Jumbo Interactive Ltd Lifts FY26 Earnings Guidance on Dream US Strength

Jumbo lifts FY26 Group earnings guidance on stronger Dream US performance

Jumbo Interactive (ASX:JIN) has upgraded its FY26 earnings guidance ahead of full-year results scheduled for 27 August 2026, revising prior forecasts to reflect stronger trading across the Group.

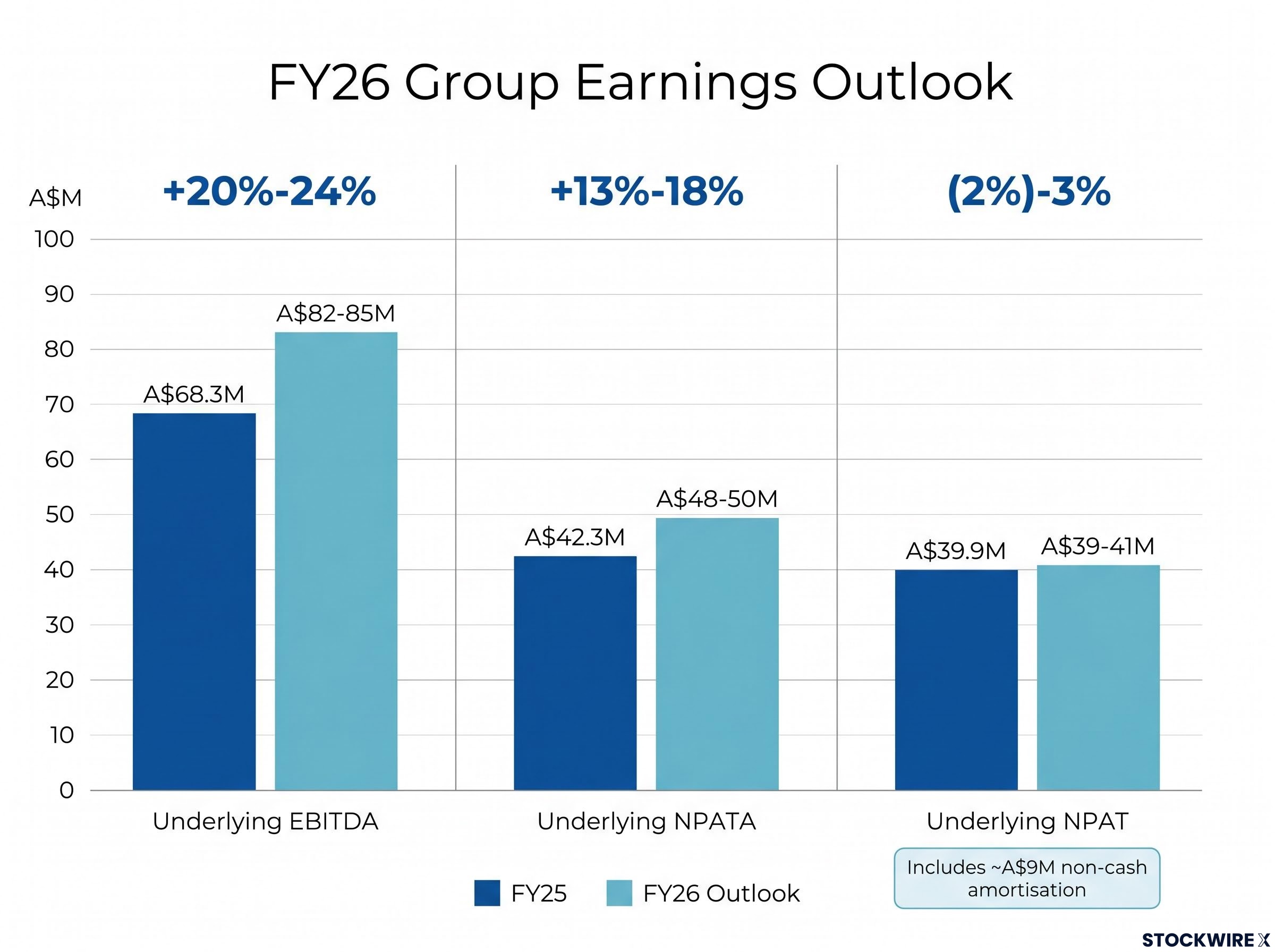

Group underlying EBITDA is now expected to rise 20–24% on FY25 to A$82–85 million, up from A$68.3 million, while underlying NPATA is forecast to climb 13–18% to A$48–50 million, from A$42.3 million.

The standout driver is the recently acquired Dream Giveaway (Dream US) business, whose guidance was materially raised since February. The company will provide its FY27 Outlook alongside the FY26 results release on 27 August 2026.

