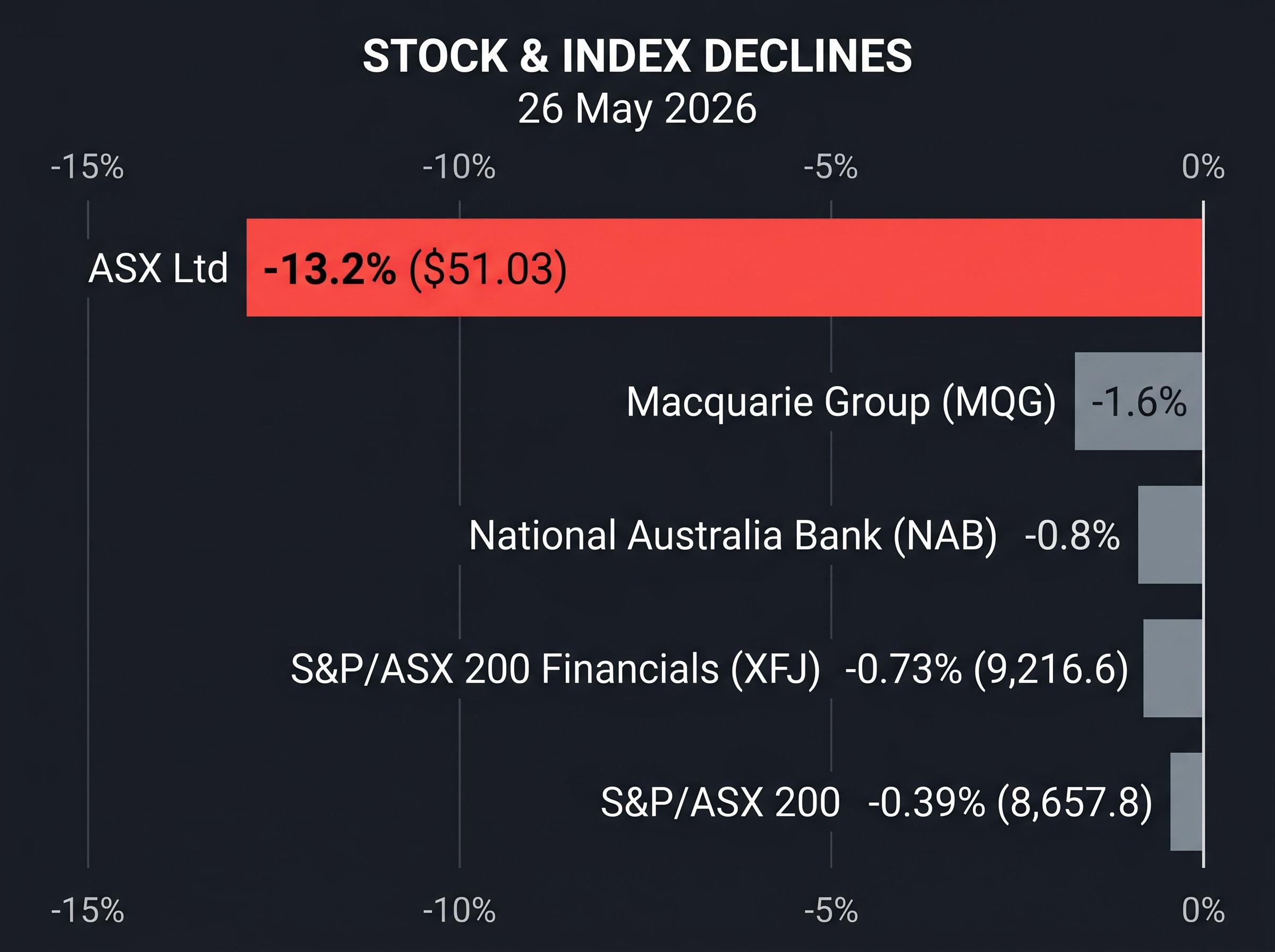

A 13.2% single-day share price collapse is not what investors expect from the company that runs Australia’s own securities exchange. On 26 May 2026, ASX Ltd disclosed FY27 total expense growth of 18-21%, an uplift driven by its CHESS replacement programme, cloud migration, and data infrastructure expansion. The announcement arrived ahead of a scheduled June investor forum, suggesting management judged the magnitude of the guidance too material to hold. The Financials sector (XFJ) fell 0.73% on the day, with ASX Ltd’s decline the dominant single-stock contribution. What follows unpacks what the guidance actually says, why the market reacted so severely, what the CHESS programme’s current status means for the cost trajectory, and how investors should think about exchange-operator cost cycles when sizing their exposure.

