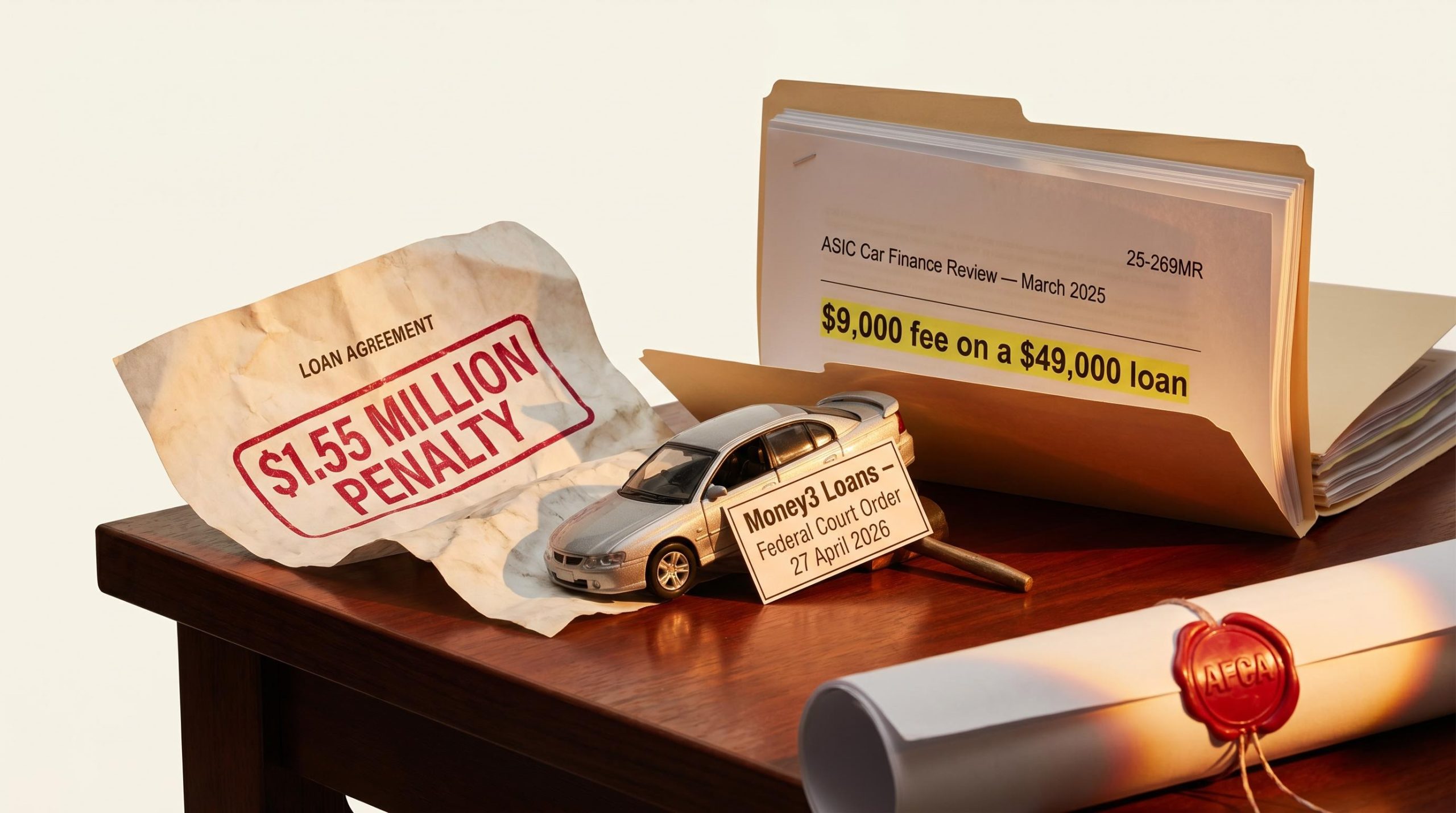

ASIC has already sent tailored action letters to car finance lenders and ordered a $1.55 million Federal Court penalty against Money3 Loans, and its full sector-wide report has not even dropped yet. The Australian Securities and Investments Commission launched its motor vehicle finance review in March 2025, published preliminary insights in November 2025, and is expected to release a comprehensive public report later in 2026. As of May 2026, that report remains outstanding, making this a critical window for consumers and industry participants to understand what is coming.

What follows is an explanation of what the ASIC car finance review covers, what the regulator has already found, why certain borrowers face disproportionate risk, and what options exist right now for Australians who believe they received an unsuitable car loan.

