TSMC Shares Fall 3% Despite Record Quarter on Supply Fears

Key Takeaways

- TSMC posted record Q1 2026 profit with revenue up 35% to NT$1.134 trillion, driven by surging AI chip demand from Nvidia, Apple, and AMD.

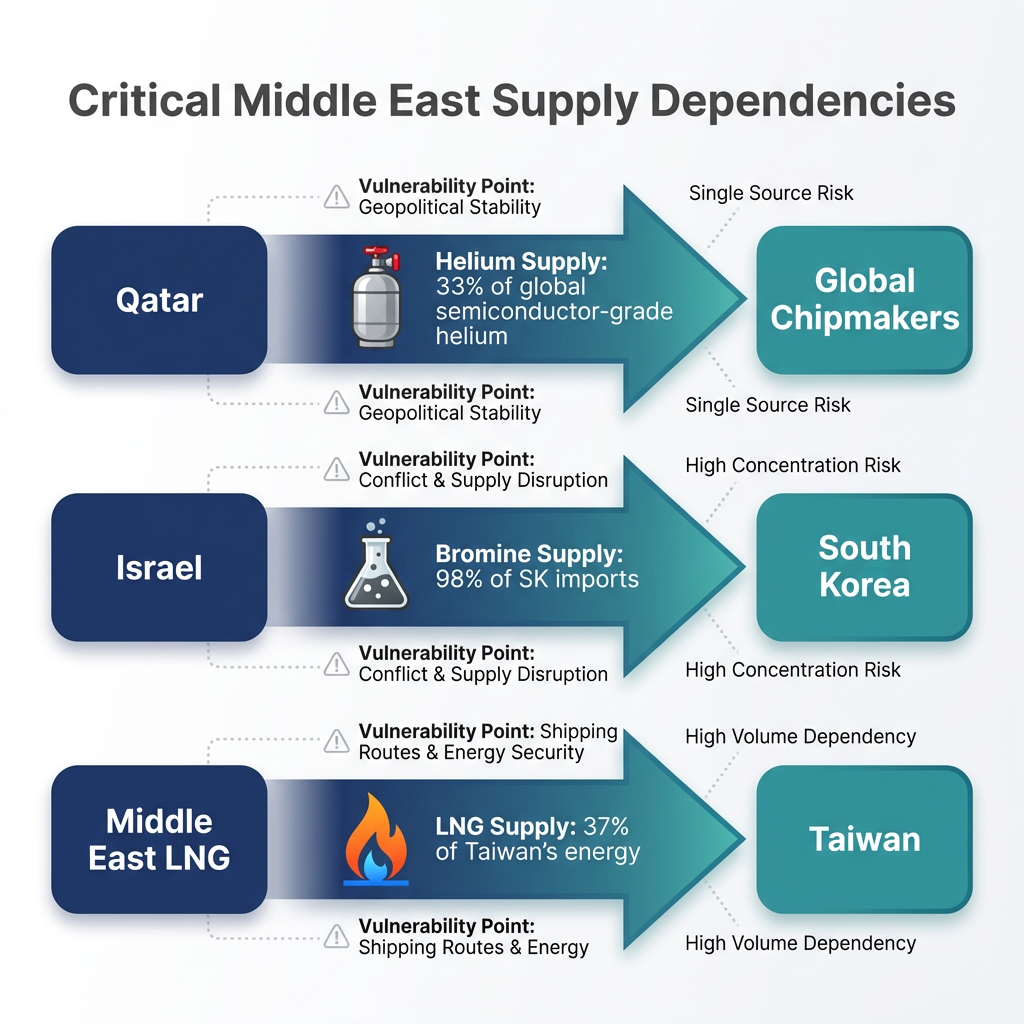

- The TSMC supply chain disruption risk centres on Qatar's Ras Laffan helium facility remaining offline, doubling global helium prices and removing approximately one-third of semiconductor-grade supply.

