Aft Pharmaceuticals Foreign Exempt NZX Eyes $300M Revenue as FY26 Sales Rise 22%

AFT Pharmaceuticals sets sights on $300M revenue as FY26 sales climb 22% to $254.7M

In its BIO 2026 investor presentation delivered in June 2026, AFT Pharmaceuticals Managing Director Dr Hartley Atkinson outlined a year of double-digit growth and reaffirmed a revenue goal of more than NZ$300M, which management said is now “in sight.”

The presentation detailed FY26 total sales of NZ$254.7M, up 22%, with operating profit of NZ$24.4M coming in ahead of guidance. A dividend of 2.5cps, up 39%, was also highlighted.

Management framed AFT as a diversified, internationally scaling specialty pharmaceutical business with more than two decades of uninterrupted growth, combining an established sales base with an expanding research and development (R&D) pipeline.

When big ASX news breaks, our subscribers know first

A multi-decade growth record gathering pace

Dr Atkinson told investors that FY26 operating revenue rose 22% to NZ$254.7M (FY25: NZ$208.0M), driven by double-digit sales growth across all territories. Product sales grew 19% in Australia, 66% internationally, and 41% across Asia.

Earnings growth was equally pronounced. EBITDA reached NZ$28.8M (FY25: NZ$20.9M), while operating profit climbed to NZ$24.4M (FY25: NZ$17.6M), enabling continued investment in international hubs and R&D. The presentation noted a 17.6% five-year compound annual growth rate (CAGR).

EBITDA is a non-GAAP measure of financial performance, with further detail available in the AFT Annual Report.

| Metric (NZ$M) | FY24 | FY25 | FY26 | Change (FY25→FY26) |

|---|---|---|---|---|

| Operating Revenue | $195.4M | $208.0M | $254.7M | +22% |

| Operating Profit | $24.2M | $17.6M | $24.4M | n/a |

| EBITDA | n/a | $20.9M | $28.8M | n/a |

AFT has delivered more than two decades of un-interrupted growth by identifying unmet clinical need and investing to develop and in-license intellectual property to meet those needs and improve health outcomes.

Expanding global footprint, now selling in 87 countries

The presentation positioned international scale-up as a central engine behind the NZ$300M-plus revenue target. Management highlighted that AFT’s medicines are now available in 87 countries, up from 80 in FY25 and 85 at the 1H FY26 mark, with Taiwan and Egypt among the newly added markets.

Distribution agreements now span more than 100 countries. International revenue from product sales and royalties rose 66%, while licensing revenue reached NZ$3.0M, up from NZ$0.7M in FY25. The company closed 9 licensing agreements in FY26.

AFT’s regional hub footprint includes:

-

Europe: UK and EU

-

North America: USA and Canada

-

Asia: China, Singapore, Malaysia and Hong Kong

-

Africa: South Africa

-

Australia and New Zealand, with head office in Auckland

Management indicated that the UK and South Africa hubs are expected to contribute to earnings in FY27, pointing to potential operating leverage as those hubs scale.

Understanding AFT’s two engines, established sales plus an R&D pipeline

AFT operates an established business alongside an R&D pipeline. The first engine is a profitable established business selling existing medicines across Australasia and international markets. The second is an R&D and in-licensing engine developing patented products for global markets.

As the presentation put it, AFT’s positive cashflows have positioned the company well to undertake and secure research and development projects either alone or in partnership with others.

