Nvidia Set to Reveal First Windows PC Processors at Computex

1 hr ago

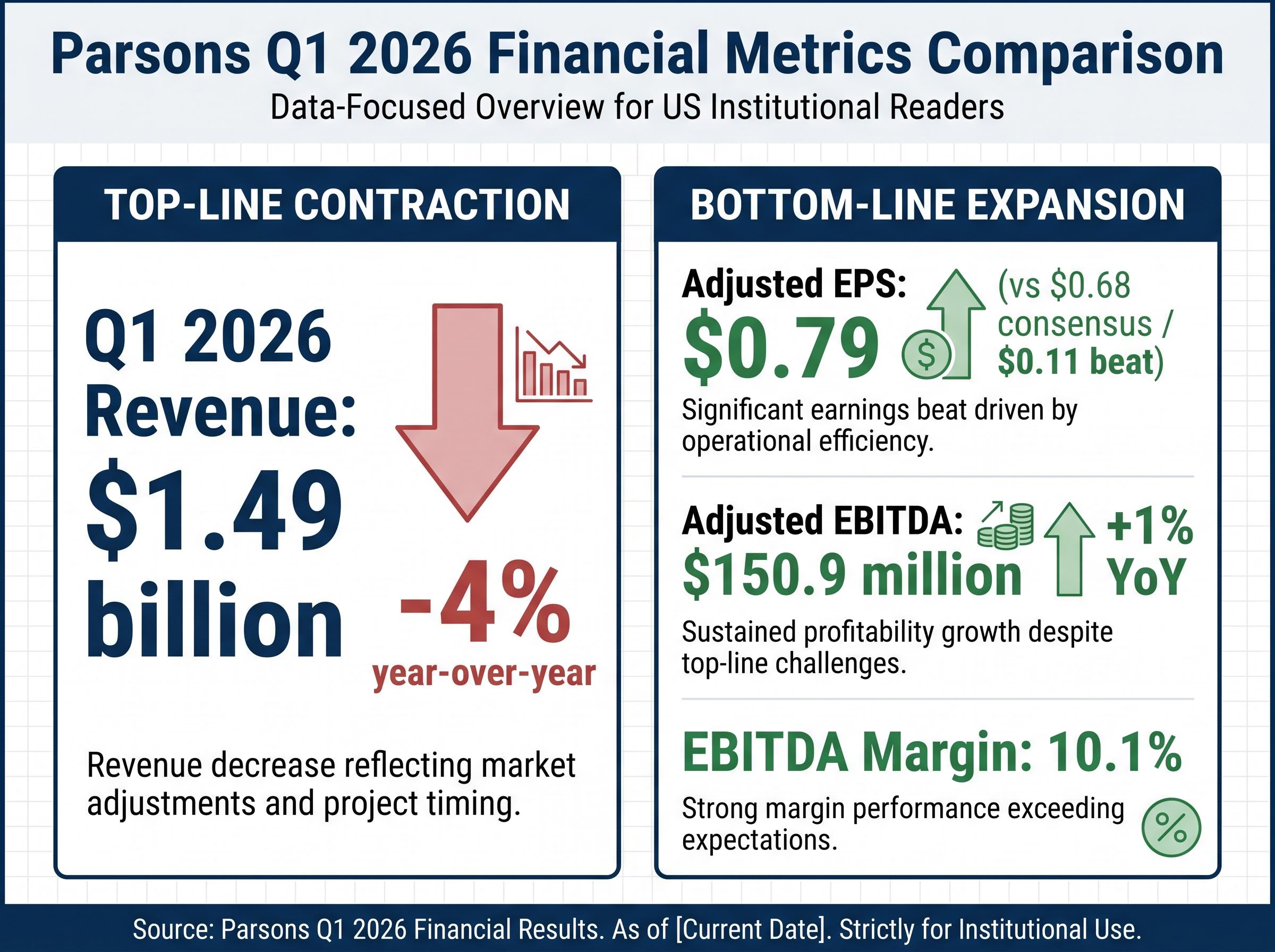

Parsons Corporation released its Q1 2026 financial results today, presenting a central paradox for the US defence sector. The latest Parsons earnings report details a decisive $0.11 earnings per share beat, achieved despite a 4% drop in top-line sales. The contractor successfully expanded profit margins while managing a temporary contraction in revenue volume.

