Bravura Solutions Ltd Lifts FY26 Cash EBITDA Guidance to $77M

Bravura Solutions lifts FY26 cash EBITDA guidance to ~$77m

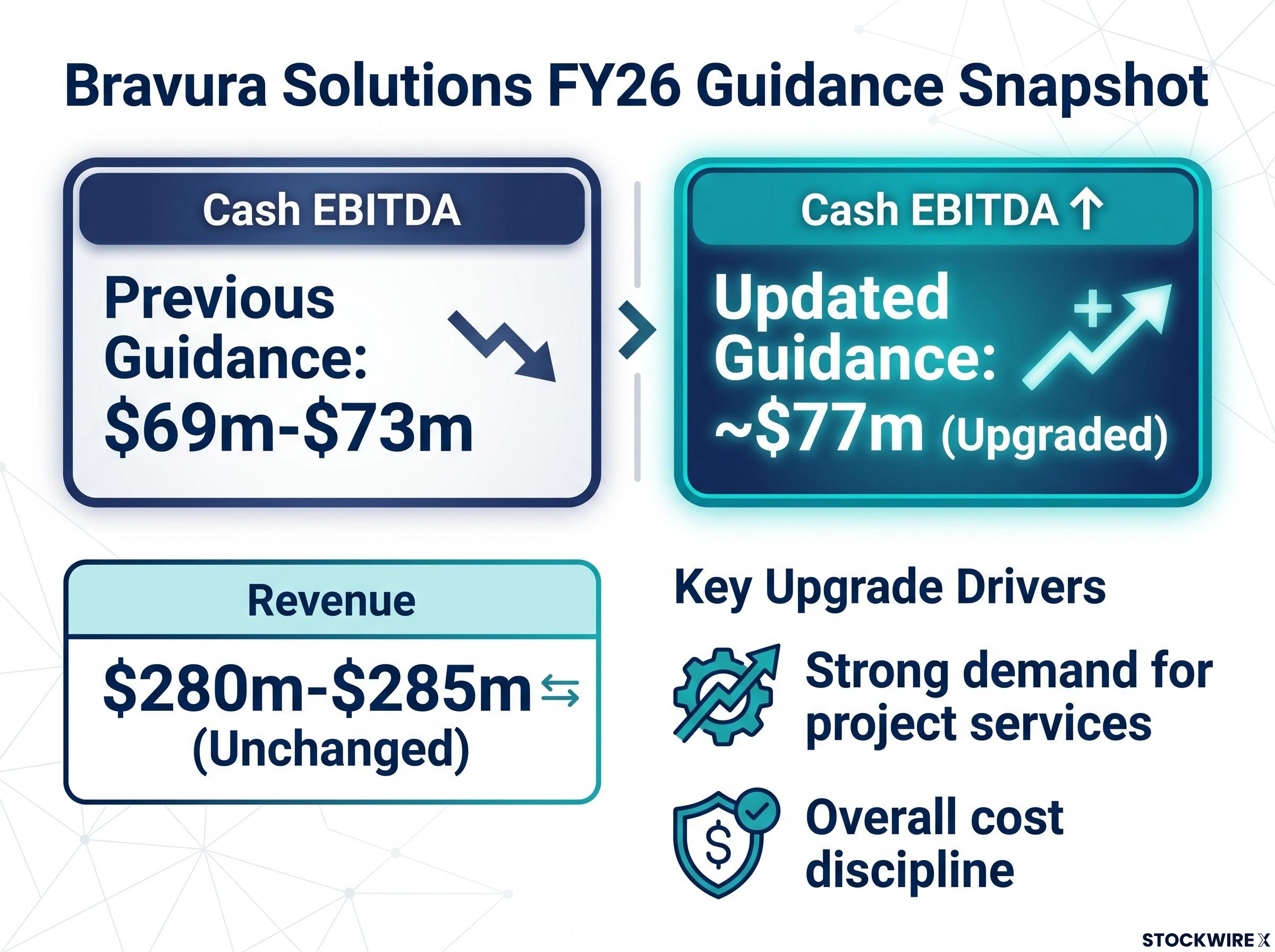

Bravura Solutions has upgraded its FY26 Cash EBITDA guidance ahead of the release of its full-year results, pointing to a stronger-than-expected second half.

Based on unaudited figures, the Company now expects Cash EBITDA of approximately $77m for FY26, up from prior guidance of $69m to $73m. Revenue remains within the previously guided range of $280m to $285m, while PPE Capex guidance is unchanged at approximately $4m.

The Company confirmed that FY26 full-year results are scheduled for release on 12 August 2026. Bravura is a leading provider of software solutions for the wealth management, life insurance and funds administration industries.

When big ASX news breaks, our subscribers know first

What’s driving the upgrade

Bravura cited two key drivers behind the improved outlook:

- Strong demand for project services across its business units.

The February 2026 guidance upgrade had already signalled strengthening operational momentum, lifting Cash EBITDA guidance from a $60m midpoint to a $69m-$73m range on the back of increased project engagement and improving operating leverage.

- Overall cost discipline maintained.

The update also reflects an average GBP/AUD exchange rate of 1.92 for 2H26, compared with the 1.95 previously assumed.

| Metric | Previous Guidance | Updated Guidance | Change |

|---|---|---|---|

| Revenue | $280m–$285m | $280m–$285m | Unchanged |

| Cash EBITDA | $69m–$73m | ~$77m | Upgraded |

| PPE Capex | ~$4m | ~$4m | Unchanged |

| GBP/AUD (2H26) | 1.95 | 1.92 | Revised |

Colin Greenhill, Group CEO and Managing Director

“I am pleased with the strong performance over the last six months. The teams are focussed on greater engagement with our customers which has led to increased project work and stronger renewals. We have continued to manage costs well whilst investing in core technology and exploring new initiatives.”

Understanding Cash EBITDA — and why the beat matters

Cash EBITDA is a measure of a company’s underlying cash-generating capacity. Bravura defines it as revenue minus operating costs (including hosting asset depreciation), less capitalised development costs, PPE capex, lease costs and one-off revenue adjustments.

The next major ASX story will hit our subscribers first

What investors should watch next

Several near-term markers will help confirm the strength of this update:

- FY26 full-year audited results are due on 12 August 2026, with current figures unaudited.

An unaudited guidance upgrade ahead of results, with steady revenue and a lifted cash earnings figure, points to disciplined execution. Confirmation of these figures lands at the August results.

Bravura’s London AIM dual listing, targeting admission on or around 28 July 2026, positions the company to reach UK and European institutional investors at a moment when its financial narrative has materially strengthened.

Don’t Miss the Next ASX Tech Winner

Get FREE breaking ASX tech news delivered to your inbox within minutes of release, complete with in-depth analysis. Join 20,000+ subscribers already ahead of the market and never miss a market-moving announcement. Click the “Free Alerts” button at StockWire X to start receiving alerts the moment ASX tech news breaks.