Nine Unveils Sofa to Street Strategy in QMS Acquisition Investor Briefing

Nine’s outdoor expansion takes audience reach from sofa to street

In its June 2026 investor briefing, Nine Entertainment Co. detailed the strategic rationale behind the QMS Media acquisition, positioning the move as a deliberate pivot toward growth verticals with structural resilience. The presentation outlined how the transaction has fundamentally rebalanced Nine’s portfolio, with growth assets now representing approximately 60% of revenue and 70% of EBITDA.

The QMS Media acquisition was announced at an $850 million enterprise value, structured to deliver low double-digit EPS accretion after accounting for the concurrent divestment of Nine Radio and NBN regional TV assets and a $178 million tax benefit embedded in the transaction.

Management framed the QMS acquisition as an extension that prioritises quality of revenue and long-term relevance as media consumption continues to fragment across platforms. The deal establishes what Nine characterises as “Sofa to Street” engagement capability — connecting audiences across streaming, broadcast, publishing and outdoor advertising environments through a unified data and targeting infrastructure.

When big ASX news breaks, our subscribers know first

What is out-of-home advertising and why does it matter?

Out-of-home (OOH) advertising encompasses digital billboards, street furniture screens, retail displays and other physical advertising formats located in public spaces. Unlike traditional broadcast or digital media consumed at home, OOH reaches audiences during daily movement through urban environments, shopping centres and transport networks.

The presentation highlighted OOH’s structural growth trajectory in Australia, where revenue has nearly tripled since 2010, making it the fastest-growing advertising segment. A key driver of this expansion is digital penetration: 77% of Australian OOH revenue is now digital, up from 54% in 2019. In New Zealand, digital accounts for 80% of industry revenue compared to approximately 59% five years ago.

For investors, OOH’s resilience stems from its role as attention becomes increasingly fragmented across streaming platforms, social media and traditional broadcast. Physical screens in high-traffic locations provide advertisers with guaranteed viewability and contextual relevance that digital environments cannot replicate at the same scale.

QMS positioning in the Australian and New Zealand markets

Management positioned QMS as the fastest-growing outdoor media operator in Australia, with a premium network concentrated in metropolitan markets. The company has systematically expanded market share through contract wins and digital conversion, supported by long-dated lease agreements that provide revenue visibility.

Market share trajectory:

- Australian market share: from 10% to 15% over the past six years

- NZ market share: 21% (2024) → over 30% (2026)

- 96% of QMS Australian revenue is digital, exceeding the 77% industry average

- More than 80% of Australian media revenue is attached to leases expiring after June 2030

QMS over-indexes in higher-margin categories, with approximately 60% of Australian revenue from roadside billboards and more than 30% from street furniture. This portfolio mix positions the business above industry-average digital penetration and supports margin expansion as the network matures.

The extended lease profile — with a weighted average expiry of approximately eight years in Australia and seven years in New Zealand — provides structural revenue stability. Approximately one-third of FY27 lease expiries are rolling month-to-month arrangements, while 82% of Australian revenue by lease value extends beyond June 2030.

Financial performance and earnings outlook

QMS has delivered three consecutive years of double-digit revenue and EBITDA growth, supported by new contract deployments and organic site expansion. Management provided FY26 EBITDA guidance of $86-88 million (pre-AASB16 basis), representing 12-15% growth on FY25’s $76.7 million.

The deal completion milestone in March 2026 removed the key execution risk from the transaction, with QMS contributing approximately $92 million of pro forma EBITDA in FY26 and H1 FY26 gross media revenue already up 15.2% year-on-year before the full deployment pipeline had scaled.

| Metric | FY25 | FY26 (est.) | Growth |

|---|---|---|---|

| EBITDA (pre-AASB16) | $76.7m | $86-88m | +12-15% |

| Underlying EBITDA margin | — | ~29% | — |

The presentation included a waterfall chart illustrating how growth drivers offset near-term headwinds. Auckland Transport deployment delays and softness in the large format billboard advertising market create temporary margin compression, while outperformance on the City of Sydney contract and full-year contribution from FY25 site additions support the guided range.

The underlying EBITDA margin of approximately 29% reflects the business model’s structural profitability once contract deployment costs are amortised across the lease duration.

