Westpac shares dropped 2.13% on 27 May 2026, the same day a Federal Court penalty landed for hardship response failures stretching back to 2017. The penalty: $26 million. The bank’s first-half profit, reported just three weeks earlier: $3.4 billion. For Australian investors holding WBC, the question is not whether the headline sounds bad. It is whether the market reaction is proportionate, or whether it conflates a backward-looking compliance failure with a forward-looking earnings story that remains intact. This analysis weighs the penalty’s actual financial materiality against Westpac’s 1H26 results, credit quality metrics, dividend position, and the broader share price trajectory, giving income and growth investors a grounded basis for their next decision on WBC.

What the $26 million penalty actually costs Westpac

The number is real. $26 million, ordered by the Federal Court on 27 May 2026, for failing to respond to over 200 online hardship requests within required timeframes between 2017 and 2023. ASIC commenced proceedings in 2023, and the matter has now resolved at the court level.

ASIC’s Federal Court proceedings against Westpac confirmed that over 200 online hardship requests went unprocessed within required timeframes across a six-year period, with Justice Timothy McEvoy ordering the $26 million civil penalty on 27 May 2026.

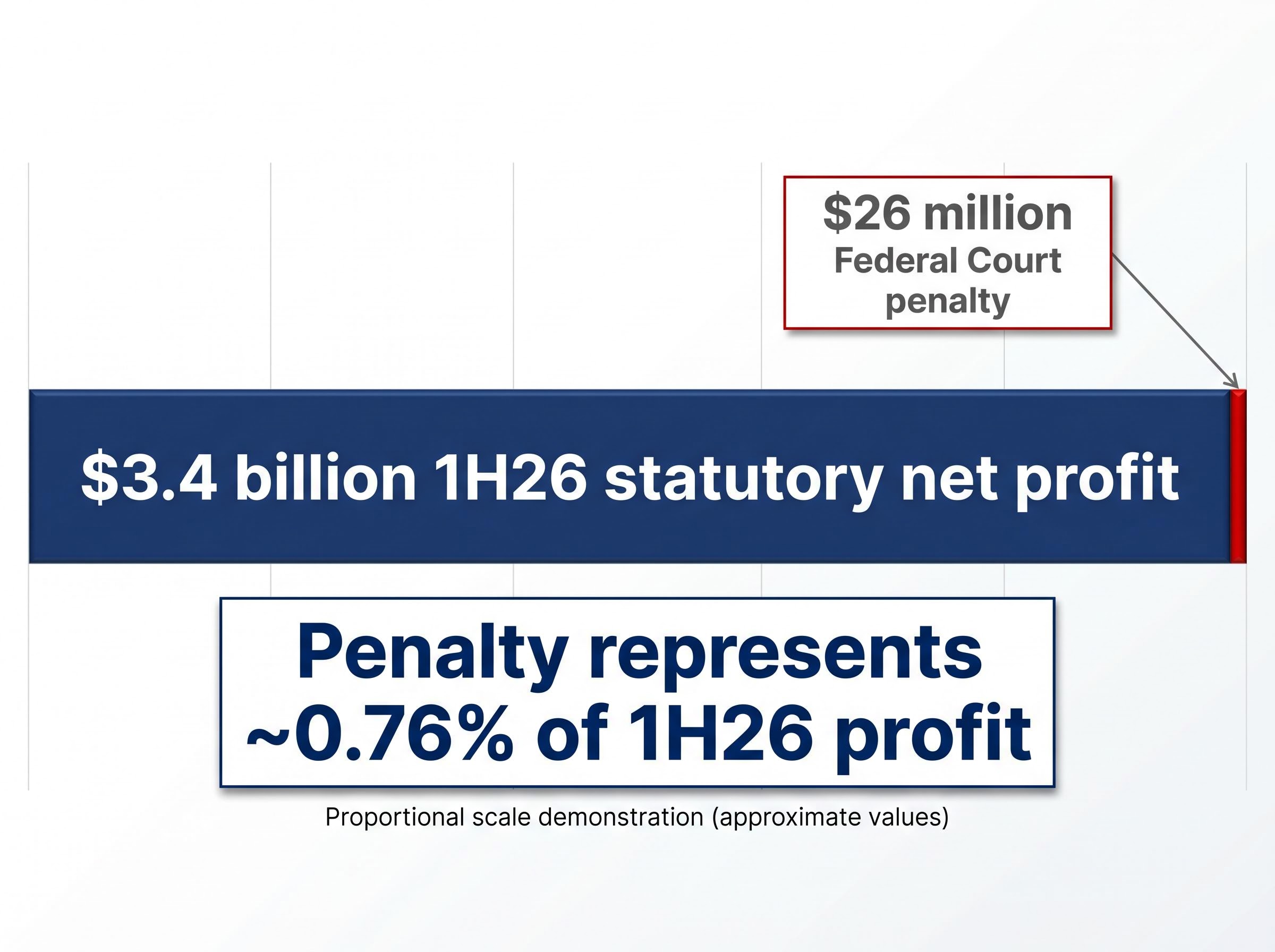

Then the context arrives. Westpac reported $3.4 billion in statutory net profit for the first half of 2026, a 3% increase on the prior corresponding period. The penalty represents approximately 0.76% of that half-year earnings figure. Remediation, including fee refunds, debt waivers, and compensation to affected customers, has been described as completed. The financial obligations beyond the penalty itself are largely crystallised.

| Metric | Figure |

|---|---|

| Federal Court penalty | $26 million |

| 1H26 statutory net profit | $3.4 billion |

| Penalty as % of 1H26 profit | ~0.76% |

| Remediation status | Described as completed |

For investors, the gap between a headline penalty and its actual earnings impact is where rational decision-making begins. A penalty representing less than 1% of half-year profit is a reputational event, not a balance sheet one.

