Oceania Healthcare Launches $100M Bond Offer to Cut Debt and Extend Funding Runway

Oceania Healthcare launches $100 million bond offer to strengthen balance sheet

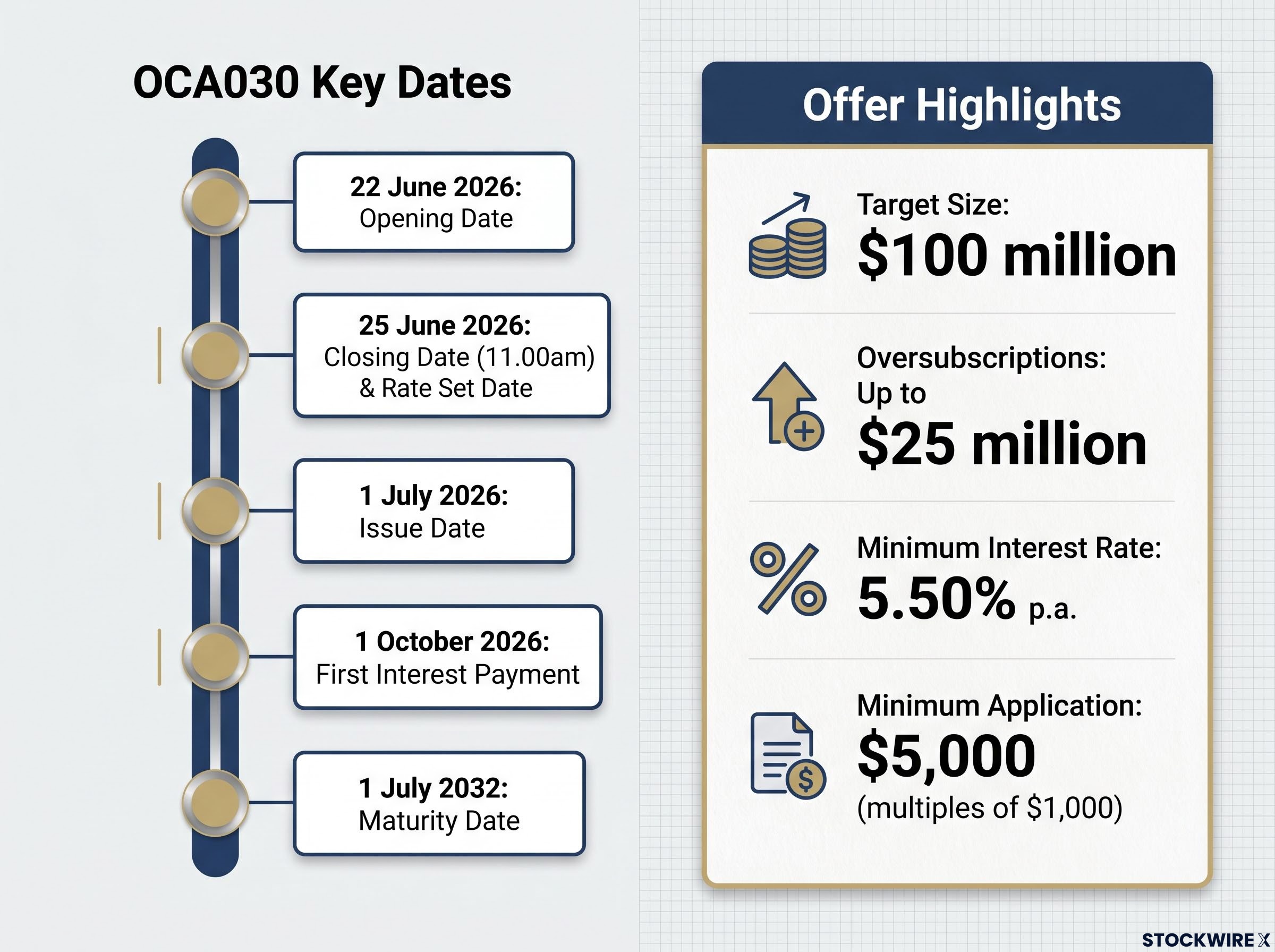

Oceania Healthcare has launched a retail bond offer targeting up to $100 million, with the ability to accept oversubscriptions of up to $25 million at the company’s discretion. The fixed-rate, secured, unsubordinated bonds mature on 1 July 2032 and carry a minimum interest rate of 5.50% per annum, with an indicative issue margin of 1.85% to 1.95% above the swap rate.