Revenue and market outperformance

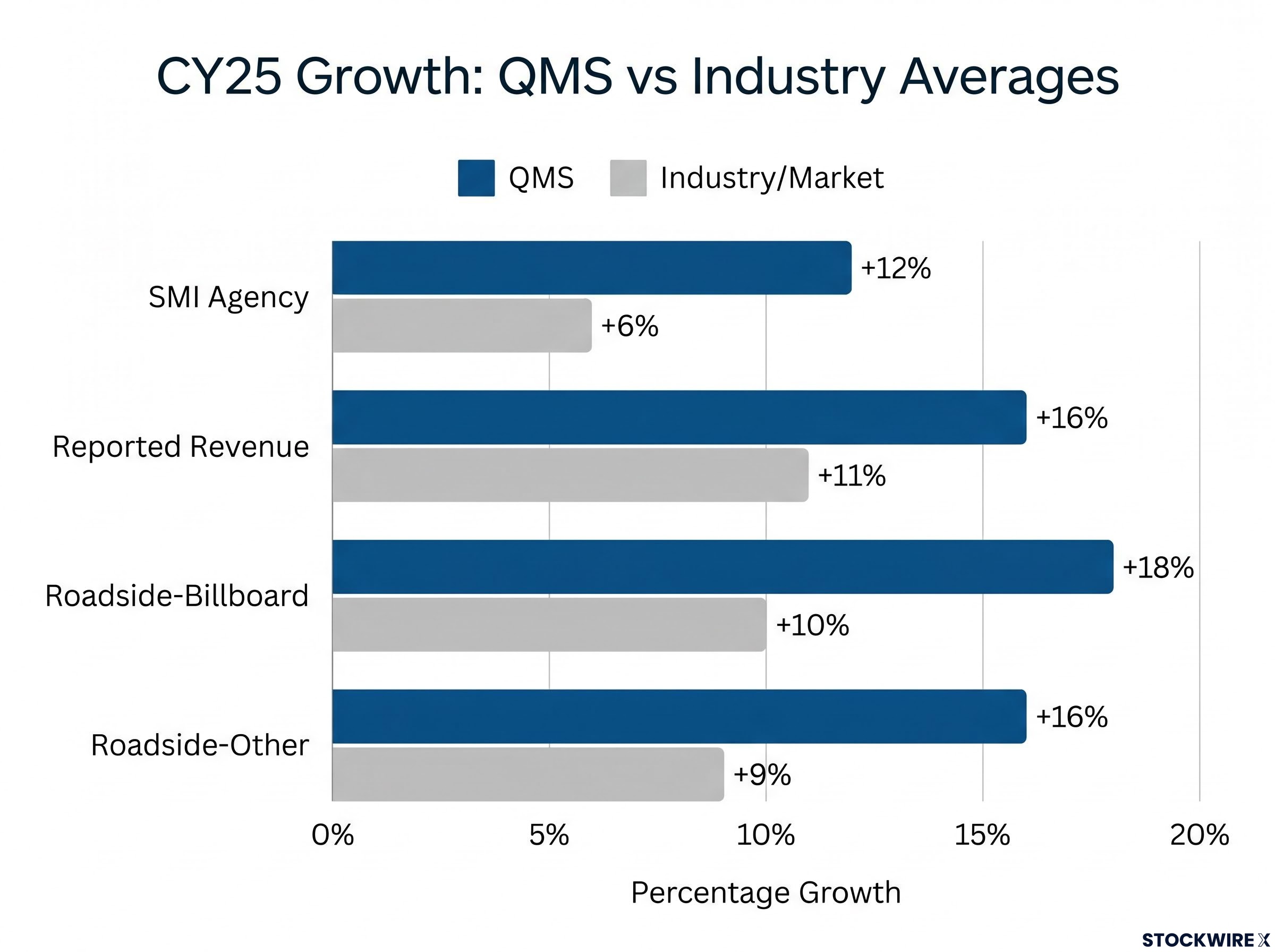

QMS continues to capture disproportionate share of industry growth across key outdoor categories. The company generated 39% of total industry revenue growth in Roadside-Other (street furniture) during CY25, well ahead of its average category market share. In Roadside-Billboards, QMS accounted for 37% of market growth, well ahead of its average category market share.

CY25 performance benchmarks:

- SMI Agency QMS growth: +12% vs industry +6%

- Reported revenue growth QMS: +16% vs industry +11%

- Roadside-Billboard QMS: +18% vs market +10%

- Roadside-Other QMS: +16% vs market +9%

This outperformance stems from QMS’ concentration in premium metro locations with higher occupancy rates, accelerated digital conversion supporting yield expansion, and strategic contract wins (City of Sydney, Auckland Transport, Transport for NSW, Vicinity Centres) that deliver above-market growth as deployment scales.

