Stakk Ltd Forecasts Maiden Operating Profit and A$21.8M FY2027 Revenue Outlook

Stakk forecasts maiden operating profit and unveils $21.8 million FY2027 revenue outlook

Stakk Ltd (ASX: SKK) expects to report a maiden profit from operating activities for FY2026, driven by a run of customer wins and accelerating revenue growth. The Board described the result as evidence of its strategy taking hold across regulated industries.

The trading update, dated 30 June 2026, carries a dual message. The Company expects FY2026 revenue of approximately A$13.55 million, alongside a forward FY2027 revenue outlook of approximately A$21.8 million based solely on executed customer agreements already disclosed to the market, assuming no further customer wins.

Stakk describes itself as “a leading AI-native Digital Trust infrastructure provider for regulated industries.” All financial figures in the update derive from the Company’s unaudited management accounts and remain subject to completion of year-end reporting, external audit procedures and final Board approval. Accordingly, actual reported results may differ from the expectations set out by the Board.

When big ASX news breaks, our subscribers know first

The numbers behind the trading update

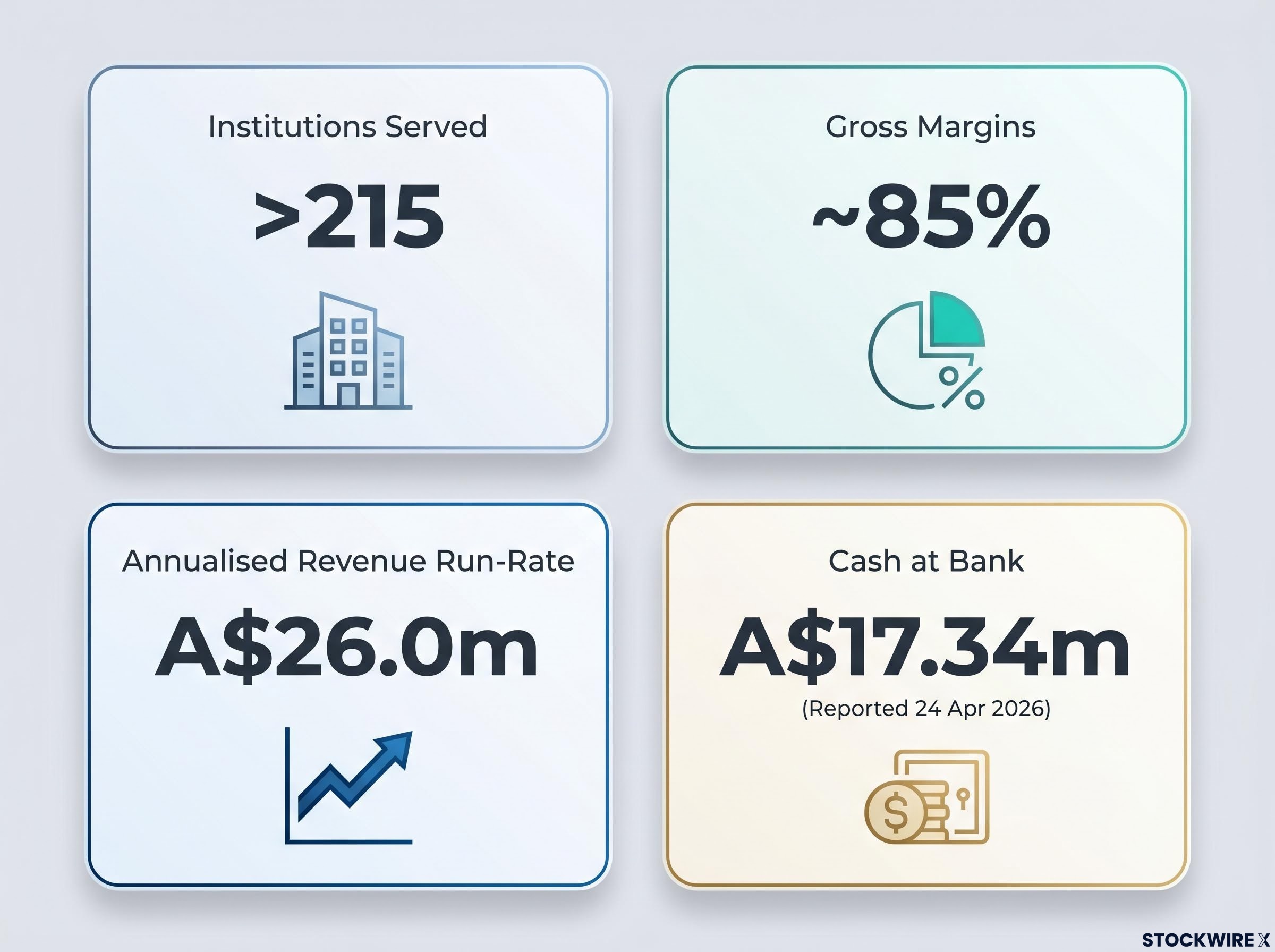

The update sets out a series of metrics spanning recognised revenue expectations, run-rate growth, cash receipts and margins. Together, they point to a business model the Board considers highly scalable.

