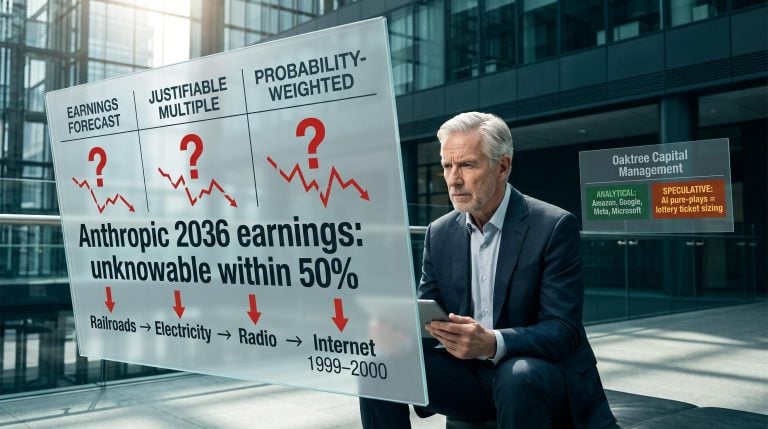

Two companies with no public financial disclosures and no confirmed path to positive free cash flow are collectively valued at nearly $1.8 trillion in private markets, and both are preparing to ask public investors to underwrite that number. Anthropic’s Series H closed at a $965 billion post-money valuation on 28 May 2026. OpenAI’s latest round closed at $852 billion on 31 March 2026. Neither company has filed a public S-1 registration statement as of 16 June 2026. The combined figure rivals the market capitalisation of any single S&P 500 constituent and dwarfs every IPO cohort since 2022. What follows is a dissection of what those valuations actually require to be true: the revenue projections, capital commitments, enterprise adoption data, and macro conditions that either validate or undermine the investment case for the most anticipated listings in a generation.

The $1.8 trillion number and where it comes from

The two headline valuations are anchored to specific, confirmed private funding rounds, not to any forward IPO pricing assumption.

| Company | Latest round | Capital raised | Post-money valuation | S-1 status (as of 16 June 2026) |

|---|---|---|---|---|

| Anthropic | Series H | $65 billion | $965 billion | No public filing confirmed |

| OpenAI | Latest round (March 2026) | $122 billion | $852 billion | No public filing confirmed |

Combined, these two private-market valuations approach $1.8 trillion, a figure that would place the pair among the five largest publicly listed companies in the world if taken at face value. That comparison carries weight precisely because these are not publicly listed companies. They are private firms whose financial performance has never been subjected to audited public disclosure.

Why the absence of public filings matters for analysis

Without audited financials in a public S-1, every revenue and profitability figure circulating in market commentary is a third-party projection or sell-side model estimate, not company-disclosed data. Anthropic’s autumn 2026 listing remains plausible given its Series H capital structure, but it should be treated as anticipated rather than formally confirmed. The same applies to OpenAI’s reported IPO timeline. Every quantitative claim in the sections that follow carries that qualification.

The IPO structural mechanics that consistently favour insiders over public-market entrants apply with particular force here: retail investors who cannot access shares at the offering price enter the secondary market after institutional allocations are filled, effectively paying a premium before lockup expiry introduces additional insider supply.

The Form S-1 disclosure requirements mandated by the SEC, covering audited financials, material business risks, and use-of-proceeds details under Regulation S-K and S-X, are precisely the obligations that will make Anthropic and OpenAI’s financial performance publicly verifiable for the first time once filings are submitted.