Why ASIC put Australia’s car finance industry under the microscope

The review did not emerge from a single headline case. It emerged from a pattern. Complaints about unaffordable car loans, excessive fees, and post-repossession debt had accumulated across ASIC’s regulatory channels, financial counselling services, and consumer advocacy bodies for years. Regional, remote, and First Nations consumers appeared disproportionately in the data. ASIC’s prior work on hardship reporting and small amount credit contracts had already flagged motor vehicle finance as a sector where lending practices lagged behind the obligations that governed them.

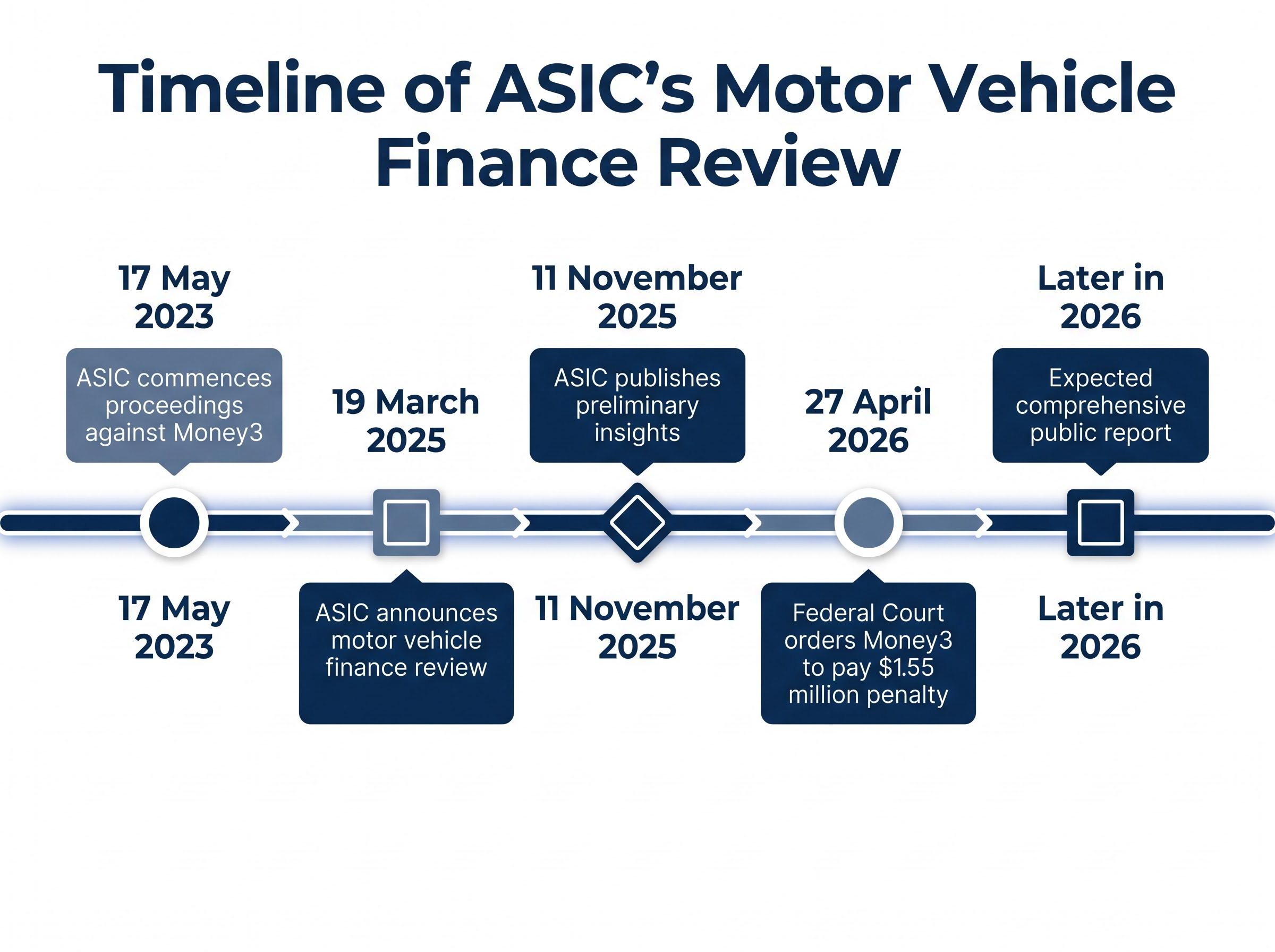

On 19 March 2025, ASIC announced it was putting car finance under the microscope. The review’s scope covers the entire customer journey, from how a loan is originated to how a default is handled:

- Compliance with responsible lending obligations by lenders, brokers, and intermediaries

- Loan defaults, hardship provisions, and dispute resolution processes

- Affordability assessments and the circumstances of early loan defaults

- Establishment fees and cost structures

- Oversight of distributors, including dealerships and brokers

- Product governance and risk frameworks

The breadth of the scope tells the story. ASIC did not isolate one practice. It targeted the full chain.