What ASX Ltd actually disclosed and why it shocked markets

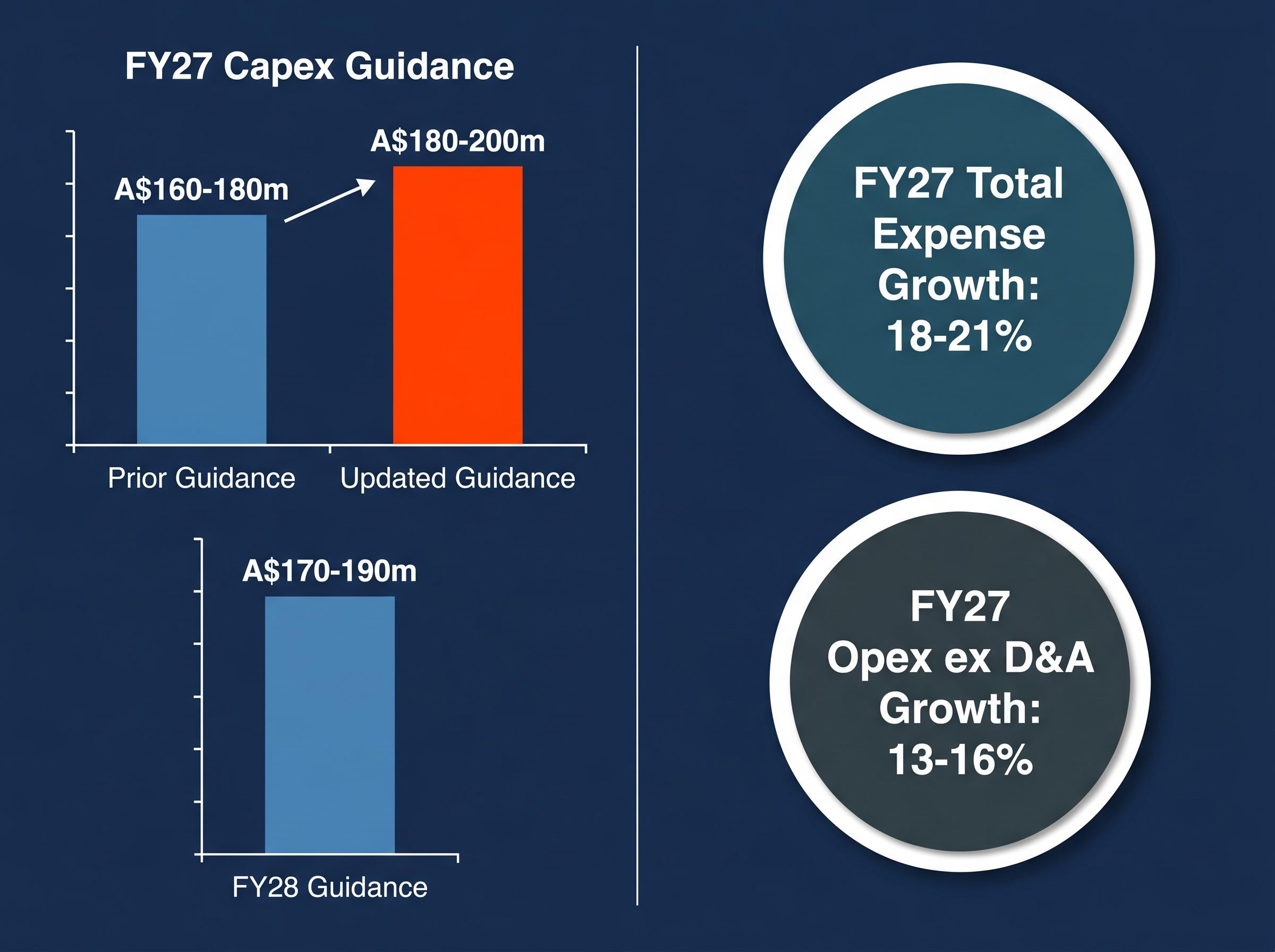

The numbers arrived bluntly. ASX Ltd guided FY27 total expense growth of 18-21% versus FY26, with operating expenses excluding depreciation and amortisation rising 13-16%. Capital expenditure guidance lifted to A$180-200 million, up from prior guidance of A$160-180 million. FY28 capex was set at A$170-190 million.

