Collins Foods Ltd Posts Record FY26 Revenue as Profit Rises 13%

Collins Foods caps FY26 with record $1,592.6m revenue and lifted dividend

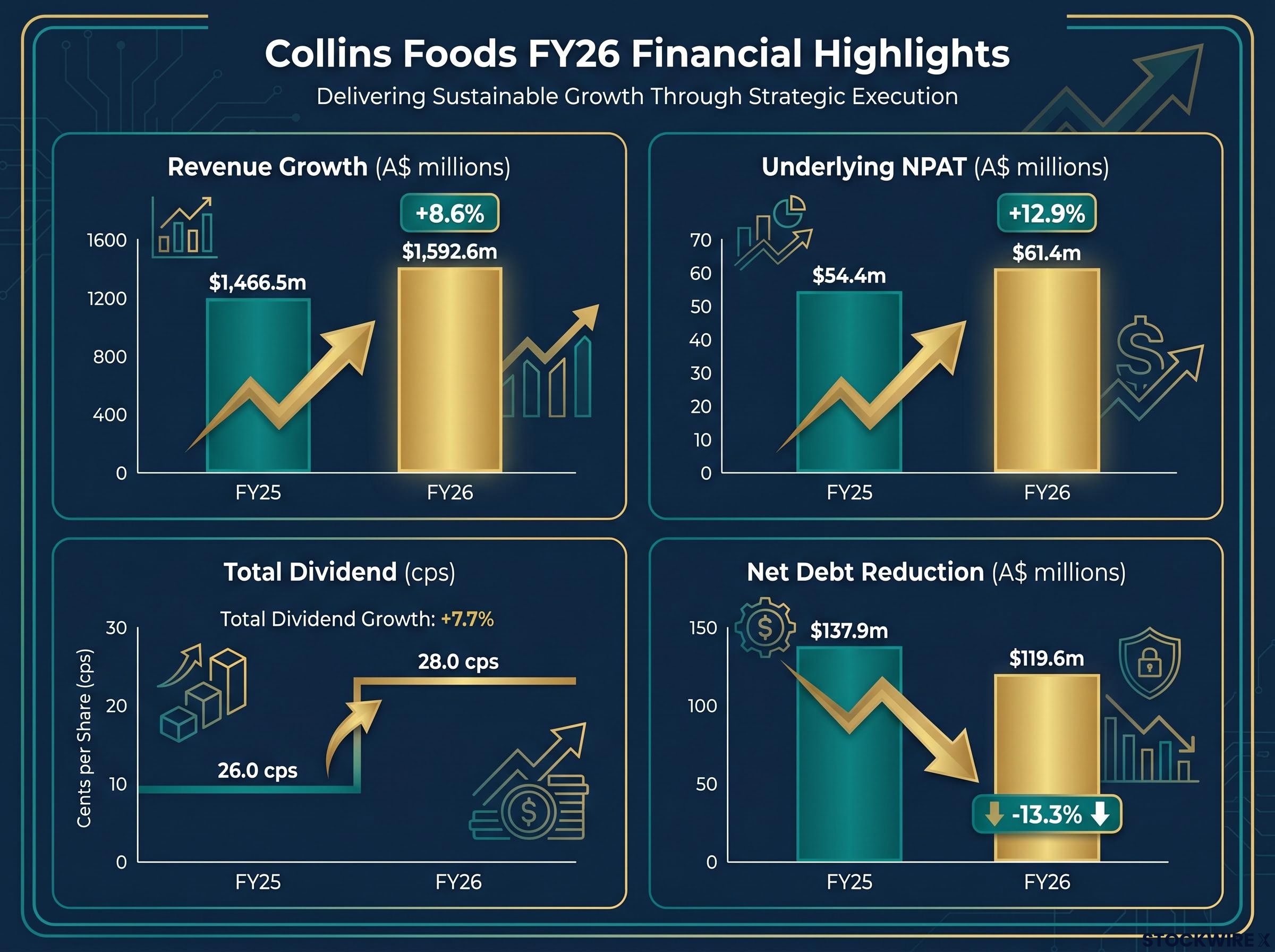

In its full-year FY26 results released 30 June 2026, Collins Foods recorded record revenue of $1,592.6m from continuing operations excluding Taco Bell, up 8.6% on FY25’s $1,466.5m. The result covered a 53-week reporting period, compared with FY25’s 52 weeks.

Underlying net profit after tax (NPAT) reached $61.4m, up 13.0% on the prior year’s $54.4m, while statutory NPAT lifted to $47.1m from $12.4m in FY25. The company declared a total fully franked FY26 dividend of 28.0 cents per share (cps), up from 26.0 cps.

The year also included the negotiated exit from Taco Bell, allowing the company to sharpen its focus on its core KFC network. Record top and bottom-line results alongside a higher dividend point to operational momentum across the KFC business in Australia and Europe.

When big ASX news breaks, our subscribers know first

FY26 financial results: margins, cash and a stronger balance sheet

Underlying EBITDA came in at $244.5m, up 6.3%, at a margin of 15.4%, down 34 basis points (bps). The company attributed the margin movement to changes in delivery fee structure, value investments made mid-year, and higher protein costs in Europe.

Underlying EBIT rose 10.1% to $130.7m, with earnings per share (EPS) of 52.0 cps, up from 46.1 cps in the prior year. Net operating cash flow was $150.1m, down $31.3m, which the company linked to the timing of royalty payments (14 in FY26 versus 12 in FY25) and higher tax paid.

