Investment Products Capture 40% of India Gold Demand in 2025

Key Takeaways

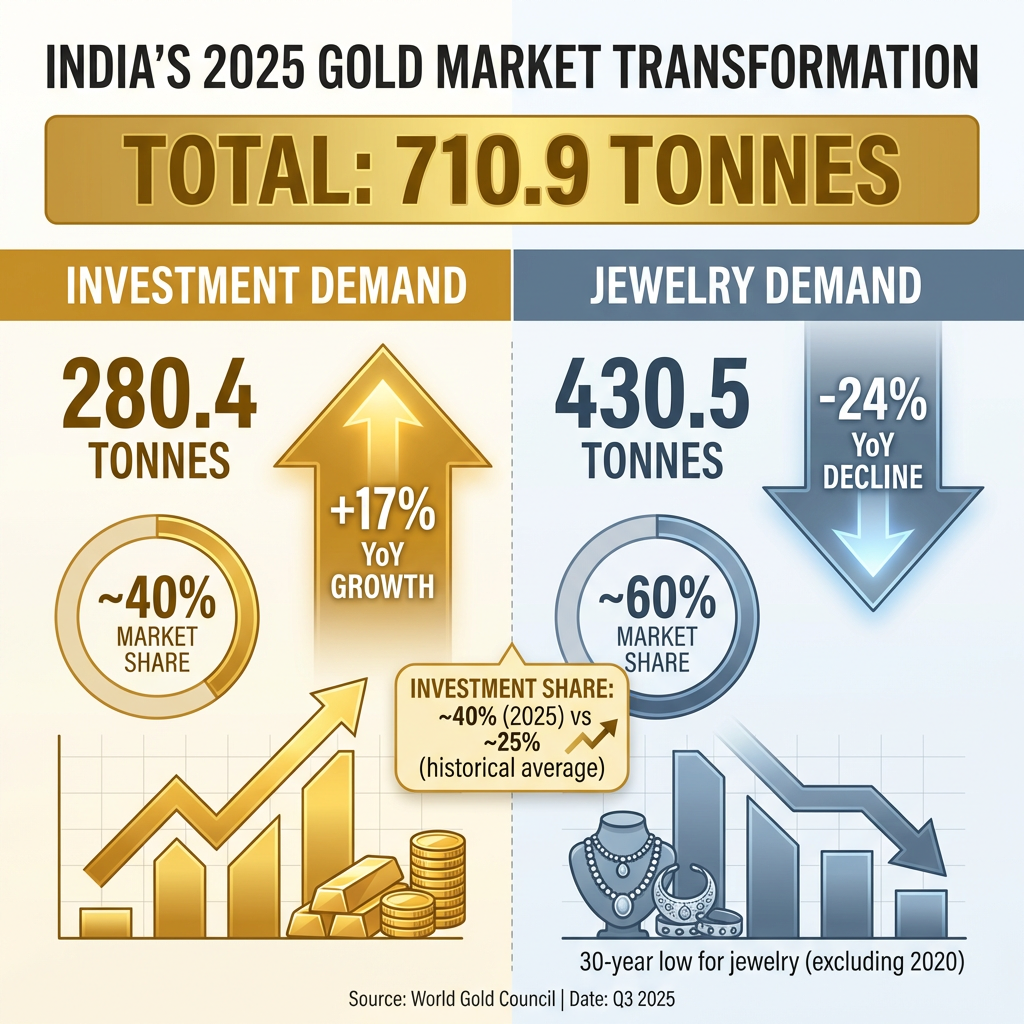

- India gold demand reached 710.9 tonnes in 2025, with investment products capturing approximately 40% of total consumption — up sharply from a historical average of around 25%.

- A 76.5% domestic price surge drove jewelry demand to a 30-year low of 430.5 tonnes, a 24% year-over-year decline, while investment demand rose 17% to 280.4 tonnes.