When big ASX news breaks, our subscribers know first

Westpac’s earnings and dividend case in 2026

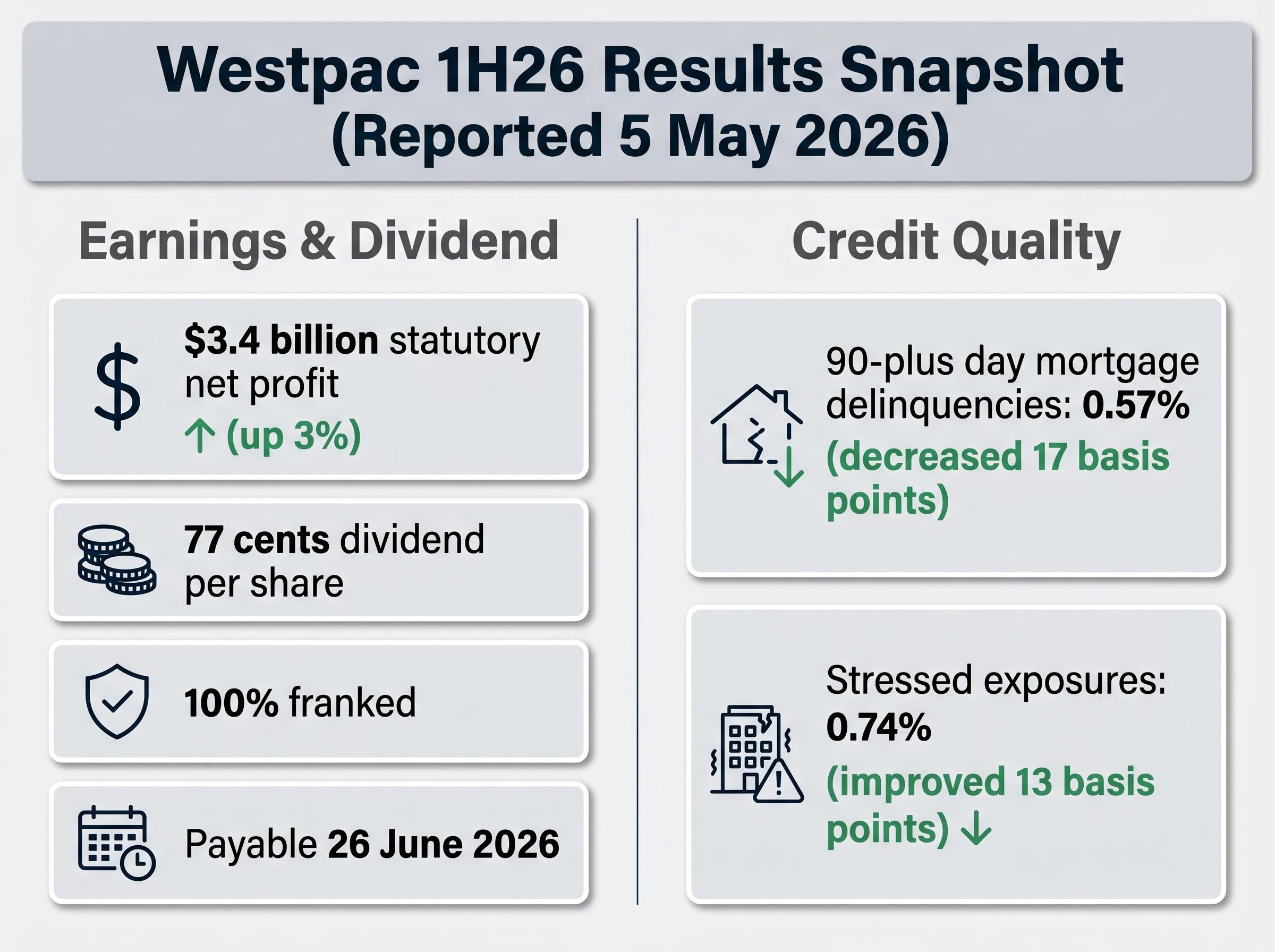

The earnings result reported on 5 May 2026 is the data point investors should anchor to, not the penalty that followed three weeks later. Westpac’s 1H26 statutory net profit of $3.4 billion, up 3% on 1H25, confirmed the bank’s core lending franchise is generating steady returns in a period of elevated household cost pressures.

$3.4 billion in first-half profit, up 3% on the prior corresponding period, reported 5 May 2026.

The interim dividend reinforces the income case. Key details for investors:

- Dividend per share: 77 cents

- Franking: 100% franked

- Payment date: 26 June 2026

- Announcement date: 5 May 2026

Full franking carries particular weight in the Australian tax context. For resident investors, particularly self-managed superannuation funds (SMSFs) and retirees, franking credits offset or eliminate the tax liability on dividend income. Superannuation funds in pension phase may receive a full refund of franking credits, effectively boosting the after-tax yield above the headline rate.

The pension-phase yield mechanics for WBC holders are more complex than the headline 77-cent dividend implies: pension-phase SMSFs can receive franking credits as a full cash refund rather than merely a tax offset, and at current share price levels following the year-to-date pullback, the effective grossed-up yield for those investors has moved materially above the face rate.

The penalty does not alter the dividend amount, the franking level, or the payment date. For income-focused investors, the 1H26 result and dividend announcement remain the operative facts.

Credit quality signals that matter more than the penalty

A regulatory penalty captures what a bank did wrong in the past. Credit quality metrics capture what the loan book is doing now. For investors weighing whether to hold or act on WBC, the second set of numbers carries more forward-looking weight.