A deep R&D pipeline targeting multi-billion-dollar markets

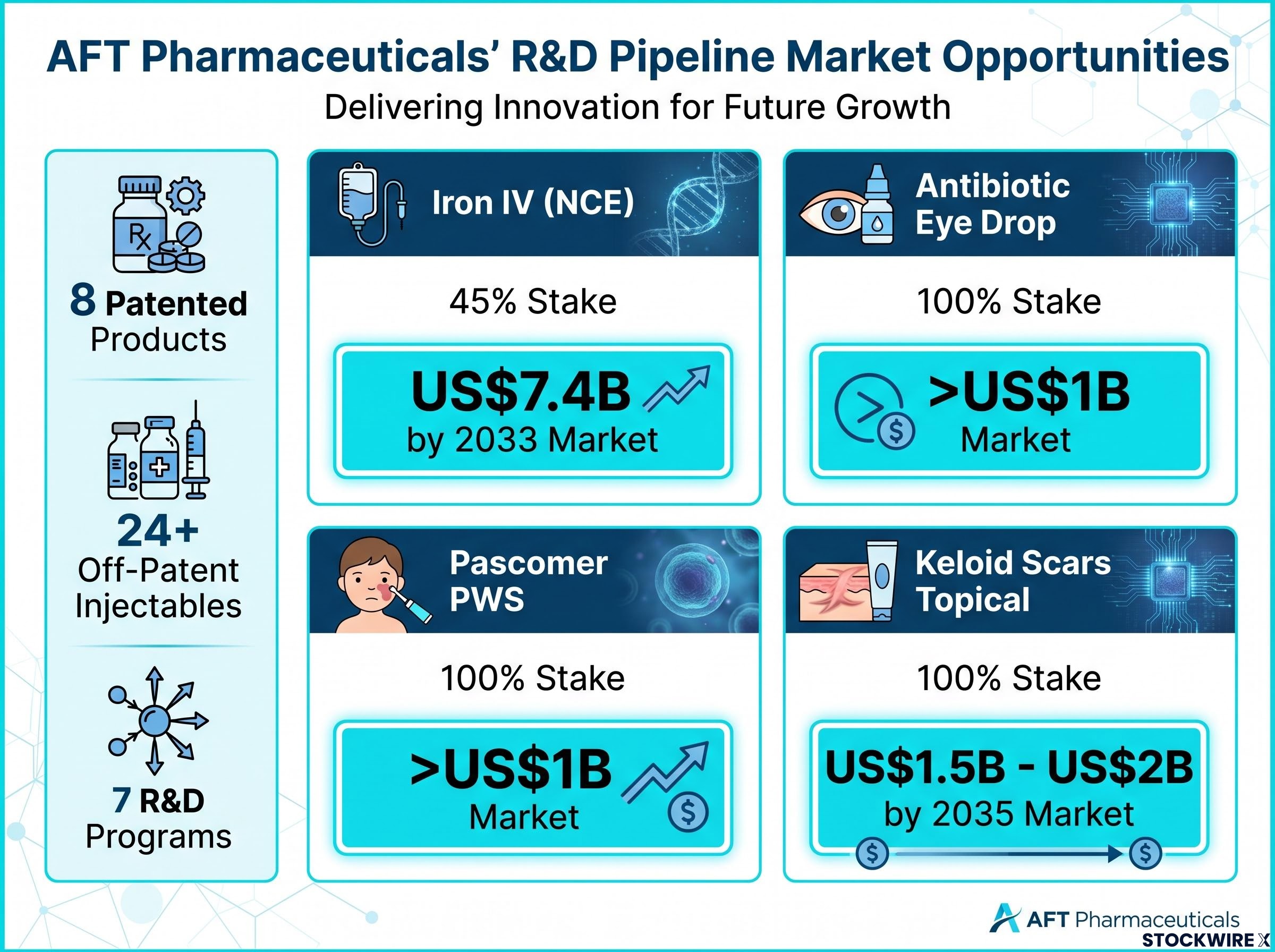

Management outlined an active R&D pipeline of 8 patented products, the progression of 24+ off-patent injectables, and 7 R&D programs currently being commercialised across multiple countries. R&D spend grew to NZ$18M in FY26 (FY25: NZ$15M).

The flagship programme is the Final Phase III NCE Injectable Iron global study. AFT is preparing a Phase III trial of approximately 1,366 patients, run by AFT across Armenia, China, Europe, India, Japan, New Zealand and the USA, supported by an open US FDA IND.

Initial Phase III data was described as positive, citing negligible free iron, the ability to administer a large single dose, a low incidence of adverse events, and no detected decreases in plasma phosphate. The market is projected at US$7.4B by 2033, with AFT holding a 45% stake.

Other pipeline highlights include Maxigesic in multiple dose forms, and Pascomer, an orphan indication for Facial Angiofibromas where licensing is underway. The Intravenous Iron Development Project has been licensed to Chengdu-based Grand Life Sciences Group, with the agreement including development and sales milestone payments.

The Pascomer appeal victory in March 2026 strengthened AFT’s commercial position on the programme, with the Court of Appeal confirming AFT retains full economics on non-orphan applications including Port Wine Stain, a patient population approximately 36 times larger than the Facial Angiofibroma orphan indication.

| Project | AFT Stake | Target Filing | Market Size | Status |

|---|---|---|---|---|

| Iron IV (NCE) | 45% | 4Q 28 | US$7.4B by 2033 | Positive initial Phase III; IND opened with FDA |

| Antibiotic eye drop | 100% (IP in-licensed) | 4Q 28 | >US$1B (analyst estimate) | Pre-IND filed; IND to be submitted 4Q 2026 – 1Q 2027 |

| Pascomer PWS | 100% | 1Q 28 | >US$1B | No approved treatment |

| 24 Hospital Injectables | 70% | 3Q 25 → 4Q 27 | US$450M | 5 dossiers to be filed by end FY27 |

| Keloid Scars Topical | 100% (IP in-licensed) | 3–4Q 29 | US$1.5B (growing to US$2B by 2035) | Formulation finalised; preparing pre-IND submission 4Q 26 |

Outlook, driving toward $300M revenue and higher earnings in FY27

Management set out a stated path toward the NZ$300M-plus revenue goal, aiming to extend AFT’s growth record in FY27 through the following drivers:

-

Continued expansion in Australasian markets

-

A strong programme of launches across international hubs

-

Increasing earnings contribution as those hubs scale, with the UK and South Africa expected to contribute in FY27

-

Continued progress in R&D and regulatory milestones

-

An active in-licensing and out-licensing programme

The presentation noted that AFT will continue to make significant investment during the financial year, with FY27 operating profit expected to reach between NZ$28M and NZ$32M. For investors, the guidance signals operating leverage even as the company reinvests for growth.

The next major ASX story will hit our subscribers first

What it means for investors

AFT’s update reinforces a dual-engine investment case: a profitable established business with a 22-year unbroken growth record, paired with a deep R&D pipeline targeting multi-billion-dollar markets.

The FY26 figures point to a consistent trajectory of rising revenue, expanding margins, and broadening geographic reach, now spanning 87 countries, with newly opened hubs expected to add to earnings in FY27.

With a clear FY27 operating profit target of NZ$28M to NZ$32M and a stated path toward more than NZ$300M in revenue, the presentation positioned AFT as continuing to balance near-term earnings with long-term pipeline optionality.

Don’t Miss the Next Healthcare Breakout

Big News Blast delivers FREE breaking ASX healthcare news to your inbox within minutes of release, complete with in-depth analysis already done for you. Join 20,000+ investors who stay ahead of the market the moment announcements drop. Click the “Free Alerts” button to start receiving real-time alerts today.