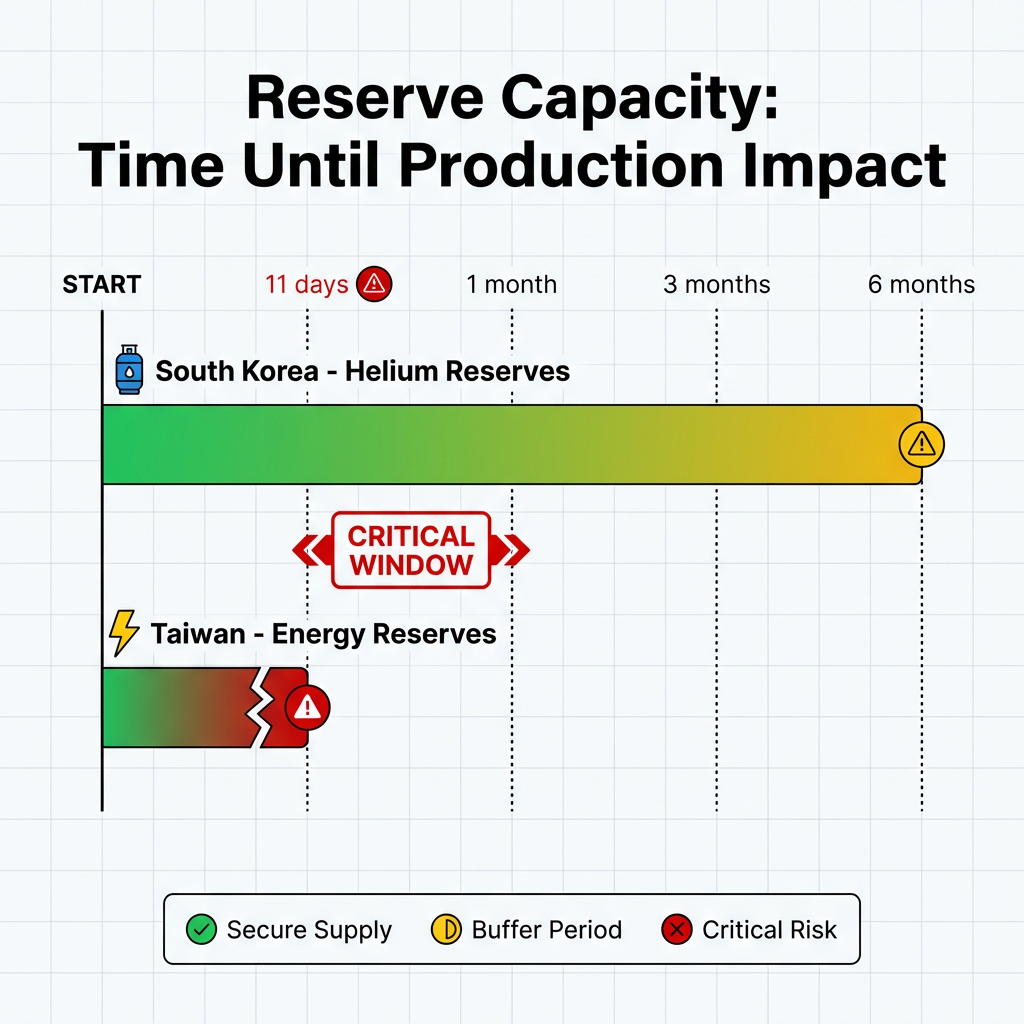

- Taiwan holds only 11 days of energy reserves compared to South Korea's 6 months of helium reserves, creating vastly different vulnerability timelines across the industry.

- No major chipmaker has reported production shutdowns as of mid-April 2026, but analysts warn that disruptions extending into weeks or months would pose severe risks to the 51% of global semiconductors produced across Taiwan, Japan, and South Korea.

- TSMC shares declined 2.4% in Taipei and 3.1% on the NYSE despite strong results, reflecting investor concern over supply chain vulnerabilities that could pressure longer-term profitability.

Taiwan Semiconductor Manufacturing Company (TSMC) reported record first-quarter profit on 16 April, with revenue surging 35% to NT$1.134 trillion driven by unprecedented demand for artificial intelligence chips. However, the world’s largest chipmaker warned that longer-term profitability could face pressure if Middle East disruptions continue threatening critical material supplies. Shares declined 2.4% in Taipei and 3.1% on the NYSE despite the strong results, as investors weighed supply chain vulnerabilities against robust AI-driven growth.

The company stated that helium, hydrogen, and energy supplies remain secure in the near term with no immediate production impacts. Yet TSMC cautioned that extended disruptions from the ongoing Middle East conflict present material risks to operations, highlighting the tension between current stability and emerging supply chain pressures.