What mortgage delinquencies tell you about a bank’s real risk

90-plus day mortgage delinquencies measure the proportion of home loans where borrowers have missed payments for at least three consecutive months. This is the standard threshold for serious arrears classification across Australian banking. A rising rate signals deteriorating borrower health and eventual pressure on provisioning, earnings, and dividends. A falling rate signals the opposite: borrowers are managing debt serviceability better than feared.

Westpac’s 1H26 results, reported 5 May 2026, showed improving credit quality across both key metrics:

- 90-plus day mortgage delinquencies: decreased 17 basis points to 0.57%

- Stressed exposures: improved 13 basis points to 0.74%

A falling delinquency rate while household cost-of-living pressures remain elevated suggests the bank’s mortgage book is performing better than the macroeconomic environment might imply. For income investors, the connection is direct: a deteriorating loan book eventually pressures dividends. An improving one supports them.

Westpac’s mortgage book concentration at 69% of total lending amplifies the significance of delinquency trends in both directions: a falling arrears rate like the 17 basis point improvement to 0.57% in 1H26 is more materially positive for Westpac than it would be for a more diversified lender, while any reversal carries proportionally greater earnings and provisioning risk.

How to read Westpac’s regulatory risk pattern as an investor

The hardship ruling did not arrive in a vacuum. Westpac has spent the years since its 2019 AUSTRAC enforcement action rebuilding its compliance infrastructure, and the failures penalised on 27 May 2026 predate much of that rebuild. Placing the penalty in its proper timeline is the first step toward a rational risk assessment.

