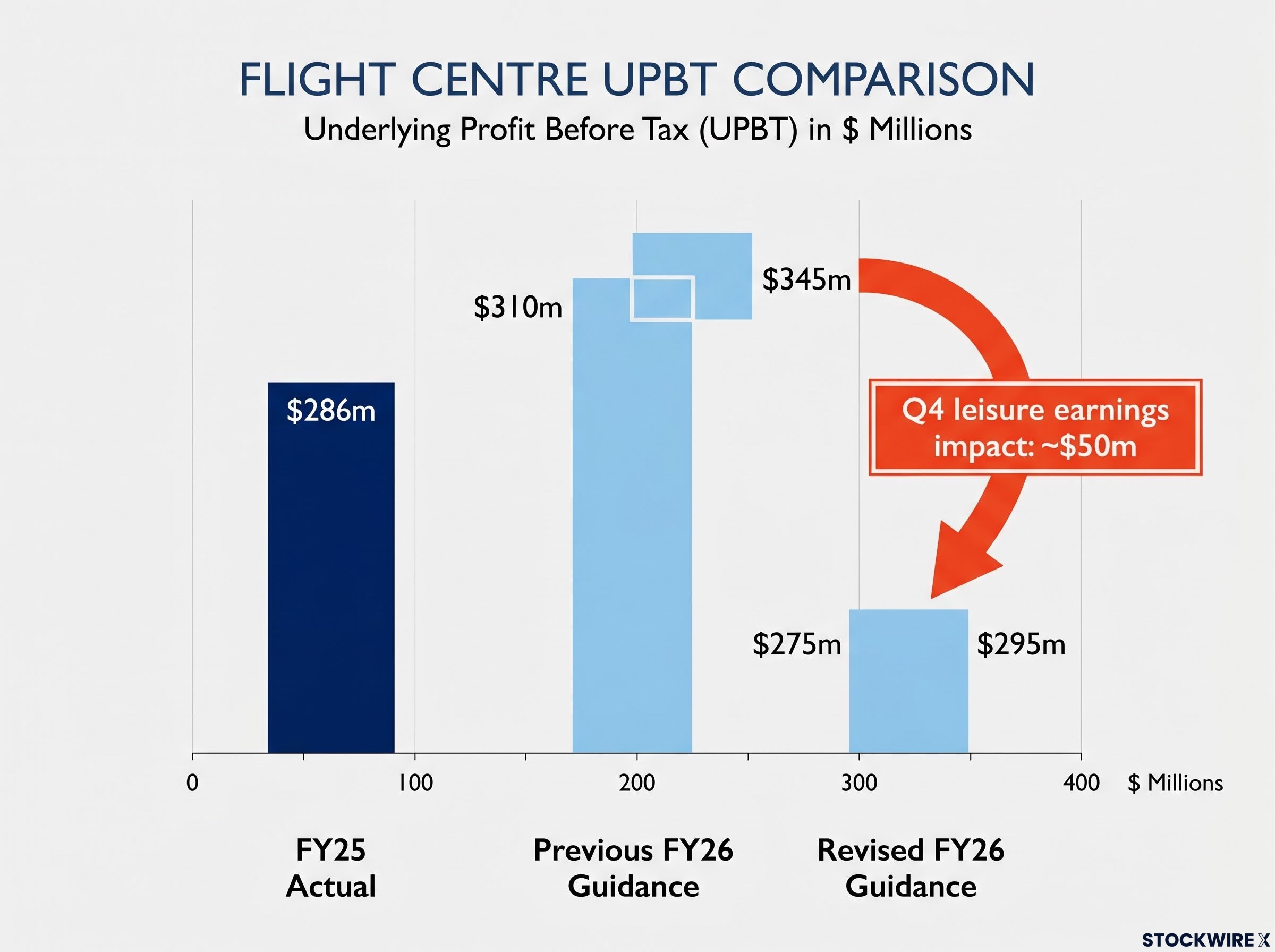

Flight Centre revises FY26 guidance to $275m-$295m amid Middle East disruption, launches $200m buy-back

Flight Centre Travel Group has revised its FY26 profit guidance to $275m-$295m and announced an up to $200m on-market share buy-back, after Middle East conflict disruption reduced expected leisure earnings during the peak travel season. The new underlying profit before tax (UPBT) guidance range sits below the previous target of $310m-$345m, with the midpoint broadly in line with FY25’s $286m UPBT. The revision reflects temporary, conflict-driven headwinds layered over what management describes as a very solid underlying year, with the business delivering almost 10% UPBT growth to $227m across the first three quarters.