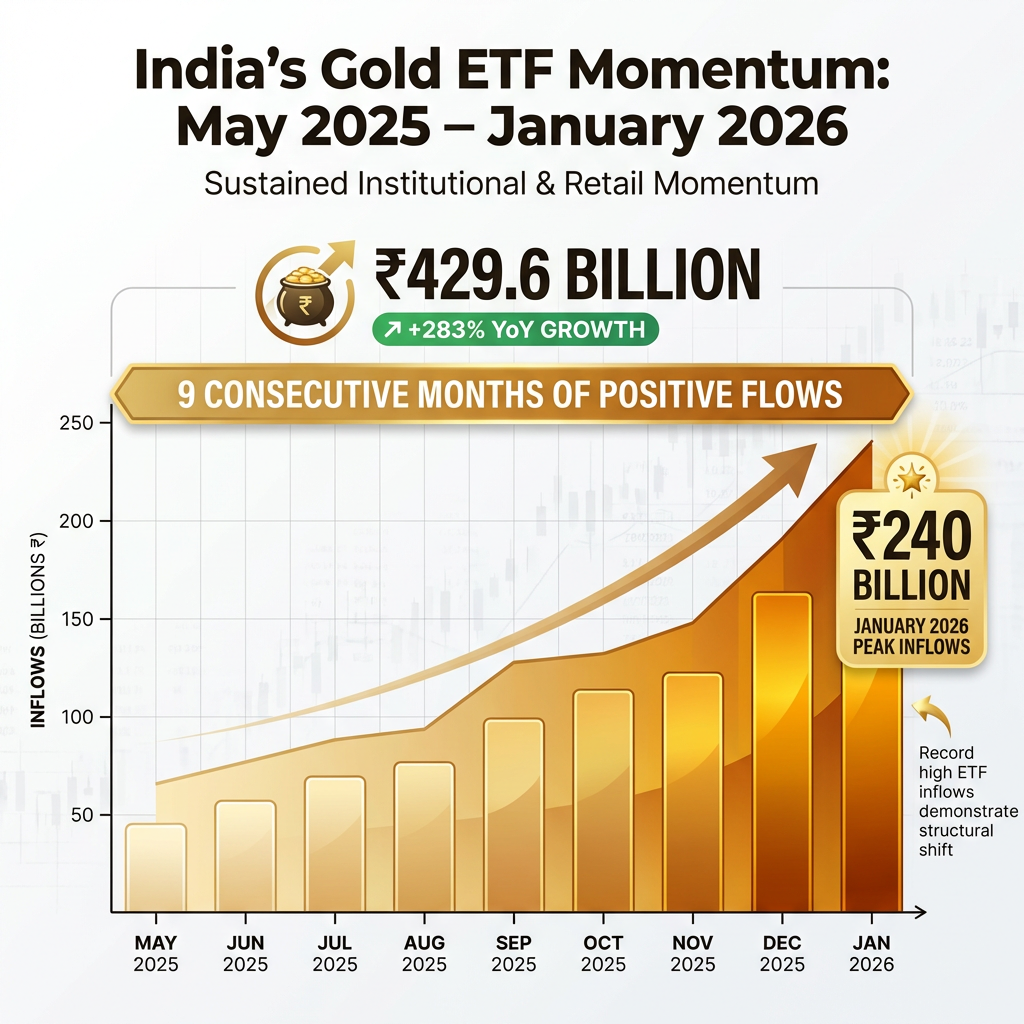

- Indian gold ETF inflows surged 283% in 2025 to ₹429.6 billion, with nine consecutive months of positive inflows recorded through January 2026, signalling a structural rather than temporary shift.

- A February 2026 regulatory change allowing equity mutual funds to allocate up to 35% of residual portfolios to gold and silver ETFs opens a major new institutional demand channel.

- The World Gold Council projects 2026 India gold demand at 600–700 tonnes, with the investment-led bifurcation from jewelry expected to persist as generational mindset shifts and regulatory infrastructure continue to evolve.