Why Semiconductor Manufacturing Depends on Middle East Supplies

Semiconductor production relies on specialised materials and energy sources concentrated in the Middle East, creating dependencies that extend thousands of miles from manufacturing facilities. Helium plays a critical role in chip cooling and lithography processes, the advanced techniques used to etch microscopic circuits onto silicon wafers. Qatar’s Ras Laffan facility, which produced nearly one-third of global semiconductor-grade helium before Iranian strikes halted operations in early March, represents a key supply point for the industry.

According to U.S. Geological Survey helium production data, Qatar’s Ras Laffan facility accounted for approximately one-third of semiconductor-grade helium globally before operations were disrupted, confirming the country’s position as the world’s second-largest helium producer.

Three critical dependencies connect Middle East stability to global chip supply:

- Helium from Qatar: The Ras Laffan facility remains offline following strikes, removing approximately 33% of semiconductor-grade helium from global markets

- Bromine from Israel: South Korea imports 98% of its bromine needs from Israel for semiconductor etching processes, creating concentrated supply risk

- Energy from Middle East LNG: Taiwan imports 97% of its energy with 37% sourced from Middle East liquefied natural gas, whilst maintaining only 11 days of reserves

These material and energy flows explain why regional conflict disrupts chip manufacturing despite geographic distance from production facilities.

When big ASX news breaks, our subscribers know first

Current Disruption Status: Prices Doubled, Production Intact

Global helium prices have doubled since the conflict began in early March, creating significant cost pressures across semiconductor manufacturing. The Strait of Hormuz remains closed since 4 March despite a 7 April ceasefire between the United States, Iran, and Israel, blocking key shipping routes for materials and energy.

TSMC has secured alternative suppliers for immediate material needs, providing near-term supply security. SK Hynix reports adequate helium inventory for medium-term operations with no financial impacts to date, citing diversified supply chains. No major chipmaker has reported production shutdowns as of mid-April 2026, indicating that existing inventories are providing an effective buffer against the disruptions.

The Timeline Risk: Weeks Matter More Than Days

Analysts including Capital Economics’ Neil Shearing assess that current inventories can sustain short-term disruptions, but disruptions extending into weeks or months would emerge as significant problems for semiconductor production. The critical variable is time rather than immediate impact, with buffer periods varying substantially across materials and regions.

> South Korea maintains 6 months of helium reserves, whilst Taiwan holds only 11 days of energy reserves, creating vastly different vulnerability timelines across the supply chain.

If significant disruptions materialise, full production restarts could require weeks to months, compounding the initial supply impact. The consensus view frames this as a time-sensitive risk where current stability depends on conflict resolution within specific buffer periods.

Broader Industry Exposure: 51% of Global Chips at Risk

Taiwan, Japan, and South Korea collectively produce 51% of global semiconductors, and all three regions rely heavily on Middle East LNG for the energy-intensive processes required in chip manufacturing. This geographic concentration creates systemic vulnerability extending beyond individual company supply chains to affect the broader technology sector.

Taiwan’s heavy reliance on Middle East LNG highlights the vulnerability created by energy-intensive manufacturing processes, where fabrication plants can consume as much electricity as small cities. This dependency has accelerated innovations in energy-efficient chip design to reduce both operational costs and supply chain risks.

Georgetown CSET research on semiconductor supply chain vulnerabilities identifies East Asian production concentration as creating systemic risk, where shared dependencies on common inputs mean disruptions affect multiple manufacturers simultaneously rather than creating competitive advantages for individual firms.

SK Hynix reports no current financial impacts due to diversified supply chains, yet faces the same 6-month helium reserve constraint affecting South Korean industry. Samsung and Intel Foundry have not issued specific statements regarding Middle East supply chain impacts. The shared dependencies across Asian chipmakers mean disruptions would affect multiple manufacturers simultaneously rather than creating competitive advantages.

The South Korean semiconductor industry faces identical helium supply constraints, with companies exploring alternative business models like licensing partnerships that could reduce dependency on traditional high-volume manufacturing approaches.

Market Response: AI Demand Outweighs Geopolitical Fears—For Now

TSMC shares recovered to record highs following the initial conflict-driven declines, with artificial intelligence chip demand from Nvidia, Apple, and AMD driving exceptional first-quarter results. Prospects of a United States-Iran peace deal potentially reopening the Strait of Hormuz have supported market optimism, outweighing supply chain concerns in current valuations.