Growth drivers and synergy targets

Management outlined multiple earnings drivers extending through FY28 and beyond. Occupancy and yield improvements on existing sites provide near-term margin expansion as the network matures. Portfolio mix shifts toward higher-margin roadside billboards and street furniture support structural margin improvement. Incremental sites under existing contracts — including Auckland Transport deployments and new Australian billboards — contribute revenue growth without requiring new contract wins.

Cost synergy realisation represents a material near-term catalyst. Nine targets $20 million in annualised cost synergies by FY28, with approximately 50% expected to be realised in FY27. Key initiatives include back office consolidation (targeting completion by end FY27), technology platform integration prioritising corporate systems, procurement efficiencies as contracts expire, and redirection of Nine’s marketing spend to QMS inventory.

Synergy Timeline

“Cost synergies of ~$20m on track, with approximately half of estimated 3-year cost synergies to be realised in FY27. Consolidation of back office is in progress, targeting completion by end of FY27. Technology integration is prioritising corporate systems, with revenue platforms targeted in years 2-3.”

Premises consolidation across CY26-CY28 will further reduce property costs as overlapping lease expiries align. Beyond cost synergies, management highlighted material EBITDA upside potential from revenue synergies with Nine’s core media business, though specific targets were not quantified.

Creating an integrated media ecosystem

Nine’s strategic thesis centres on leveraging QMS to create a cross-platform advertising proposition that few Australian media companies can replicate. The integration connects streaming (Stan, 9Now), broadcast television, publishing (SMH, The Age, AFR) and outdoor inventory under unified audience data and targeting infrastructure.

The “Sofa to Street” capability combines Nine Tribes first-party data — collected from postcode-level sign-ups across digital properties — with QMS location intelligence tracking physical movement patterns. An example workflow outlined in the presentation: Nine identifies SUV Intenders based on content consumption patterns (reading SUV reviews, watching automotive programming), maps their postcodes to QMS screen locations, identifies screens indexing highest for that audience segment (e.g., Baulkham Hills, Mona Vale, Ryde), and executes coordinated campaigns across streaming, publishing and outdoor touchpoints.

This approach shifts Nine’s market position from selling individual channels to solving full-funnel marketing problems. Management emphasised AI opportunities across four domains: audience understanding through demographic and behavioural analysis, inventory optimisation via location intelligence and predictive performance modeling, dynamic content delivery adjusting creative based on real-time conditions, and business operations encompassing the rollout of Gemini across all employees, efficiency improvements, predictive maintenance for assets, and automated reporting.

“Outdoor now plays a critical role in our media plans, ticking boxes across all audiences and the full funnel.”

The enhanced Move audience measurement system, launched in March 2026, provides granular visibility into how audiences interact with every outdoor sign and campaign. This infrastructure supports joint targeting precision that leverages both digital behaviour signals and physical movement data.

The next major ASX story will hit our subscribers first

What’s next for Nine and QMS

Near-term execution priorities focus on operational integration rather than immediate revenue expansion. Back office consolidation is in progress with completion targeted by end FY27. Technology integration prioritises corporate systems before transitioning to revenue platform integration in years two and three. Procurement efficiencies will be captured as existing contracts expire, while premises consolidation is scheduled across CY26-CY28.

Management framed integration — not ownership alone — as the value unlock. The strategic positioning creates a differentiated market offer: a complete ecosystem spanning streaming, broadcast, publishing, outdoor and data infrastructure working across the full marketing funnel. This cross-platform proposition cannot be easily replicated by competitors operating in siloed media verticals.

For investors, the key execution variables over the next 12-24 months are synergy realisation velocity, technology platform integration progress, and evidence of revenue synergies materialising through joint client mandates. The long-dated QMS lease profile provides revenue stability while Nine executes the operational integration required to capture the strategic premium management assigns to the cross-platform ecosystem.

Want the Next Media Sector Breakout in Your Inbox?

Join 20,000+ investors receiving FREE breaking ASX news within minutes of release, complete with in-depth analysis. Click the “Free Alerts” button at Big News Blast to get media sector announcements and expert coverage delivered straight to your inbox the moment market-moving news breaks.