Net proceeds from the offer are to be applied to repay a portion of existing bank debt and for general corporate purposes. The bond issue extends Oceania’s funding diversification and tenor by approximately 0.3 years, with NZX ticker code OCA030 reserved for the bonds on the NZX Debt Market.

Payments on the bonds are guaranteed by Oceania Village Company Limited, Oceania Care Company Limited and Oceania Group (NZ) Limited under a guarantee contained in the Global Security Deed. Bondholders rank equally with bank lenders for security under the Security Trust Deed.

When big ASX news breaks, our subscribers know first

What is a retail bond offer?

Retail bonds allow individual investors to lend money to a company in exchange for regular interest payments and the return of principal at maturity. In Oceania’s case, the bonds are “secured,” meaning bondholders have claims over company assets if the issuer defaults. The bonds are also “unsubordinated,” meaning bondholders rank equally with bank lenders for security purposes.

Oceania’s revenue model includes a Deferred Management Fee (DMF) structure. When a resident purchases an Occupation Right Agreement (ORA) for a care suite, apartment, or villa, Oceania charges a 30% DMF recognised over the average expected occupancy period (3 years for care suites, 5 years for apartments, 7 years for villas). Oceania also receives any capital gain on the resale of the unit under its standard resale gain policy.

This revenue structure provides a predictable income stream that supports bond interest payments and operational cash flow generation.

Record FY26 performance underpins the offer

Oceania reported record operational and financial performance for the financial year ended 31 March 2026, strengthening its balance sheet ahead of the bond offer. Sales volumes reached a record 603 units, up 16% from 520 units in FY25, while Proforma Underlying EBITDA increased 20.2% to $97.7 million.

Net debt reduced by $121 million to $506.7 million, representing a 19.3% decrease from $628 million in FY25. Gearing fell 6.2 percentage points to 30.1%, at the low end of the board’s target range of 30-35%. Total assets reached $3.1 billion, with $2.9 billion in property assets.

| Metric | FY25 | FY26 | Change |

|---|---|---|---|

| Sales Volume (units) | 520 | 603 | +16.0% |

| Proforma Underlying EBITDA | $81.3m | $97.7m | +20.2% |

| Net Debt | $628.0m | $506.7m | -19.3% |

| Gearing | 36.3% | 30.1% | -6.2pp |

This operational momentum demonstrates Oceania’s ability to generate recurring earnings and strengthen its balance sheet, providing capacity to service bond obligations while maintaining development optionality.

Oceania’s FY26 results in full show cost-out savings of $13.2 million delivered during the year, with annualised savings expected to reach $20.4 million in FY27 as part of a broader $30 million cash and cost savings program.

Security structure and covenant protections

How bondholders are protected

Bondholders receive security through guarantees from three key operating subsidiaries: Oceania Village Company Limited (total assets $2,995 million), Oceania Care Company Limited (total assets $52 million), and Oceania Group (NZ) Limited (total assets $13 million). Combined, these entities hold total assets of $3.1 billion, comprising $2.9 billion in property assets.

After priority claims including liabilities preferred by law ($34 million, comprising employee entitlements and amounts owed to Inland Revenue) and statutory supervisor liabilities ($1,258 million), approximately $1.8 billion in assets remain available as security for bondholders and bank lenders. Bondholders rank equally with bank lenders under the Security Trust Deed, with first ranking mortgages over undeveloped land and aged care centre land, and second ranking mortgages over land used for registered retirement villages.