Four drivers were cited: technology modernisation tied to CHESS, the expanded Accelerate Programme, customer-growth investments, and technology cost inflation. FY26 expense and capex guidance was left unchanged, meaning the shock is entirely forward-looking and concentrated in a single fiscal year.

ASX Ltd’s share price closed at $51.03, down 13.2% on the day. The Australian Financial Review described the move as the company’s biggest single-day loss on record.

The timing carried its own signal. This guidance had been earmarked for the June 2026 Investor Forum. Bringing it forward suggests management concluded the gap between market expectations and the actual cost trajectory was too wide to leave unaddressed for another month.

| Metric | Prior Guidance | Updated FY27 Guidance |

|---|---|---|

| Total expense growth (vs FY26) | Not previously disclosed | 18-21% |

| Opex growth ex D&A (vs FY26) | Not previously disclosed | 13-16% |

| Capex FY27 | A$160-180 million | A$180-200 million |

| Capex FY28 | Not previously disclosed | A$170-190 million |

For investors who hold ASX Ltd for its perceived defensive, near-monopoly characteristics, the scale of this uplift reframes the near-term earnings profile entirely. This is a cost base being rebuilt, not trimmed.

The full FY27 guidance detail covers additional dimensions not addressed here, including the near-term dividend constraint tied to the $150 million capital accumulation requirement, the Sympli stake disposal, and year-to-date revenue momentum across all four operating divisions.

When big ASX news breaks, our subscribers know first

The CHESS programme: what is built, what remains, and what it costs

CHESS, the Clearing House Electronic Subregister System, is the infrastructure through which Australian securities are cleared and settled. Its replacement has been a multi-year programme, made more complicated by the abandonment of an earlier blockchain-based approach that failed to deliver.

CHESS settlement infrastructure underpins every equity trade on the exchange, and Release 1 going live in May 2026 marked the first major milestone in replacing a system that has processed Australian securities clearing and settlement for decades.

The programme is now progressing in two releases:

- Release 1 was confirmed complete on 5 May 2026, with the system transitioning from Hypercare Stage 1 to Hypercare Stage 2 ahead of final business-as-usual support.

- The Accelerate Programme, developed in direct response to the ASIC inquiry, is contributing to the FY27 cost profile and remains ongoing.

- Release 2, covering settlement functionality, is targeted for 2029 and represents the programme’s remaining major deliverable.

The CEO transition at ASX, announced in February 2026 and structured around the CHESS Release 1 milestone, adds a layer of leadership uncertainty to an already demanding technology and regulatory delivery schedule.

The RBA Financial Stability Standards for clearing and settlement set the compliance baseline that ASX Clear and ASX Settlement must meet as licensed facilities, establishing the supervisory framework within which CHESS Release 2 must eventually be delivered and accepted.

The FY27 capex increase from A$160-180 million to A$180-200 million was attributed in part to technology cost inflation associated with the CHESS programme. Release 2 delivery is still three years away, meaning the elevated spending profile has a long runway.

The Accelerate Programme: a regulatory cost that cannot be deferred

ASIC’s inquiry into ASX Ltd’s handling of the original CHESS replacement triggered the Accelerate Programme. The resulting costs sit outside management’s discretionary capital allocation; they are obligations imposed by the regulator.

ASIC’s inquiry into ASX governance, which concluded in April 2026 and imposed a $150 million capital charge alongside a hard 30 June 2026 deadline to reset the Accelerate Programme with both ASIC and the RBA, is the direct regulatory origin of the compulsory spending that now sits inside the FY27 cost profile.

ASIC’s statutory notices to ASX Clear and ASX Settlement required the release of a Special Report and Audit Report arising from the CHESS Programme External Review, formalising the regulatory obligations that now underpin the Accelerate Programme’s non-discretionary cost profile.

This distinction matters for how the market prices the spending. Regulatory-driven expenditure typically receives less investor credit than growth-oriented capex, because the return profile is defensive rather than expansionary. The compulsory nature of the Accelerate Programme helps explain why the market’s reaction was punitive rather than patient.