This performance arrives amid shifting priorities in the broader US defence environment. Market participants increasingly demand operational efficiency and capital discipline rather than solely rewarding sheer growth. Parsons experienced significant pre-earnings stock volatility leading up to this release, facing an estimated 16.12% monthly decline before a notable 3.13% rise on April 24.

The mechanics behind this margin expansion reveal how disciplined cost management and a massive project backlog can satisfy Wall Street expectations even when headline revenue shrinks. Analysis of the underlying segments demonstrates that operational health relies on contract mix and execution rather than unadjusted sales volume.

The first quarter presented an immediate tension between shrinking headline revenue and expanding operational margins. Parsons reported $1.49 billion in Q1 2026 revenue, representing a 4% year-over-year decline that initially suggested a slowdown in procurement. Yet the company delivered an Adjusted EPS of $0.79, comfortably beating the FactSet consensus estimate of $0.68.

Management disclosures within the Parsons official first quarter results explicitly link this temporary billing dip to the strategic rollout of specific federal programmes rather than a structural loss of market share.

This divergence highlights a clear victory of operational efficiency over sheer sales volume. Generating higher earnings on lower sales requires aggressive cost controls and a favourable shift in the margin profile of active contracts. Adjusted EBITDA reached a record $150.9 million, increasing 1% year-over-year and expanding the margin to 10.1%.

The bottom line did see net income drop, but capital management metrics improved substantially. First-quarter operational cash utilisation tightened, a marked improvement from the prior year. This reduction in cash burn during a period of lower total billing indicates strict internal financial discipline.

This section of the balance sheet demonstrates to investors that revenue growth is not the sole driver of profitability. Strong execution can protect the bottom line, generate cash, and satisfy institutional expectations during temporary sales dips.

| Financial Metric | Q1 2026 Actual | Wall Street Consensus | Year-Over-Year Change |

|---|---|---|---|

| Total Revenue | $1.49 billion | Higher projected volume | -4% |

| Adjusted EPS | $0.79 | $0.68 | Beat consensus by $0.11 |

| Adjusted EBITDA | $150.9 million | Margin expansion expected | +1% |

| EBITDA Margin | 10.1% | N/A | Expanded margin profile |

To understand the actual operational momentum of defence stocks, investors must differentiate between headline revenue declines and true organic growth. A single confidential agreement can distort the apparent health of a massive contracting firm, creating false negative signals. The mechanics of government contracting often involve highly concentrated, short-term project bursts that skew quarterly comparisons.

This concentration risk is equally prevalent in international defense procurement, where securing initial multi-million dollar test contracts can temporarily distort quarterly revenue while laying the necessary groundwork for substantial future production runs.

Within the Federal Solutions segment, the roll-off of a specific classified contract masked otherwise solid operational expansion. When analysts exclude the impact of this single confidential agreement, the underlying business demonstrates an impressive 8% organic growth rate. This metric captures the true velocity of the recurring project base, free from the volatility of one-off specialised deployments.

Other core divisions confirm this upward trajectory, insulating the firm against single-contract dependency. The Critical Infrastructure segment provided an organic boost during the quarter, indicating steady demand for civil and commercial engineering services.

Removing the classified variable reveals a completely different growth profile for the quarter.

This mechanism explains why sophisticated investors look past misleading headline figures to evaluate structural business velocity.

The Classified Impact Headline numbers frequently fail to tell the whole story in the defence sector. The completion or transition of single, highly classified federal agreements can temporarily depress overall top-line revenue without degrading core business operations or forward-looking project pipelines.