Loan-to-value covenant

The bond terms include a loan-to-value ratio (LVR) covenant requiring total secured debt to not exceed 50% of property valuations. As at 31 March 2026, Oceania’s current LVR stood at 31.8%, providing 18.2 percentage points of headroom against the covenant limit. The interest cover ratio reached 3.7x against a covenant requirement of 2.0x, demonstrating substantial buffer against property market volatility.

If an LVR breach occurs, Oceania has 6 months from the date of the semi-annual compliance report setting out that breach to remedy it. If not remedied within that 6 months, Oceania must give notice to the Bond Supervisor within 20 Business Days of that date of its plan to remedy the breach. If the breach is not then remedied within 6 months of the date of that notice, an Event of Default occurs.

Liquidity and funding position

Oceania held over $200 million in cash and undrawn committed facilities as at 31 March 2026, comprising $16.6 million in cash and $201.7 million in undrawn facility headroom. The company’s total bank facilities stand at $500 million, with $185 million in general/corporate facilities and $315 million in development facilities (Facility B).

Oceania intends to cancel an equivalent amount of bank facility limit post-offer to maintain existing headroom. The board is considering refinancing options for the $125 million OCA010 retail bonds maturing in October 2027.

Existing retail bonds on issue:

- OCA010: $125 million maturing 19 October 2027

- OCA020: $100 million maturing 13 September 2028

The capital structure provides operational flexibility and debt management optionality, with average facility tenor of 3.3 years at 31 March 2026 (increasing by approximately 0.3 years following the OCA030 bond issue).

Development pipeline and growth outlook

Oceania expects to complete 81 units across 3 sites in FY27, comprising 28 villas at Franklin Stage 2, 30 units at Elmwood (conversion of villas and apartments), and 23 villas at Bream Bay. Approximately 80 units are planned for FY28 delivery, with a target build rate of 150 units per annum by FY31.

The company holds a development pipeline of approximately 1,270 units across geographically diverse locations, allowing a staged approach to capital deployment. Development debt stood at $248 million as at 31 March 2026, supported by $382 million in development assets (comprising $227 million in unsold new stock, $49 million in work-in-progress, and $106 million in undeveloped land).

This staged development approach allows Oceania to maintain capital discipline while preserving growth optionality, with the flexibility to accelerate or moderate construction activity in response to market conditions.

Key dates for investors

The offer operates on a tight timeline requiring prompt investor action:

- Opening Date: Monday, 22 June 2026

- Closing Date: Thursday, 25 June 2026 (11.00am)

- Rate Set Date: Thursday, 25 June 2026

- Issue Date: Wednesday, 1 July 2026

- First Interest Payment: Thursday, 1 October 2026

- Maturity Date: Thursday, 1 July 2032

The minimum application is $5,000, with additional investments in multiples of $1,000. Interest payments occur quarterly on 1 January, 1 April, 1 July and 1 October each year until maturity.

The next major ASX story will hit our subscribers first

Strategic priorities and dividend outlook

Dividend payments remain paused pending positive operating free cash flow. Oceania intends to resume dividends at 40%-60% of free cash flow from operations once this milestone is achieved. Free cash flow from operations improved 64% in FY26 and remains on track to be cash positive in FY27.

The company has annualised $20.4 million in right-sizing benefits from year end, with an additional $10 million in targeted cash savings for FY27. These operational efficiency initiatives support the pathway to dividend resumption while strengthening the balance sheet to service bond obligations.

Strategic Focus

The board’s target gearing range is 30-35%, while management is building toward sustainable dividend payments, with a clear focus on operational cash flow generation and debt reduction.

The bond offer provides Oceania with extended funding tenure and diversified capital sources, supporting both operational cash flow improvement and future growth initiatives while maintaining financial flexibility through the development cycle.

Don’t Miss the Next Healthcare Financing Move

Join 20,000+ investors receiving FREE breaking ASX news within minutes of release, complete with expert analysis. Get real-time alerts on healthcare bond offers, capital raisings, and sector developments delivered straight to your inbox. Click the “Free Alerts” button at Big News Blast to stay ahead on healthcare market moves.