The world’s largest gold consumer market is undergoing a historic transformation. India’s 76.5% domestic gold price surge in 2025 has not simply reduced demand—it has fundamentally restructured how 1.4 billion consumers engage with the precious metal, accelerating an unprecedented shift from traditional jewelry purchases toward investment products.

India gold demand reached 710.9 tonnes in 2025, but beneath this headline figure lies a remarkable bifurcation. Investment products captured approximately 40% of total consumption, up from a historical average of about 25%, whilst jewelry demand collapsed to 30-year lows. This structural transformation in the market that accounts for approximately 25% of global gold consumption carries significant implications for worldwide pricing dynamics and mining economics.

Understanding India’s Gold Market: Why It Matters Globally

India’s position as a dominant force in global gold markets makes any structural shift in consumption patterns consequential for worldwide prices and supply chains. The nation represents approximately one-quarter of global gold demand, meaning changes in Indian buying behaviour ripple through international markets with material impact.

Historically, jewelry has accounted for roughly 75% of Indian gold consumption, driven by deeply embedded cultural traditions surrounding weddings, festivals, and intergenerational wealth preservation. Gold ornaments have served not merely as adornment but as tangible stores of value passed through families for generations. The current pivot toward investment products represents a departure from centuries of established purchasing patterns, signalling a fundamental evolution in how Indian households view gold’s primary function.

When big ASX news breaks, our subscribers know first

The Numbers Behind the Transformation: 2025 Market Performance

The 2025 market data reveals two distinct trajectories. Investment demand surged 17% year-over-year to 280.4 tonnes, whilst jewelry consumption contracted 24% to 430.5 tonnes, marking the lowest level in nearly three decades excluding pandemic-affected 2020.

| Category | 2025 Volume/Value | Year-over-Year Change | Market Share |

|---|---|---|---|

| Total Demand | 710.9 tonnes | Decline expected in 2026 | 100% |

| Jewelry Demand | 430.5 tonnes | -24% | ~60% |

| Investment Demand | 280.4 tonnes | +17% | ~40% |

| Gold ETF Inflows | ₹429.6 billion | +283% | Primary investment vehicle |

The gold exchange-traded fund (ETF) story provides particularly compelling evidence of structural change. Indian gold ETFs recorded ₹429.6 billion in inflows during 2025, representing a 283% year-over-year increase and establishing a new record high. This momentum has proven sustained rather than episodic, with ETFs posting their ninth consecutive month of positive inflows as of January 2026, accumulating ₹240 billion during that month alone. Such persistent institutional and retail investor interest suggests this represents a fundamental shift in gold allocation preferences rather than temporary market positioning.

What’s Driving the Investment Pivot

The 76.5% price surge has created an affordability crisis that fundamentally altered purchase calculations for middle-class households. Gold jewelry that once represented accessible discretionary spending has moved beyond many family budgets, forcing consumers to reconsider both whether and how they engage with the precious metal.

Three converging forces are accelerating the investment pivot:

- Price-induced affordability constraints: The dramatic price appreciation has pushed traditional jewelry purchases beyond discretionary budgets for substantial segments of the consumer base, particularly affecting planned wedding and festival purchases

- Modest equity market returns: The Nifty 50 index gained 10.5% in 2025, making gold’s investment characteristics increasingly attractive as portfolio diversification and hedging instruments relative to equity alternatives

- Generational mindset evolution: Younger Indian consumers increasingly view gold primarily as a financial asset class rather than cultural artifact, favouring paper products and investment vehicles over physical ornamental holdings

> Investment products now represent approximately 40% of total gold consumption, a dramatic increase from the historical average of about 25%, representing a clear bifurcation in how Indian consumers are allocating gold spending between traditional jewelry and modern investment products.

Jewelry Market Adaptation: Lighter, Simpler, Investment-Ready

Even within the contracting jewelry segment, an investment-oriented mindset is reshaping consumer preferences. Indian consumers are increasingly choosing lower purity gold jewelry due to elevated price levels, reflecting a pragmatic response to affordability constraints.