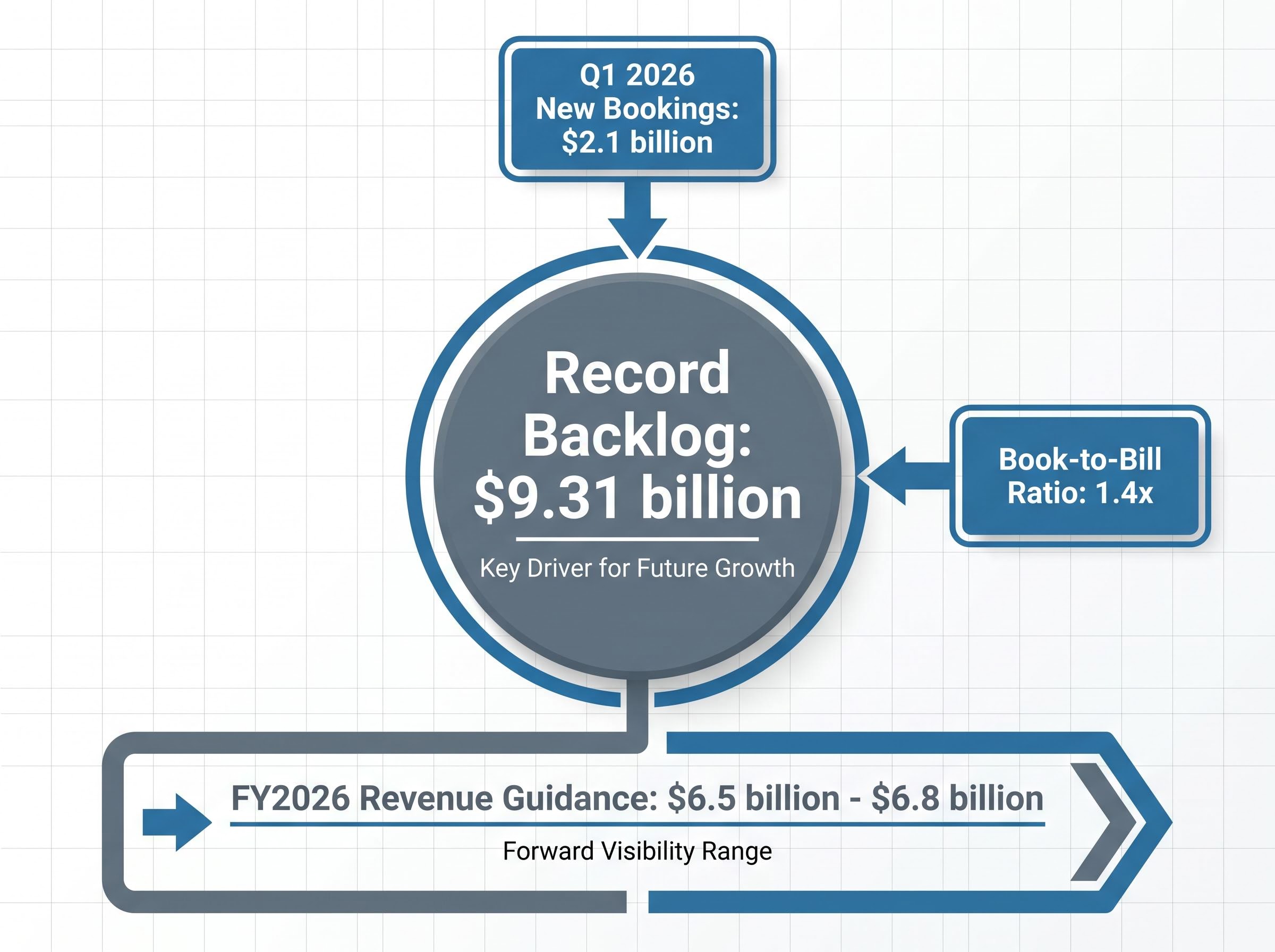

The focus now shifts from past quarterly performance to future revenue visibility. Parsons generated $2.1 billion in new bookings during Q1 2026, achieving a highly favourable 1.4x book-to-bill ratio. This multiple signals that the company is securing new work significantly faster than it is billing current projects, replenishing the pipeline and securing long-term earning potential.