When big ASX news breaks, our subscribers know first

What the AI industry’s adoption data actually shows

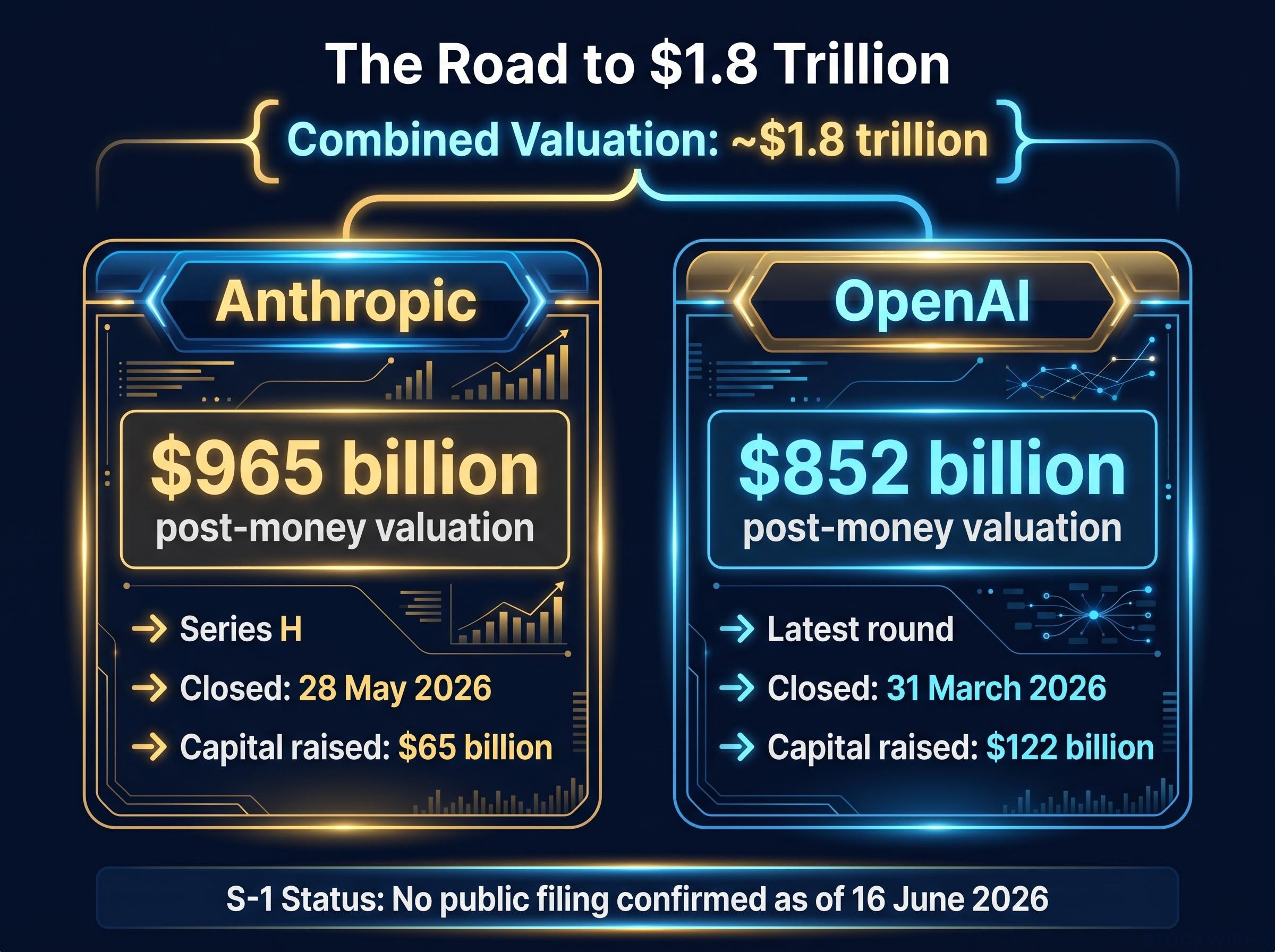

The demand signal is real. According to the McKinsey 2025 State of AI Global Survey (published November 2025), 88% of surveyed organisations reported using AI in at least one business function. That figure suggests a technology already embedded in corporate workflows at a scale few enterprise software categories have achieved this quickly.

The earnings conversion tells a different story.

- 88% of organisations using AI in at least one function (self-reported)

- 31-33% actively scaling AI usage beyond initial deployment

- 39% reporting measurable positive EBIT impact from AI adoption

- 30% having experienced at least one inaccurate AI output

These are survey self-reported figures, not independently audited data. Even so, the pattern is consistent with prior McKinsey surveys tracking the same adoption curve.

The McKinsey 2025 State of AI survey, covering responses from organisations across more than 100 countries, provides the primary data behind the 88% adoption and 39% EBIT impact figures, and its methodology notes that self-reported impact estimates are subject to optimism bias, a caveat that matters when using these numbers to anchor vendor revenue projections.

Only 39% of organisations deploying AI report measurable positive EBIT impact, meaning the majority of current AI deployment has not yet converted into quantifiable financial returns.

