (excluding lease right-of-use assets and corresponding lease liabilities). These figures are indicative and remain subject to completion of impairment testing, final Board approval and external audit concurrence.

For investors, the distinction matters. A non-cash charge does not drain cash, affect covenants, the franking account or dividend capacity, essential context for interpreting the headline loss.

The other significant items behind the statutory result

Beyond the Focus on Furniture impairment, several additional significant items will be excluded from underlying earnings in FY26:

-

Focus on Furniture impairment: $62m–$68m ($56m–$60m after tax)

-

Software-as-a-Service (SaaS) project costs (including the Adairs ERP update): $18.0m–$19.0m, including non-cash write-offs of legacy infrastructure ($2.8m); the new ERP system is scheduled to go live in late Q1 FY27

-

Adairs New Zealand market exit costs: $3.5m–$4.0m (lease surrenders and modifications, make-good requirements, employee obligations, and store asset and inventory impairments)

-

Impact of AASB 16 Leases

The operating result for Adairs New Zealand, including clearance activity during the wind-down, remains included in underlying earnings. New Zealand accounted for 3.0% of Adairs revenue in FY26, and the exit is expected to improve Group underlying EBIT and EBIT margin from FY27.

Capital position remains solid despite the loss

The Group’s balance sheet remains in a solid position despite the anticipated statutory loss. Net debt stood at approximately $49m at the end of June 2026, down from $67.6m at June 2025, and comfortably within facility limits of $135m.

Because the impairment charge is non-cash, it raises no concern in the Group’s covenant calculations. It does not affect the franking account and is not expected to affect the Company’s capacity to pay a dividend in respect of FY26. Any final dividend will be determined by the Board in conjunction with the FY26 results.

Key reassurance from the announcement

“The impairment is a non-cash accounting charge; it does not affect the Group’s franking account and is not expected to affect the Company’s capacity to pay a dividend in respect of FY26.”

Attributed to the Company’s announcement.

The next major ASX story will hit our subscribers first

What comes next for Adairs

The forward path centres on a series of milestones expected to shape the FY27 setup:

-

FY26 full-year results and conference call: 24 August 2026

-

Adairs ERP go-live: late Q1 FY27

-

Mocka Christchurch store: Q1 FY27; Mornington store: Q2 FY27

-

Focus on Furniture: operational improvement programme intended to re-platform the business for growth and materially improve earnings over the medium and long term

-

New Zealand exit benefits expected to flow from FY27

The combination of sustained margin gains at Adairs, continued Mocka momentum, the Focus on Furniture remediation programme and New Zealand exit tailwinds positions the Group for improving EBIT margins and performance as FY27 progresses. While the statutory loss will dominate the headline result, the underlying business continues to generate cash and grow across two of its three brands.

Don’t Miss the Next Consumer Discretionary Move

Big News Blast delivers FREE breaking ASX news straight to your inbox within minutes of release, complete with in-depth analysis already done for you. Join 20,000+ subscribers staying ahead of the market across retail, consumer and beyond. Click the “Free Alerts” button at StockWire X to start receiving alerts the moment news breaks.