This accelerated booking activity drove the total project pipeline to an unprecedented $9.31 billion record backlog. Within this figure, funded commitments hit a public-company peak, representing capital that the federal government has already appropriated and assigned. These forward-looking metrics provided management with the confidence to maintain full-year FY2026 revenue guidance between $6.5 billion and $6.8 billion.

Strategic awards like the official MDA SHIELD contract announcement validate this optimistic guidance, demonstrating that critical national security infrastructure projects continue to receive robust federal funding allocations.

The structural foundation remains entirely intact despite the current top-line noise.

The company is actively supplementing this organic pipeline with the targeted $340 million to $349.5 million acquisition of Altamira. This strategic purchase operates as an accelerator for the Federal Solutions segment, bringing specialised data analytics and advanced engineering capabilities into the existing portfolio.

A $47 million classified contract extension for US Government support awarded in March 2026. A potential $1.51 billion missile defence contract from the Missile Defense Agency secured in late 2025. A $30 million contract from the US Space Development Agency contributing to sustained momentum. The strategic Altamira acquisition, which structurally supplements the broader record backlog.

Major analysts routinely look past headline misses when profitability fundamentals hold firm, and the institutional response to this report reflects that pragmatism. The broad institutional sentiment leading into and immediately following the April 2026 report remains largely positive. Wall Street maintains a firm OUTPERFORM consensus on the stock, rewarding the company for its efficient cash management despite the top-line contraction.

Prior to the release, the stock closed at $51.66 on April 28, capping a period of significant directional volatility. Institutional capital appears to be recalibrating, pricing in the core business strength rather than the temporary revenue dip.

Valuation platforms and fundamental analysis systems strongly support this optimistic positioning. Data from GuruFocus assigns the contractor a profitability score of 8 out of 10 and a growth score of 9 out of 10. These high-tier metrics quantify exactly why institutional analysts prefer structural margin expansion over low-margin revenue volume.

Consensus price targets show some variance but reflect clear upside potential across major banking institutions. The median price target sits around $72.00, with high estimates reaching up to $78.67. Citigroup recently adjusted its target to $70.00, indicating that even conservative institutional models foresee significant value based on the underlying profitability indicators and the massive backlog.

For investors wanting to build a robust portfolio in this sector, our deep-dive into defense contractor investing breaks down how to systematically evaluate pipeline visibility, book-to-bill momentum, and margin stability across both mid-tier firms and industry giants.

Margin expansion and disciplined cash management can successfully offset top-line revenue challenges in the government services sector. The ability of Parsons to manage the roll-off of a major classified contract while generating record EBITDA indicates strong corporate agility. The firm absorbed a direct hit to its Federal Solutions revenue base while protecting its bottom-line profitability.

The two most important takeaways from this reporting period are the 10.1% peak margin and the $9.31 billion backlog. These factors will dictate the trajectory of the firm for the remainder of 2026, lowering the perceived investment risk of the current revenue dip. When management maintains a $6.8 billion upper-end revenue guidance despite a weak first quarter, they rely heavily on that funded backlog to accelerate billing in the second half of the year.

The true value of defense contractor backlogs depends heavily on the distinction between funded obligations that guarantee immediate work and unfunded commitments that require future government appropriations.

Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors. These forward-looking statements rely on continued federal appropriations and uninterrupted contract execution.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Parsons Corporation's Q1 2026 earnings report showed an Adjusted EPS of $0.79, beating the $0.68 consensus, despite a 4% year-over-year revenue decline to $1.49 billion. This performance highlighted expanded profit margins and operational efficiency.

Parsons beat EPS estimates by successfully expanding profit margins through disciplined cost management and a favorable shift in contract mix. The company achieved a record Adjusted EBITDA of $150.9 million and a 10.1% margin, offsetting the temporary revenue contraction.

Parsons achieved a 1.4x book-to-bill ratio in Q1 2026, securing $2.1 billion in new bookings, which indicates they are winning new work faster than billing existing projects. This led to a record $9.31 billion project backlog, securing long-term revenue visibility.

Parsons' Q1 2026 revenue decline was primarily linked to the strategic roll-off of a specific classified federal program. Excluding this single contract, the underlying Federal Solutions segment demonstrated an 8% organic growth rate.