Who the review is designed to protect

The review explicitly prioritises outcomes for regional, remote, and First Nations consumers. These are the cohorts ASIC identified as disproportionately exposed to unsuitable lending.

The Indigenous Consumer Assistance Network (ICAN) has publicly supported the review, having raised car finance as a persistent issue affecting these communities. Geographic isolation and exclusion from mainstream banking create conditions where limited competition, fewer alternatives, and reliance on intermediaries concentrate harm. When lending practices are inadequate, these borrowers absorb the worst of it.

When big ASX news breaks, our subscribers know first

What the responsible lending rules actually require of car finance lenders

The legal standard that governs every car loan in Australia is the responsible lending obligations framework under the National Consumer Credit Protection Act (NCCP). These obligations do not apply exclusively to banks. They bind every lender, broker, and dealership acting as a credit intermediary.

A compliant affordability assessment follows three steps:

- Gather financial information from the applicant, including income, living expenses, and existing liabilities

- Verify that information against available evidence such as bank statements, payslips, and credit reports, rather than relying solely on what the applicant declares

- Determine suitability before issuing credit, confirming the loan will not place the borrower in substantial hardship

The Money3 Loans case illustrates what happens when these steps are not followed. Five loans issued between May 2019 and February 2021 formed the basis of ASIC’s action. In each case, bank statement data was available to the lender, but living costs were not adequately investigated before the loans were approved.

Justice McElwaine characterised the failures as “serious” and as undermining “the fundamental purpose of licensee responsible lending obligations.”

That characterisation matters. It frames the obligation not as a procedural box-ticking exercise but as a substantive duty that exists specifically to prevent harm.

What ASIC’s preliminary findings reveal about how the industry is actually operating

ASIC media release 25-269MR, published on 11 November 2025, provides the most current official picture of how car finance lenders are performing against their obligations. The release, titled “ASIC drives car finance providers to improve consumer outcomes,” identifies four failure patterns that extend well beyond any single lender.

The table below summarises each pattern and the corresponding improvement area ASIC flagged in its action letters to lenders.

| Failure Pattern | What It Looks Like in Practice | Recommended Improvement Area |

|---|---|---|

| Unaffordable loans and early defaults | Borrowers defaulting within months of loan commencement; loans that were unaffordable at origination | Risk management and affordability frameworks |

| Excessive establishment fees | Fees representing a substantial proportion of the loan principal (e.g., a reported $9,000 fee on a $49,000 loan) | Product governance and fee structures |

| Inadequate distributor oversight | Dealerships and brokers operating with insufficient training, accreditation, and auditing | Distributor training and regular audit processes |

| Hardship communication deficiencies | Borrowers in difficulty not informed of options including voluntary surrender | Hardship communication and governance frameworks |

ASIC sent tailored action letters to some lenders recommending specific improvements. Lender responses will be detailed in the full 2026 report. The release also stated explicitly that ASIC “will take enforcement action where appropriate.”

ASIC media release 25-269MR, published on 11 November 2025, details each of the four failure patterns identified across the sector and confirms that tailored action letters were sent to lenders, with full lender responses to be published in the forthcoming 2026 report.

The significance of early defaults as a lending indicator

A borrower who defaults within the first few months of a loan is telling a specific story. It is not the story of changed circumstances, a job loss six months in, or an unexpected medical bill. It is the story of a loan that was unaffordable from the day it was written.

This distinction matters for regulatory purposes. A loan that becomes unaffordable due to unforeseeable life events may not indicate a lending failure. A loan that was unaffordable at origination almost certainly does. The lender had an obligation to verify affordability before issuing credit. When early defaults cluster across a lender’s portfolio, the pattern points to systemic shortcomings in how affordability assessments were conducted.

Compounding the problem, consumers whose vehicles are repossessed frequently remain in significant debt after the repossessed vehicle is sold. The equity shortfall means the harm does not end with repossession; it compounds.

Enforcement is already moving, with more expected in 2026

The regulatory response is not prospective. It is already producing outcomes.

The most concluded action to date is the Money3 penalty. The Federal Court ordered Money3 Loans to pay $1.55 million on 27 April 2026 (ASIC media release 26-084MR). ASIC had commenced proceedings against Money3 on 17 May 2023, and the case took nearly three years to reach resolution.

ASIC media release 26-084MR confirms the Federal Court’s order and sets out the specific lending failures the court found to have occurred, including the reliance on declared expenses rather than verified bank statement data across the five loans examined.