The dual announcement signals management conviction in the business’s recovery trajectory. Despite the near-term disruption, the Board has initiated a new $200m buy-back programme following the successful May 2026 completion of a similar programme that repurchased 16.2 million shares (7.3% of issued capital). The peace agreement reached this week provides a clearer runway into FY27 and a significant earnings tailwind, though its timing means limited FY26 impact.

When big ASX news breaks, our subscribers know first

How geopolitical shocks affect travel stocks

Travel companies are particularly sensitive to geopolitical events because international leisure bookings rely on stable air routes, predictable transit hubs, and consumer confidence in safe passage. When conflicts disrupt major travel corridors, customers typically respond in two ways: they either reroute via alternative hubs (often switching to lower-margin carriers) or defer bookings entirely until uncertainty clears. This creates sharp short-term earnings volatility.

The travel sector has historically demonstrated strong resilience following such disruptions. Short-term downturns are typically followed by rapid and steep rebounds as pent-up demand releases once normalcy returns. Leisure travel is discretionary and deferrable, which amplifies immediate booking slowdowns during crises but also concentrates recovery demand into compressed periods. Understanding this cyclical pattern helps investors assess whether a guidance revision reflects structural business deterioration or a temporary external shock.

Q4 leisure earnings hit by $50m as conflict disrupts peak travel season

The Q4 leisure earnings impact is expected to reach approximately $50m compared to previous expectations, after the business was tracking towards a $200m UPBT at the end of Q3. This shortfall stems from two temporary shifts in travel and booking patterns triggered by escalating Middle East hostilities during the peak travel season.

Customers with forward bookings to the UK and Europe — Flight Centre’s largest and highest-value international leisure destinations — routed via the Middle East typically amended or cancelled plans. Those who rerouted via Asia or the Americas to bypass the region typically switched to lower-margin carriers, compressing profitability per transaction. A concurrent slowdown in longer-haul bookings occurred as ongoing volatility, capacity constraints, and higher fuel prices drove airfare price spikes. Enquiry has remained healthy — up 18% month-to-date in the Flight Centre brand in Australia — but customers have been deferring bookings, a typical response during uncertain times.

Additional impacts include approximately $5m in UK-based touring business cancellations linked to Middle East-related disruptions, and a $5m-$10m adverse profit translation impact from the stronger Australian dollar. The Australian Government’s Do Not Travel advisory for key Middle Eastern transit hubs has impeded recovery by stripping Australians of travel insurance cover for non-war-related issues while merely transiting the region, a step above comparable countries including the United Kingdom.

Graham Turner, Managing Director

“The change in our short-term expectations reflects a temporary, conflict-driven headwind layered over what was shaping as a very solid year. It has been driven by an external shock – the Middle East conflict disrupting peak leisure travel – not by a deterioration in our underlying business.”

Strong first three quarters masked by Q4 disruption

Corporate business delivers profit growth despite headwinds

Flight Centre’s underlying performance remained robust across the first nine months of FY26, with the group recording almost 10% UPBT growth to $227m during the first three quarters. Q3 profit growth accelerated to approximately 20% compared to the FY25 Q3, culminating in a record profit in Australia in March despite escalating Middle East hostilities. This performance demonstrates the strength of the business prior to the peak-season leisure disruption.

Flight Centre entered Q4 having already posted record $19.5 billion TTV for the nine months to March 2026, with corporate UPBT growing 23% to $177 million on only 4% TTV growth, a combination that demonstrated expanding operating leverage before the conflict-driven leisure disruption hit.