How exchange operators absorb technology cost cycles: the investor’s framework

Exchange operators share a structural economic profile: high fixed-cost bases, near-monopoly clearing and settlement revenues, and periodic large-capital technology cycles that compress margins temporarily before yielding operating leverage on the other side.

ASX Ltd is not the first exchange to face this dynamic. LSEG absorbed elevated costs during its Refinitiv integration. Nasdaq committed to a cloud-driven investment cycle. HKEX has undertaken its own technology modernisation. Direct numeric comparisons are not available in public sources, but the pattern is consistent: spend heavily, compress margins, then harvest operating leverage as the platform matures.

The investor framework for evaluating whether this kind of cycle is manageable or structurally impairing centres on three signals:

- Capex-to-revenue ratio trend: Is spending rising faster than revenue, and for how long?

- Post-cycle operating leverage evidence: Do margins recover once the programme concludes, or does the cost base reset permanently higher?

- Time-bounded versus open-ended cost growth: Is there a defined endpoint, or does the spending horizon keep extending?

Exchange operators trading at premium multiples for their monopoly characteristics face asymmetric market reactions when cost discipline falters. The premium prices in stability; elevated cost guidance reprices the near-term earnings profile rapidly.

The absence of publicly available pre-announcement EPS consensus figures makes it difficult to quantify the exact earnings surprise. The 13.2% share price reaction itself, however, is evidence that the guidance materially exceeded market expectations. Investors holding ASX Ltd for defensive yield characteristics now face a near-term earnings profile under pressure, and the investment case rests on whether post-CHESS operating leverage is credible.

The next major ASX story will hit our subscribers first

Financials sector drag and how ASX Ltd’s move compared to peers on the day

The broader Financials sector declined on 26 May 2026, but the weakness was broad and shallow. ASX Ltd was the outlier.

- ASX Ltd (ASX): -13.2% to $51.03

- National Australia Bank (NAB): -0.8%

- Macquarie Group (MQG): -1.6%

- S&P/ASX 200 Financials (XFJ): -0.73% to 9,216.6

- S&P/ASX 200: -0.39% to 8,657.8

The contrast is instructive. The major banks declined on macro sentiment. ASX Ltd declined on company-specific disclosure. These are different risk events requiring different investor responses: one is a sector headwind that rotates; the other is a repricing of a single company’s earnings trajectory.

Broker reaction: what to watch for in coming days

No publicly available post-announcement broker price target or rating changes specifically responding to the FY27 cost disclosure have been identified as of 26 May 2026. Broker research notes responding to major guidance surprises typically emerge within 24-48 hours.

Investors should monitor coverage from Macquarie, UBS, Morgan Stanley, Citi, and Ord Minnett for updated price targets and earnings revisions. EPS and dividend consensus downgrades represent the primary risk if brokers conclude the elevated cost profile is durable beyond FY27.

ASX Ltd’s cost reset is a test of the infrastructure investment thesis

The investment question now has two parts. First, whether the FY27-FY28 cost cycle proves time-bounded, with CHESS Release 2 delivery in 2029 serving as the programme’s endpoint. Second, whether post-programme operating leverage materialises in a way that restores the earnings growth profile.

The January 2026 FY26 guidance update was a precursor signal. The May 2026 disclosure represents the first formal FY27 framing, meaning further revisions remain possible as programme costs are refined.

Three forward-looking watchpoints define the path from here:

- CHESS Release 2 delivery timeline: Slippage beyond 2029 would extend the elevated cost profile and erode confidence in the programme’s manageability.

- FY28 capex execution versus guidance: The A$170-190 million range represents a modest step-down from FY27, a tentative positive signal that the spending peak may be near.

- Operating leverage evidence in FY28-FY29 results: Margin recovery after programme completion is the proof point that validates the investment case.

The FY28 capex guidance of A$170-190 million represents a modest step-down, but the distance to cost normalisation remains measured in years, not quarters.

The June 2026 Investor Forum, the originally scheduled venue for this guidance, is the next major disclosure event. Investors should watch for additional detail on cost trajectory, capex phasing, and management’s operating leverage assumptions.

For long-term holders, the question is not whether FY27 earnings are impaired. They are. The question is whether the cost programme has a credible endpoint and a recovery path on the other side.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.