ASIC Chair Joe Longo has acknowledged that responsible lending cases are complex but critical to pursue given the severity of harm to individuals.

The Money3 Loans penalty concluded proceedings that ASIC had commenced in May 2023, with the Federal Court ordering $1.55 million against the Solvar subsidiary on 27 April 2026; Solvar’s CEO confirmed the company had already overhauled its underwriting, complaints, and hardship practices in the years since the conduct occurred.

Beyond Money3, ASIC has ongoing proceedings against Diamond Wheels Pty Ltd, a car dealership, for alleged misconduct in finance distribution. This case signals that ASIC’s enforcement focus is expanding beyond lenders to the intermediaries who originate loans at the point of sale.

Three enforcement signals now sit in view:

Federal Court enforcement action in Australian financial regulation has scaled considerably in recent years; the $35 million penalty against Macquarie Securities Australia Limited in March 2026 for systematic short sale misreporting across more than 15 years and up to 1.5 billion transactions demonstrates the upper range of outcomes that ASIC is prepared to seek when systemic failures are established.

- Concluded penalty: Money3 ordered to pay $1.55 million for responsible lending breaches

- Ongoing proceedings: Diamond Wheels Pty Ltd facing allegations of misconduct in the distribution chain

- Prospective enforcement: ASIC’s 25-269MR release explicitly flagging that enforcement action will follow where misconduct is identified

The Australian Automotive Dealer Association (AADA) has confirmed that misconduct in used car finance is a key ASIC priority for 2025-2026. The tailored action letters sent to lenders in late 2025 are not advisory suggestions. They are the precursor. Lenders who fail to demonstrate substantive improvement face the prospect of being the next enforcement target when the full report lands.

What Australians who may have received an unsuitable car loan can do now

Waiting for the 2026 report does not protect a borrower who is currently in financial difficulty. The complaints and redress pathway exists under current frameworks, and it follows a logical sequence:

- Lodge an internal complaint with the lender, setting out why the loan may have been unsuitable (for example, that the lender did not adequately assess affordability before approving the credit)

- Allow 30 days for the lender to respond

- Escalate to the Australian Financial Complaints Authority (AFCA) if the complaint is unresolved or the response is unsatisfactory; AFCA has jurisdiction to order remediation, fee waivers, or loan restructuring in cases of responsible lending breaches

- Seek free financial counselling in parallel if experiencing hardship, as counsellors can assist with both the complaint process and broader debt management

The key question in any complaint is whether the lender conducted an adequate affordability assessment before issuing the loan. If bank statements, payslips, or credit reports were available but living costs were not properly investigated, that may constitute a responsible lending breach.

Three free support resources are available:

- AFCA (Australian Financial Complaints Authority): www.afca.org.au

- National Debt Helpline: 1800 007 007, free and confidential

- Mob Strong Debt Helpline: specifically designed for First Nations consumers

The Moneysmart website also provides educational resources for understanding loan products and debt management options.

The next major ASX story will hit our subscribers first

What the 2026 full report is expected to address, and how to stay informed

ASIC’s full report has been anticipated throughout 2026 and, as of 6 May 2026, has not been released. Based on the review’s stated scope and the preliminary findings already published, the report is expected to cover:

- Lender responses to ASIC’s tailored action letters and whether improvements have been made

- Detailed findings on distributor oversight failures across the sector

- Product governance outcomes, including fee structures and their suitability for target consumer markets

- Enforcement decisions arising from the review’s findings

The AADA has confirmed that detailed findings will be published in 2026. Lender responses to the action letters will be a central element, making the report a consequential accountability document for the industry.

For consumers and industry participants seeking to monitor developments, asic.gov.au is the authoritative source for the report’s release and any associated enforcement actions. The Australian Treasury’s consultation portal at treasury.gov.au is the recommended monitoring point for any NCCP amendments or targeted consultations that may follow.

The review is a checkpoint, not a conclusion

ASIC’s motor vehicle finance review represents a structural accountability moment for an industry where the gap between legal obligations and observed practice has been wide and persistent. Three things are clear from the evidence available so far.

The responsible lending obligations under the NCCP already require lenders to verify affordability before issuing credit. The preliminary findings published in November 2025 signal systemic failures in how those obligations are being met, from unaffordable loans and excessive fees to inadequate distributor oversight. And the complaints and redress pathways, through AFCA, the National Debt Helpline, and Mob Strong, exist right now for borrowers who believe their loan should never have been approved.

The full 2026 report will test whether the lenders who received action letters have substantively reformed their practices. Its credibility will rest on whether enforcement follows the findings.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.