Emerging jewelry purchase patterns include:

- Lightweight contemporary designs: Consumers favour pieces with lower gold content by weight, reducing per-item costs whilst maintaining aesthetic appeal

- Plain gold preference: Demand has shifted toward predominantly plain gold jewelry rather than heavily crafted pieces, as intricate workmanship adds cost without preserving intrinsic value

- Lower purity acceptance: Growing popularity of 22k and 18k purity products versus traditional 24k, balancing cost management with gold content

- Dual-purpose purchase motivation: Younger demographics increasingly view jewelry as both wearable and investable assets, prioritising designs that retain more of gold’s underlying value

- Younger demographic engagement: Millennial and Generation Z buyers are entering the market with fundamentally different expectations around jewelry’s primary function

These adaptations provide evidence that the investment mindset is permeating even traditional consumption categories, with buyers seeking jewelry that serves as portable wealth storage rather than purely ornamental function.

Regulatory Catalyst: New Rules Open Institutional Demand Channels

A February 2026 regulatory change introduced by Indian financial authorities could substantially accelerate the investment trend. Actively managed equity mutual funds are now permitted to invest up to 35% of residual portfolio allocation in gold and silver ETFs, creating a significant new institutional demand channel for precious metals exposure.

SEBI’s framework for mutual fund gold and silver ETF investment modified investment norms for actively managed equity mutual funds, permitting holdings of up to 35% in gold and silver ETFs within their residual portfolio allocation framework.

This policy shift effectively allows equity fund managers to increase defensive portfolio positioning through precious metals allocation, normalising gold as a standard diversification tool for mainstream investment products. The timing of this regulatory change, coinciding with sustained retail ETF inflows, could provide structural institutional demand that operates independently of traditional retail jewelry and investment cycles, potentially establishing a sustained demand floor for gold investment products throughout 2026 and beyond.

The institutional shift toward gold-focused institutional investment vehicles reflects broader market dynamics, with major fund launches demonstrating sustained investor appetite for precious metals exposure through structured products.

2026 Outlook: What Comes Next for India Gold Demand

World Gold Council projections indicate total 2026 India gold demand in the range of 600-700 tonnes, representing a potential decline of 10-111 tonnes from 2025 levels. This anticipated contraction reflects continued price sensitivity rather than fundamental market weakness, as the structural transformation from jewelry to investment products continues to reshape demand composition.

According to the World Gold Council’s India demand projections, total 2026 India gold demand is expected in the range of 600-700 tonnes, representing a potential decline of 10-111 tonnes from 2025 levels.

Key outlook factors shaping the 2026-2027 market trajectory include:

- Continued jewelry weakness: Sustained high prices are projected to maintain pressure on traditional jewelry consumption through 2026, with affordability constraints limiting discretionary purchases

- Investment growth trajectory: Investment demand is expected to maintain expansion as Indian households increasingly allocate to paper gold products and ETFs as portfolio diversification tools

- Institutional demand channels: The February 2026 regulatory change allowing equity mutual funds to hold 35% in gold and silver ETFs creates new structural demand sources independent of retail cycles

- Equity market conditions: Analyst expectations of modest equity returns due to high valuations and macroeconomic headwinds support continued gold allocation as an alternative investment

- Structural shift durability: The investment-led transformation appears durable rather than cyclical, supported by generational preference changes and regulatory infrastructure development

Market analysts suggest equity markets may remain subdued due to elevated valuations, tariff concerns, and foreign portfolio outflows, providing a supportive backdrop for gold’s investment appeal to persist through the forecast period.

The next major ASX story will hit our subscribers first

The Bottom Line

India gold demand is experiencing a generational transformation. The 76.5% price surge in 2025 has accelerated a structural shift that may permanently alter how the world’s largest gold consumer market operates, transitioning from a jewelry-dominated, culturally-driven consumption model to an investment-led, financially-motivated allocation framework. Investment products now command approximately 40% of total demand compared to a historical average of about 25%, whilst jewelry consumption has contracted to 30-year lows at 430.5 tonnes.