The balance sheet strengthened over the period. Net debt fell to $119.6m from $137.9m, the net leverage ratio improved to 0.77 from 0.93, and return on equity (ROE) lifted 220 bps to 14.5%.

| Metric | FY26 Underlying | FY25 Underlying | Change |

|---|---|---|---|

| Revenue ($m) | 1,592.6 | 1,466.5 | 8.6% |

| EBITDA ($m) | 244.5 | 230.1 | 6.3% |

| EBIT ($m) | 130.7 | 118.7 | 10.1% |

| NPAT ($m) | 61.4 | 54.4 | 13.0% |

| EPS basic (cps) | 52.0 | 46.1 | 12.7% |

| DPS (cps) | 28.0 | 26.0 | 7.7% |

| Net debt ($m) | 119.6 | 137.9 | $18.3m lower |

| Net leverage ratio | 0.77 | 0.93 | 0.16 lower |

The dividend mechanics for the year were as follows:

-

Final dividend: 15.0 cps fully franked

-

Interim dividend: 13.0 cps

-

Record date: 14 July 2026; Payment date: 11 August 2026

KFC Australia drives the engine; Europe builds momentum

KFC Australia — sales growth and productivity lift profits

KFC Australia delivered revenue of $1,241.3m, up 7.6%, with same store sales (SSS) growth of +2.7%, a marked improvement on FY25’s +0.3%. Restaurant-level EBITDA rose 6.2% to $260.5m, while EBIT lifted 6.6% to $155.8m.

The restaurant count increased by 7 to 295, supported by 8 new openings, 1 closure, and 1 relocation. The company also completed 33 remodels including 3 supercharged formats. The company noted a successful Cairns trial of Kwench by KFC, now moving to national rollout.

Brand metrics remained strong. KFC led the quick service restaurant (QSR) category in the YouGov Brand Index, as well as in Brand Satisfaction and Brand Recommendation through FY26.

KFC Europe — solid improvement in challenging conditions

KFC Europe recorded revenue of $351.3m, up 12.5% (or 7.0% on a constant currency basis), with EBIT up 94.7% to $14.9m. Germany delivered SSS of +3.7%, while the Netherlands posted SSS of 0.0%, both improvements on the prior year.

The European restaurant count rose by 2 to 80. In Germany, the Munich acquisition of 8 restaurants completed on 1 June 2026, lifting the German count to 25 and making Collins Foods “the largest KFC franchisee in Germany by system sales.” The Munich restaurants are not included in the FY26 results.

The Bavarian KFC acquisition completed on 1 June 2026, growing Collins Foods’ German portfolio by approximately 50% and covering states that represent more than half of Germany’s population and around 54% of its GDP.

In the Netherlands, the Corporate Franchise Agreement (CFA) was extended three years to 31 December 2029, with Yum! Brands to resume marketing responsibilities from 1 January 2027.

What “same store sales” and the QSR franchise model mean for investors

Collins Foods operates KFC under franchise from Yum! Brands. Growth in this model is driven by new restaurant development, remodels, menu innovation, and operational efficiency.

-

SSS: underlying demand from existing restaurants

-

Network expansion: new openings, remodels and acquisitions

-

Yum! relationship: brand strength and operational support

The Taco Bell exit and the runway ahead

Taco Bell exit successfully negotiated

The Taco Bell exit was announced 31 March 2026, with 20 restaurants transferring to a joint venture between a subsidiary of Yum! and Restaurant Brands Australia. The remaining 7 restaurants were closed during FY26.

Trading and capital expenditure exposure on the transferring restaurants ceased 1 April 2026, with completion expected July to August 2026. One-off closing costs of $1.7m were recognised, and the company expects a one-off gain in FY27 relating to lease liability transition and reversal, subject to negotiated outcomes. The exit allows the company to concentrate on its core KFC business.

Strategic growth priorities and FY27 investment

In Australia, the company plans a national rollout of Kwench by KFC across FY27 and FY28, with capex of $35m in FY27 and $10m in FY28, targeting 80% coverage by April 2027 and 100% by mid-2027. Additional initiatives include late-night trade expansion, a breakfast trial, and the “GO FULL CHICKEN” brand relaunch.

Germany has been positioned as the company’s “second strategic growth pillar”, with an ambition to grow the network by 45–90 additional restaurants by FY30. FY27 plans include approximately $20m in capex plus $3m of incremental general and administrative (G&A) investment. Group FY27 capex guidance was set at approximately $80–$100m.

The next major ASX story will hit our subscribers first

FY27 trading update and outlook

In the first 8 weeks of FY27, Australia recorded total sales growth of +6.7% and SSS of +4.0%, which the company described as a strong start led by its main profit engine. Europe trading was below expectation: Germany total sales rose +26.4% (including 4 weeks post-Munich) but SSS was (7.2)%, while the Netherlands recorded total sales of (5.2)% and SSS of (7.8)%.

Management cited conflict in the Middle East, fuel prices, a prolonged heatwave affecting restaurant traffic, and the lapping of a strong Squid Game limited time offer (LTO) comparator as factors weighing on European performance. The company noted it is working with Yum! on short and long-term initiatives.

On costs, the company reported flat-to-modest commodity inflation in Australia and deflation in Europe. Labour inflation remained elevated and is being addressed through AI-powered operations and automation. Avian influenza cost impacts in Europe are expected to dissipate over FY27, with no cases currently detected in Australian poultry.

The company summarised its four FY26 strategic achievements as follows:

-

Lifted performance in Australia

-

Enabled growth pathway in Germany

-

Improved profitability in the Netherlands

-

Successfully negotiated Taco Bell exit

Don’t Miss the Next Consumer Sector Winner

Big News Blast delivers FREE breaking ASX announcements straight to your inbox within minutes of release, complete with in-depth analysis already done for you. Over 20,000 subscribers rely on it to stay ahead of market-moving news across Consumer, Tech, Healthcare and more. Click the “Free Alerts” button to get started today.