| Metric | Figure | Context / Comparison |

|---|---|---|

| Expected FY2026 revenue | ~A$13.55m | From ordinary operating activities; subject to audit |

| Expected FY2027 revenue outlook | ~A$21.8m | Based solely on executed contracts, no further wins assumed |

| Annualised revenue run-rate | A$26.0m | Up from A$15.0m target set 29 Jan 2026; +2,067% vs 28 Dec 2024 figure |

| Gross margins | ~85% | Reflects scalability of recurring revenue model |

| Q3 FY2026 quarterly cash receipts | A$5.36m | more than 270% on prior quarter’s A$1.44m |

| Cash at bank (reported on 24 Apr 2026) | A$17.34m | Strengthened balance sheet position |

The annualised revenue run-rate of A$26.0 million has overshot the A$15.0 million target announced on 29 January 2026. Importantly, that earlier figure was an Annual Recurring Revenue (ARR) run-rate target, not guidance for revenue expected to be recognised during FY2026. The two metrics measure different things and should not be conflated.

The A$26 million run-rate milestone was reached when Stakk secured a second US healthcare client in early June 2026, adding approximately A$3.85 million in annualised revenue and validating the same AI-native infrastructure across a new regulated vertical.

Milestone payments and contract wins fuelling the growth

Recent executed customer agreements have materially expanded the Company’s contracted recurring revenue base. The Board points to two material contract wins and a pair of milestone payments received under previously disclosed schedules.

- 24 March 2026: customer agreement with an estimated contract value of US$5.5 million (~A$7.85 million)

The 24 March 2026 agreement, which represents the largest contract in the company’s history, introduced Stakk to the US healthcare vertical and established a 50/50 milestone payment structure that anchors the near-term cash receipts now reflected in the FY2026 update.

-

2 June 2026: further customer agreement with an estimated contract value of US$2.75 million (~A$3.85 million)

-

Recent payments received totalling US$3.693 million (~A$5.36 million), comprising US$3.0 million (~A$4.35 million) relating to the 24 March contract and US$693,000 (~A$1.01 million) relating to the 2 June contract

These are cash milestone payments tied to previously disclosed contractual schedules. For investors, they offer evidence that signed contracts are converting into cash receipts, not merely sitting on paper.

How Digital Trust infrastructure creates recurring revenue

Stakk operates AI-native Digital Trust infrastructure embedded within the “control path” of regulated systems. In practice, this means its technology sits inside the digital processes used by banks, credit unions, neobanks and fintech platforms, governing high-consequence digital interactions in real time.

The platform serves more than 215 institutions across Australia and the United States, working to prevent invalid or fraudulent activity from entering institutional core systems. It operates within a closed-loop, SOC 2 Type II compliant environment purpose-built for regulated institutions, combining federated signal intelligence, contextual digital personas, real-time authentication, orchestration and settlement.

Why does this matter to investors? Recurring software and managed services models carrying gross margins of approximately 85% can scale efficiently. This is the structural reason a maiden operating profit and a strengthening forward run-rate are credible.

Why the FY2027 outlook matters for investors

The Board frames the FY2027 revenue expectation of approximately A$21.8 million as a figure built on existing foundations rather than future ambition. The expectation is based solely on executed and disclosed customer agreements, with assumptions around implementation and Australian Accounting Standards revenue recognition.

Critically, the FY2027 expectation excludes any contribution from future customer acquisitions, cross-selling opportunities, expanded customer utilisation or pricing adjustments. Accordingly, any additional customer contracts secured during FY2027 would represent upside to the figures outlined.

The profitability timeline has also shifted forward. During Q3 FY2026, the Company expected to achieve profitability and positive operating cash flow by the end of the 2026 calendar year (31 December 2026). The Board now expects an operating profit for the financial year ending 30 June 2026, ahead of that earlier expectation, though this remains subject to audit and final Board approval.

The Board believes these expectations reflect the successful execution of the Company’s strategy of building a high-margin, recurring revenue business servicing regulated industries through long-term customer relationships.

The next major ASX story will hit our subscribers first

What comes next for Stakk

The forward path centres on completing the reporting cycle and continuing to convert contracted revenue into recognised income. The Board has flagged the following markers:

-

Completion of FY2026 year-end financial reporting, external audit and final Board approval, with all figures remaining subject to these processes

-

A FY2027 revenue trajectory toward approximately A$21.8 million from executed contracts, with any new wins representing potential upside

-

Continued conversion of customers from implementation into recurring production revenue

The balance sheet adds support to the outlook. The Company reported A$17.34 million cash at bank on 24 April 2026, gross margins of approximately 85% and a growing contracted recurring revenue base. The Board has stated these factors provide it with confidence in the Company’s outlook.

That confidence, however, remains anchored to the qualifiers running throughout the update. The figures are derived from unaudited management accounts and remain subject to completion of the FY2026 financial reporting process, external audit procedures, normal accounting adjustments and final Board approval.

Don’t Miss the Next ASX Tech Breakout

Big News Blast delivers FREE breaking ASX tech news directly to your inbox within minutes of release, complete with in-depth analysis. Over 20,000 active subscribers already rely on it to stay ahead of the market. Click the “Free Alerts” button at StockWire X to get the next major announcement the moment it drops.