The gap between 88% adoption and 39% earnings impact is the single most telling data point for investors evaluating AI vendor valuations. Inaccuracy in AI outputs is not merely a product complaint; in regulated and high-stakes domains, it functions as a structural cap on the economically exploitable portion of the addressable market. The addressable market that actually generates earnings for AI vendors is meaningfully smaller than the addressable market that has adopted the technology.

How frontier model economics actually work (and why they are structurally unusual)

Investors evaluating these IPOs need to distinguish between three layers of profitability, because only one of them ultimately supports equity value in a capital-intensive business:

- Operating income: Revenue minus operating expenses, including cost of goods sold and sales, general, and administrative costs. This is the metric most commonly referenced in early-stage growth narratives.

- Net income: Operating income minus interest, taxes, and non-operating charges. This captures the full cost of the business as a going concern.

- Free cash flow after capital expenditure: Net income adjusted for non-cash items, minus the capital expenditure required to maintain and grow the business. For companies spending hundreds of billions on compute infrastructure, this is the only metric that captures what is left for equity holders.

Anthropic’s implied forward price-to-sales multiple sits at approximately 22x on an annualised revenue run-rate of roughly $44 billion, derived from a third-party quarterly revenue projection of $10.9 billion for Q2 2026. This is not a disclosed figure. OpenAI is reported to be generating approximately $25 billion in annualised revenue, with projected cumulative compute expenditure through 2030 estimated at $600 billion. Neither figure is corroborated by public filings or management guidance.

Among the three major 2026 AI IPO candidates, Anthropic was the only one projected to approach operational profitability in 2026.

The pricing transition risk

A shift from subsidised, below-cost pricing to cost-reflective, token-based consumption models is structurally necessary for these businesses to reach profitability. The transition is underway across the industry. What has never been stress-tested at scale is whether enterprise customers will maintain current consumption volumes at sustainable price points. Below-cost pricing and free tiers have built adoption curves that may not survive the move to margin-positive pricing, making historical growth rates a potentially unreliable guide to durable revenue.

Frontier model pricing durability is under independent structural pressure from open-source models that have repeatedly closed the benchmark gap to prior-generation frontier systems within 6-12 months of release, compressing the window during which frontier API charges can be sustained at scale without accelerating customer migration to lower-cost alternatives.

Five questions institutional investors will ask before committing capital

- Will demand hold at cost-reflective pricing?

The industry has subsidised usage to build adoption. Whether enterprise consumption remains at current levels once pricing reflects true compute and infrastructure costs is unproven. Every revenue model that assumes current growth rates are durable depends on the answer.

- How durable is the competitive moat?

General-purpose technologies historically experience margin compression as competition enters and tools commoditise. Without proprietary data advantages, ecosystem lock-in, or material switching costs, early movers in prior technology waves have frequently lost pricing power within a decade.

- When does free cash flow turn positive?

All three major 2026 AI IPO candidates were spending well in excess of revenues on infrastructure and model development. Operating profitability is not the same as free cash flow after capital expenditure. Only the latter supports equity value.

- Can the S&P 500 absorb these names?

S&P 500 eligibility generally requires profitability for new constituents. At current financial profiles, neither Anthropic nor OpenAI would qualify for immediate index inclusion, limiting the passive capital flows that typically support mega-cap valuations post-IPO.

The AI valuation trap is most acute for passive investors who may never have explicitly chosen this exposure: if index committees waive standard profitability requirements for inclusion, passive funds and retirement accounts could be mechanically obligated to buy these shares at prevailing prices, removing any valuation discretion from the allocation decision.

- Why go public now, at these valuations?

Listing while still structurally reliant on external capital and at near-trillion-dollar private valuations raises a legitimate question about the primary purpose of the offering: funding future infrastructure, or crystallising gains for existing investors at attractive prices. The answer is likely both, but the weighting matters.

| Risk area | Unresolved variable | Resolution evidence |

|---|---|---|

| Pricing sustainability | Enterprise demand elasticity at cost-reflective prices | Post-transition renewal rates and consumption data in first public earnings |

| Competitive moat | Whether margin compression follows the general-purpose technology pattern | Gross margin trajectory over 4-6 quarters; open-source model performance parity |

| Free cash flow timeline | Capex-to-revenue ratio normalisation | Disclosed capex plans and burn rate relative to IPO proceeds |

| Index eligibility | Profitability requirement for S&P 500 inclusion | Audited net income in first full fiscal year post-IPO |

| Insider motivations | Proportion of proceeds allocated to growth versus secondary sales | Use-of-proceeds disclosure and lock-up structure in S-1 filing |

The margin of safety at 20-plus-times forward sales is effectively zero under standard discounted cash flow sensitivity analysis. Each unanswered question compounds the uncertainty rather than existing in isolation.