The exceptional demand from AI customers reflects the broader AI investment landscape and sustainability questions, where semiconductor capacity remains the critical bottleneck for deploying advanced models even as concerns grow about return on investment.

The strong results came after market sentiment preceding TSMC’s Q1 2026 earnings reflected optimism about AI chip demand despite uncertainty about Middle East supply chain pressures.

CEO C.C. Wei addressed analyst concerns about customer diversification during the 16 April earnings call, stating that establishing independent semiconductor manufacturing at TSMC’s scale would require at least three years alongside heavy capital spending. Major customers have not announced diversification initiatives, suggesting continued confidence in TSMC’s supply chain management and competitive positioning.

The next major ASX story will hit our subscribers first

What Comes Next: Key Variables to Watch

Four critical factors will determine whether current supply stability holds or gives way to production disruptions:

- Strait of Hormuz reopening status: The waterway remains closed since 4 March, blocking material and energy shipments despite the 7 April ceasefire

- Qatar Ras Laffan facility restart: No updates on production resumption have been reported since 16 April, leaving helium supply timeline uncertain

- United States-Iran peace negotiations: Progress beyond the initial ceasefire will determine conflict duration and regional stability

- Taiwan LNG diversification: Efforts to shift energy imports towards United States suppliers could reduce Middle East dependency over time

These variables represent the difference between manageable short-term pressures and extended disruptions that would test reserve capacities across the industry.

Frequently Asked Questions

Has TSMC experienced any production disruptions from the Middle East conflict?

As of 16 April 2026, TSMC reports no immediate production impacts. The company has secured alternative suppliers for critical materials including helium and hydrogen in the near term. However, TSMC cautioned that longer-term profitability could be affected if disruptions persist.

Why does the Middle East conflict affect semiconductor manufacturing?

Chip manufacturing depends on specialised materials and energy from the Middle East region. Qatar’s Ras Laffan facility, halted by Iranian strikes, produced nearly one-third of global semiconductor-grade helium. Taiwan also imports 37% of its LNG from the region with only 11 days of energy reserves.

How long can chipmakers sustain production without Middle East supplies?

Timelines vary by material and region. South Korea maintains 6 months of helium reserves, whilst Taiwan has only 11 days of energy reserves. Analysts indicate short-term disruptions are manageable through existing inventories, but extended conflicts lasting weeks or months would create severe production problems.

Are TSMC’s competitors affected by the same supply chain risks?

Yes, the vulnerability is industry-wide. Taiwan, Japan, and South Korea produce 51% of global semiconductors and share similar dependencies on Middle East materials and energy. SK Hynix reports no current impacts but faces the same reserve constraints as other Asian chipmakers.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

What is the TSMC supply chain disruption risk from the Middle East conflict?

TSMC's supply chain faces risks from disrupted helium supplies out of Qatar's Ras Laffan facility, bromine from Israel, and LNG energy imports, all of which are critical inputs to semiconductor manufacturing. While no production shutdowns have occurred as of mid-April 2026, prolonged disruptions lasting weeks or months could pressure operations and profitability.

Has TSMC reported any production shutdowns due to Middle East supply disruptions?

No, as of 16 April 2026, TSMC has secured alternative suppliers and reports no immediate production impacts, though the company cautioned that longer-term profitability could be affected if disruptions persist beyond existing inventory buffers.

How long can semiconductor manufacturers sustain operations without Middle East supplies?

Reserve timelines vary significantly — South Korea holds approximately 6 months of helium reserves, while Taiwan has only 11 days of energy reserves, meaning Taiwan-based manufacturers like TSMC face a much tighter window before energy disruptions become critical.

Why does the Middle East conflict affect chip manufacturing so far away?

Semiconductor fabrication relies on specialised materials concentrated in the Middle East, including semiconductor-grade helium from Qatar's Ras Laffan facility and LNG energy supplies, with Taiwan importing 37% of its liquefied natural gas from the region to power its energy-intensive chip plants.

Which chipmakers are most exposed to Middle East supply chain risks?

Taiwan, Japan, and South Korea collectively produce 51% of global semiconductors and all share heavy reliance on Middle East LNG and materials, meaning TSMC, SK Hynix, and Samsung face simultaneous exposure rather than any single firm bearing concentrated risk.