When big ASX news breaks, our subscribers know first

What changed across each division

The revised guidance updates the Group’s previous FY26 Outlook, provided at the 1H26 results in February 2026. The changes are concentrated in the two Dream businesses acquired in October 2025 and the Managed Service divisions, while the Australian segment’s guidance was left unchanged.

| Segment | Measure | Previous FY26 Outlook | Revised FY26 Outlook | Commentary |

|---|---|---|---|---|

| Australia | EBITDA margin | 46%–50% | 46%–50% | No change |

| Dream UK | EBITDA (8½ months) | £8.0m–£8.3m | £7.0m–£7.3m | Integration investment, market testing, seasonality |

| Dream US | EBITDA (8 months) | US$2.7m–US$3.0m | US$5.2m–US$5.5m | More draws and favourable timing |

| Managed Service – UK | EBITDA growth vs pcp | 10%–15% | ~10% | Higher jackpots, offset by cost discipline |

| Managed Service – Canada | EBITDA growth vs pcp | 20%–25% | 35%–45% | New business wins, product investment, campaign timing |

Dream US drives the upgrade

The Dream US revision is the most significant of the update, with guidance nearly doubling to US$5.2–5.5 million for the 8-month period, up from the prior US$2.7–3.0 million range.

The company attributes the improved performance to changes in both the number and timing of draws since acquisition, with 29 draws in FY26 versus 16 draws in the prior comparable period. Jumbo noted it will continue to invest in the business, including migrating Dream US onto the Jumbo Lottery Platform and a new app scheduled for 1QFY27.

Dream UK: a softer range but strong underlying growth

The Dream UK guidance was trimmed to £7.0–7.3 million for the 8½-month period, but the company states the business remains on a strong growth trajectory. The annualised result represents expected growth of 20–25% on the £8.3 million reported for the 12 months to 30 April 2025.

The revision reflects increased investment as Dream UK transitions from its founders to Jumbo, the impact of new market testing initiatives, and seasonality.

On leadership, Jumbo confirmed the appointment of a new Dream UK business head who joins this month. The founders are expected to transition out of the business by December 2026, in line with the earn-out period.

Why the guidance upgrade matters for investors

The segment revisions flow through to a stronger Group-level result, with the standout being the divergence between the flat NPAT forecast and the double-digit growth expected in EBITDA and NPATA.

| Group Metric (A$M) | FY25 | FY26 Outlook | Growth |

|---|---|---|---|

| Underlying EBITDA | 68.3 | 82–85 | 20%–24% |

| Underlying NPAT | 39.9 | 39–41 | (2%)–3% |

| Underlying NPATA | 42.3 | 48–50 | 13%–18% |

The gap between the flat NPAT outlook (-2% to 3%) and NPATA growth of 13–18% is a key point for investors. Underlying NPAT includes approximately A$9 million of incremental non-cash amortisation of acquired intangibles from the Dream acquisitions, whereas NPATA strips this out.

In practical terms, the acquisitions are contributing genuine earnings growth, and the NPAT drag reflects a non-cash accounting effect rather than deteriorating operations.

Underlying EBITDA also excludes FY26 one-off and non-recurring items of approximately A$8–9 million pre-tax, including:

-

Transaction and integration costs associated with the Dream UK and Dream US acquisitions

-

Acquisition accounting adjustments under AASB 3 – Business Combinations

-

Unrealised foreign exchange impacts on intercompany loans

Understanding underlying earnings and acquisition accounting

Companies often report “underlying” earnings alongside statutory figures to help investors see operating performance without the distortion of one-off or non-cash items. Underlying metrics here exclude one-off and non-recurring costs.

EBITDA measures earnings before interest, tax, depreciation and amortisation, giving a view of core operating profitability. NPAT is net profit after tax, the bottom-line statutory measure. NPATA is NPAT before the amortisation of acquired intangibles.

When a company makes an acquisition, accounting rules require it to recognise and gradually write down the value of acquired assets such as software, customer relationships and trademarks. This amortisation is a non-cash charge that reduces reported NPAT but does not reflect cash leaving the business.

For Jumbo, this distinction matters because it allows investors to assess the operating performance of the Dream businesses separately from the accounting effects tied to acquiring them.

The next major ASX story will hit our subscribers first

What comes next

The company pointed investors to several upcoming catalysts. The figures released remain unaudited management forecasts, subject to Board and external audit review, and may be impacted by final acquisition accounting adjustments for the Dream UK and Dream US acquisitions.

Key dates ahead include:

-

FY26 full-year results on 27 August 2026, presenting audited figures.

-

FY27 Outlook, to be provided at the same results release.

-

Dream US platform and app migration scheduled for 1QFY27.

-

Dream UK founder transition completing by December 2026, in line with the earn-out period.

Company commentary on Dream UK

“The business remains on a strong growth trajectory, with the annualised result representing expected growth of 20-25% on the £8.3m reported for the 12 months to 30 April 2025 (as disclosed at the time of the acquisition on 15 October 2025).”

The upgraded guidance reflects stronger trading across the Group, led by Dream US, though investors should note the figures are current management forecasts and remain subject to review before the audited results are confirmed in August.

Don’t Miss the Next Consumer Sector Winner

Big News Blast delivers FREE breaking ASX announcements to your inbox within minutes of release, complete with in-depth analysis already done for you. Join 20,000+ subscribers who stay ahead of the market the moment news breaks. Click the “Free Alerts” button at StockWire X to get started today.