For global gold markets, this evolution in Indian consumption patterns carries lasting implications. India’s approximately 25% share of worldwide gold demand means structural changes in purchasing behaviour influence international pricing dynamics, mining project economics, and product development strategies across the precious metals industry. As younger Indian demographics embrace investment-oriented approaches and regulatory infrastructure expands institutional access channels, the investment-jewelry bifurcation observed in 2025-2026 may represent the early stages of a permanent market restructuring rather than a cyclical adjustment.

Frequently Asked Questions About India Gold Demand

How much gold does India consume annually?

India consumed 710.9 tonnes of gold in 2025, with 2026 demand projected at 600-700 tonnes by the World Gold Council. This represents approximately 25% of global gold consumption, positioning India as one of the world’s two largest national markets alongside China. The anticipated 2026 decline reflects continued price sensitivity affecting jewelry purchases whilst investment demand maintains growth.

Why is India’s gold jewelry demand declining?

The 76.5% gold price surge in 2025 created severe affordability constraints, pushing jewelry beyond discretionary budgets for many households. Jewelry demand fell 24% to 430.5 tonnes, marking the lowest level in nearly 30 years excluding pandemic-affected 2020. Consumers are responding by shifting to lighter designs, lower purity options (22k, 18k), and in many cases, substituting jewelry purchases with investment products that don’t carry craftsmanship premiums.

What are gold ETFs and why are they popular in India?

Gold exchange-traded funds (ETFs) are investment products that track gold prices and trade on stock exchanges, offering exposure to gold price movements without requiring physical storage, insurance, or security concerns associated with holding bullion or jewelry. Indian gold ETF inflows surged 283% in 2025 to ₹429.6 billion, reflecting investor preference for accessible, liquid gold investment vehicles that can be bought and sold through standard brokerage accounts.

Is the shift from jewelry to investment gold permanent?

Whilst some jewelry demand may recover if prices stabilise or decline, multiple structural factors suggest lasting change. Younger demographics increasingly favour investment approaches over ornamental purchases, February 2026 regulatory changes support institutional gold allocation through mutual funds, and consumer mindset has evolved toward viewing gold primarily as a financial asset rather than cultural artifact. These fundamental shifts indicate the investment-jewelry bifurcation represents a structural market evolution rather than purely cyclical price response.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

What is India gold demand and why does it matter to global markets?

India gold demand refers to the total volume of gold consumed across jewelry, investment, and industrial uses in India, which accounts for approximately 25% of global gold consumption. This makes any structural shift in Indian buying behaviour — such as the 2025 pivot from jewelry to ETFs — consequential for international gold pricing and mining economics.

How much did India's gold investment demand grow in 2025?

Indian gold investment demand surged 17% year-over-year to 280.4 tonnes in 2025, now representing approximately 40% of total gold consumption compared to a historical average of around 25%. Gold ETF inflows alone reached ₹429.6 billion, a 283% increase that established a new annual record.

Why is India's gold jewelry demand at a 30-year low?

A 76.5% gold price surge in 2025 pushed jewelry beyond the discretionary budgets of many Indian households, causing jewelry consumption to fall 24% to 430.5 tonnes — the lowest level in nearly three decades excluding the pandemic year of 2020. Consumers have responded by shifting to lighter designs, lower purity options like 22k and 18k gold, and substituting jewelry purchases with investment products.

What regulatory change could boost India's gold investment demand in 2026?

A February 2026 rule introduced by Indian financial authorities now permits actively managed equity mutual funds to invest up to 35% of their residual portfolio allocation in gold and silver ETFs. This creates a significant new institutional demand channel that could provide a structural demand floor for gold investment products independent of retail cycles.

What is the outlook for India gold demand in 2026?

The World Gold Council projects total India gold demand in the range of 600–700 tonnes for 2026, a potential decline of 10–111 tonnes from 2025 levels, driven by continued price-related weakness in jewelry consumption. Investment demand is expected to keep growing as Indian households and institutions increase allocations to gold ETFs and paper gold products.