The global corporate business has been less affected by the conflict and remains on track to deliver strong FY26 profit growth. Corporate business growth drivers include:

- Growing operating leverage as scale increases across existing accounts

- New offerings expanding addressable markets beyond traditional managed travel

- Blockskye partnership strengthening US presence and enabling competition for some of the world’s largest accounts

- Accelerating contract win pipeline late in FY26

The corporate segment’s resilience reflects its focus on business-critical travel, which is less discretionary and less dependent on Middle Eastern transit routes than leisure bookings to Europe.

$200m buy-back signals Board confidence in recovery outlook

The new buy-back will be conducted on-market over the next 12 months at Flight Centre’s discretion, following the successful completion of a similar programme in May 2026 that bought back 16.2 million shares (7.3% of issued capital). The buy-back is subject to prevailing share price and market conditions, and the company reserves the right to suspend or terminate the programme at any time.

The strategic rationale centres on three objectives: reducing the number of shares on issue, driving earnings per share (EPS) growth, and offsetting potential dilution associated with the outstanding Convertible Notes. The final amount and exact timing of trades will depend on market conditions, Flight Centre’s prevailing share price, future capital requirements, and any unforeseen developments that may arise during the buy-back period.

Managing Director Graham Turner stated that the Board’s decision to launch the buy-back “clearly signals that we see our shares as undervalued at current levels.” A $200m buy-back during a guidance downgrade is an atypical capital allocation decision that reflects management’s conviction in the business’s intrinsic value and recovery trajectory. The programme will be executed in addition to managing outstanding Convertible Notes and maintaining the existing capital management policy.

The buy-back sits within a broader capital management sequence that includes the Pedal Group divestment completed in May 2026, which returned $61.7 million in cash proceeds and an approximate $15 million accounting gain as Flight Centre simplified its portfolio ahead of the recovery phase.

Cost discipline and AI deployment underpin margin protection

Flight Centre continues to focus on short-term savings initiatives, including reducing discretionary spend, freezing support role recruitment, and prioritising investment and capital expenditure. This cost discipline is balanced against ongoing investment in key growth drivers — including network enhancements, marketing, and new customer offerings — to ensure the business is well placed to capitalise during the recovery phase.

The company continues to deploy artificial intelligence (AI) and automation group-wide to lift productivity, reduce cost, and open new sources of revenue, while also deepening its competitive moat. Enhancing the customer experience (CX) through AI is a priority, as evidenced by recent developments:

- Sam and Mel AI-powered assistants (FCM and Corporate Traveller) – broad rollout commencing this week

- Google Agent Search – AI-powered search experience launched for leisure customers

- AI Travel Assistant – upcoming feature giving customers easy access to frequently requested pre-trip information and proactive notifications

FY27 runway clears as peace agreement provides earnings tailwind

The peace agreement reached this week provides a clearer runway into FY27 and a significant earnings tailwind, though its timing means it is unlikely to meaningfully alter the company’s FY26 fourth quarter result trajectory.

Flight Centre’s leisure strategy continues as the business works to strengthen the Flight Centre brand, expand in growth sectors including cruise, tour, and luxury, and embed the new World360 Rewards programme, which now has more than 420,000 members. The $200m profit milestone the business was on track to achieve during FY26 remains a viable near-term target given that travel downturns are historically short and followed by rapid rebounds.

Key figures at a glance

| Metric | Value |

|---|---|

| Revised FY26 UPBT guidance | $275m – $295m |

| Previous FY26 UPBT guidance | $310m – $345m |

| FY25 UPBT (adjusted) | $286m |

| 9M FY26 UPBT | $227m |

| Q4 leisure earnings impact | ~$50m |

| New buy-back programme | Up to $200m |

| Previous buy-back completed | 16.2m shares (7.3%) |

| World360 Rewards members | 420,000+ |

Want the Next Travel Sector Breakout in Your Inbox?

Join 20,000+ investors getting FREE breaking ASX news delivered within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at Big News Blast to start receiving real-time alerts the moment market-moving announcements drop across travel, retail, finance, tech, and more.