- 2017-2023: Over 200 online hardship requests went unprocessed within required timeframes

- 2023: ASIC commenced Federal Court proceedings against Westpac

- 27 May 2026: Justice Timothy McEvoy handed down a $26 million penalty

- Remediation completed: Fee refunds, debt waivers, and compensation to affected customers described as finalised

The judicial characterisation matters for investors assessing systemic risk:

ASIC Regulatory Guide 271 on internal dispute resolution sets the enforceable standards Australian credit licensees must meet when handling customer complaints, including hardship requests, establishing the compliance framework Westpac was found to have breached across the 2017-2023 period.

The court classified Westpac’s conduct as grossly negligent rather than intentional.

That distinction carries different implications. Gross negligence in processing hardship requests points to systems and resourcing failures during a specific period, not deliberate disregard for customer welfare. It does not excuse the conduct, but it frames the risk profile differently than an intentional breach finding would.

Westpac has stated that its online hardship support systems have been upgraded and internal processes enhanced. Investors can note this, but corporate assurances of improved compliance warrant monitoring rather than acceptance at face value. The genuine test is whether new proceedings emerge in coming years.

Investors who held WBC through the 2019 AUSTRAC period understand that regulatory risk is a structural feature of major bank ownership in Australia, not an exceptional event. The relevant question is trajectory, not perfection.

Share price context: reading the 2026 chart without overreacting

The 2.13% single-day decline on 27 May 2026 is the shortest of three timeframes investors should consider.

The May share price reaction on 8 May 2026, when WBC dropped 2.2% despite reporting the same 3% profit rise, established a pattern that helps contextualise the 27 May move: a combination of ex-dividend adjustment mechanics, half-on-half earnings softness, and broker consensus targets sitting below recent trading levels all contributed to selling pressure that had little to do with the underlying earnings quality.

| Timeframe | Performance |

|---|---|

| 27 May 2026 (single day) | -2.13% |

| 2026 year-to-date | ~-7% |

| 12-month | ~+13% |

The intraday range on 27 May tells its own story. WBC traded between $35.69 and $36.46, closing at approximately $35.83 on volume of roughly 1.64 million shares. The market tested lower but did not collapse, and no evidence of panic-level volume or capitulation appeared in the session’s data.

The genuine investor question sits in the year-to-date figure. A 7% decline since the start of 2026 against a 13% gain over twelve months could indicate consolidation within a broader uptrend, or it could represent the early stages of a re-rating. Without peer-comparative valuation data, the distinction is difficult to resolve definitively.

How an investor frames that difference determines whether the day’s dip reads as noise or signal.

The next major ASX story will hit our subscribers first

The WBC investment case after 27 May: what income investors should actually weigh

The tension in the WBC holding decision is genuine but bounded. On one side: a $3.4 billion half-year profit (up 3%), a 77 cents per share fully franked dividend payable 26 June 2026, and mortgage delinquencies falling to 0.57%. On the other: a regulatory pattern that, while improving, has not yet delivered a clean slate.

Income investors vs. growth investors: different readings of the same data

For income investors, the penalty does not affect the 26 June dividend, the franking is intact, and the earnings base supports continuation at similar levels in the second half. The $26 million penalty, representing approximately 0.76% of half-year profit, does not alter the income thesis.

Income investors who want to stress-test the sustainability of dividend growth beyond the current 1H26 confirmation will find our dedicated guide to Westpac’s dividend forecast through FY28, which models the path from the confirmed FY25 payout of $1.53 per share to a projected $1.70 by FY28 and identifies the three specific risks, including UNITE programme cost overruns and mortgage margin compression, that could break that trajectory.

For growth investors, the 7% year-to-date decline is the more relevant question. Without peer-comparative valuation data, the case for near-term price recovery rests on broader sector re-rating rather than WBC-specific catalysts.

Forward-looking indicators to monitor:

- Mortgage delinquency trend at full-year results

- Dividend per share at 2H26 reporting

- Any new ASIC or APRA proceedings

- Housing credit growth as a lead indicator of lending volume

Penalty or dip? The Westpac holding decision in plain terms

The $26 million penalty is a reputational event, not a material earnings event. Investors who conflate the two risk making the wrong call on a stock that delivered $3.4 billion in first-half profit and improved its credit quality metrics in the same period.

The genuine watchlist items are specific: the 26 June dividend payment, the credit quality trend at full-year results, and the presence or absence of new regulatory proceedings. These are the variables that will determine whether WBC’s 2026 story is one of steady income generation or renewed compliance disruption.

Westpac is not the same bank it was in 2019. It is also not a bank with a clean regulatory slate. Pricing that tension accurately is the investor’s actual job.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.