The macro environment these IPOs are entering

Even if the company-level thesis proves correct, the external environment amplifies the sensitivity of these particular instruments to forces outside management’s control.

The S&P 500 was trading at a price-to-earnings ratio of approximately 31x as of mid-2026. U.S. Treasury yields were approaching 5%. The ten largest S&P 500 constituents, the majority of which carry material AI-related business exposure, collectively represented approximately 35-40% of total index weight.

Passive index investors already carry concentrated AI sector risk through existing top-10 S&P 500 holdings. Sector underperformance is not merely an active stock-picking problem; it is systemic for anyone holding a broad market index fund.

Why long-duration growth equities are especially rate-sensitive

Businesses whose value is predominantly derived from cash flows projected five to ten years into the future suffer disproportionate present-value decline when the discount rate rises, compared to businesses generating cash today. A move from 5% to 6% in risk-free rates applied to a company valued at 20-plus-times forward sales with back-loaded cash flows produces a materially larger reduction in present value than the same rate move applied to a mature, near-term cash generator. At these multiples, the discount rate is not a background variable. It is the variable.

The simultaneous capital raise by multiple AI companies also creates a crowding dynamic that may affect pricing and capital allocation across other asset classes.

Standard Chartered’s global CIO has specifically flagged market absorption difficulties this summer as a consequence of the near-simultaneous listing timeline, noting that even genuine institutional demand for new issuance behaves differently when multiple mega-offerings compress into a single calendar window.

What the bulls are actually betting on

The investment decision is not a binary vote on whether AI is transformative. That is close to consensus. It is a probabilistic bet on value capture specifics: which firms, how fast, at what margins, and at what cost of capital.

For the bull case to deliver at these valuations, four conditions need to hold simultaneously:

- Sustained revenue growth at scale for multiple years, with these companies capturing a very large share of global AI spend

- Material gross margin expansion as compute costs decline, model efficiency improves, and cost-reflective pricing is accepted by enterprise customers

- Durable competitive moat retention, with these firms keeping a large share of the value they create rather than seeing it competed away by other labs, open-source models, or vertically integrated incumbents

- A supportive macro and regulatory environment, including no sustained regime of very high real rates and no sudden regulatory action dramatically raising costs or constraining deployment

The bull case is coherent. Some of the required conditions, particularly compute cost deflation and enterprise adoption acceleration, have meaningful supporting evidence. The $122 billion OpenAI round and $65 billion Anthropic round represent substantial capital commitments from sophisticated institutional investors who have conducted detailed private due diligence. The McKinsey finding that 88% of organisations have adopted AI is a real demand signal, even if earnings conversion lags.

What to watch in the first 12 months post-IPO

Three to four specific disclosures will serve as early signals on whether the thesis is tracking: gross margin trajectory in the first public earnings cycle, free cash flow burn rate relative to IPO proceeds, enterprise contract renewal and expansion rates, and any disclosure of compute cost per token. These are the metrics that will separate the narrative from the financials for the first time.

The only honest verdict: what you are actually buying at $1.8 trillion

The cumulative weight of the evidence points to a precise conclusion. The $1.8 trillion combined valuation, anchored to Anthropic’s $965 billion Series H and OpenAI’s $852 billion latest round, is not unreasonable if all four bull-case conditions hold simultaneously. Each condition is individually uncertain. Collectively, the probability of all four holding is lower than any single one.

The margin of safety at these valuations is structurally near zero. The downside from assumption failure compounds rapidly, while the upside from exceeding expectations is already largely priced in. The adoption-to-earnings gap, 88% deployment versus 39% measurable EBIT impact, remains the clearest evidence that the distance between AI’s real-world footprint and its measurable financial return is still the central open variable.

Public investors will, for the first time, have audited financials to evaluate once S-1 filings are made public. Until then, every valuation argument rests on projections.

The question is not whether AI transforms the economy. It is which companies capture how much of that value, how fast, at what margins, and at what cost of capital.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced in this article are third-party estimates, not company-disclosed figures. Past performance does not guarantee future results.