Alstom Plunges 17% After Scrapping €1.5bn Cash Flow Target

Key Takeaways

- Alstom shares plunged approximately 17% on 17 April 2026 to around €16.50, marking the stock's lowest level since mid-2024 and its worst single-day performance on the STOXX 600 index.

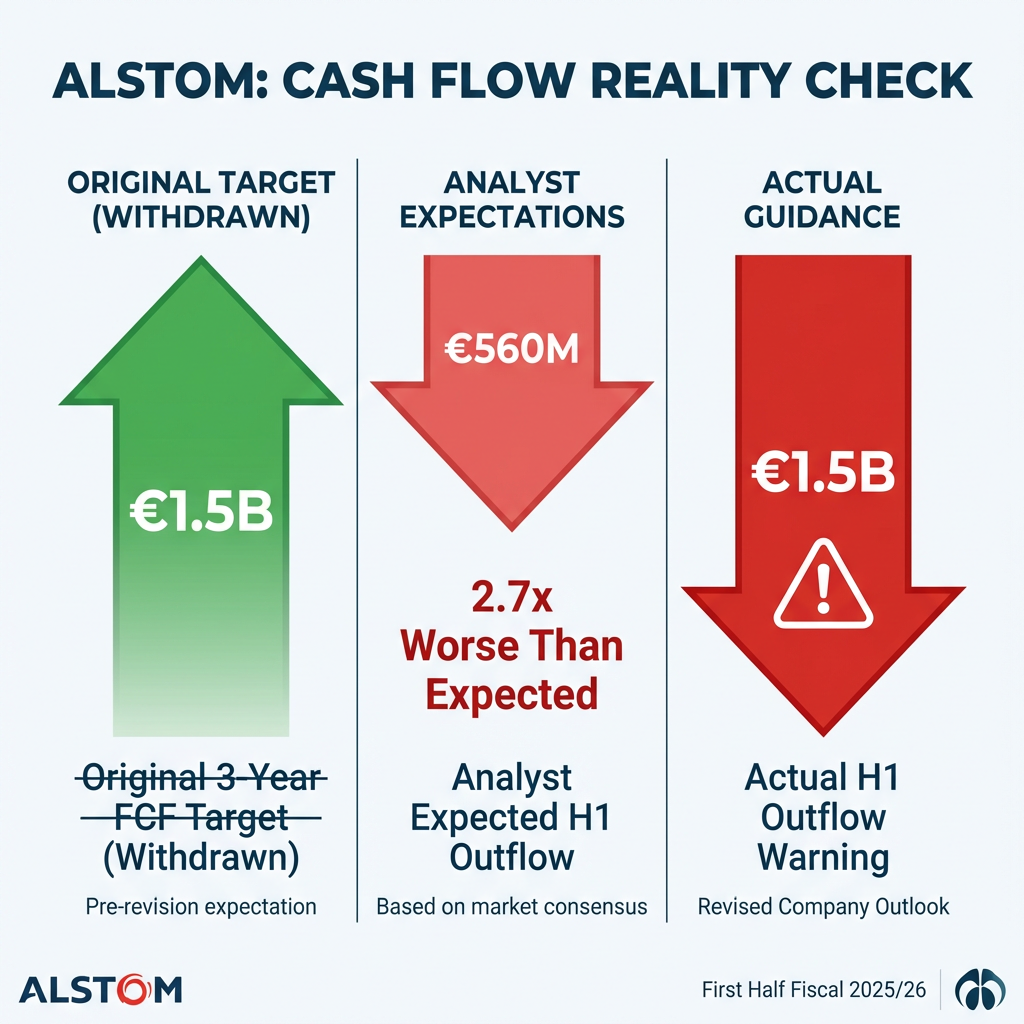

- The company withdrew its €1.5 billion three-year free cash flow target and warned of €1.5 billion in first-half cash outflows, nearly triple analyst expectations of €560 million.

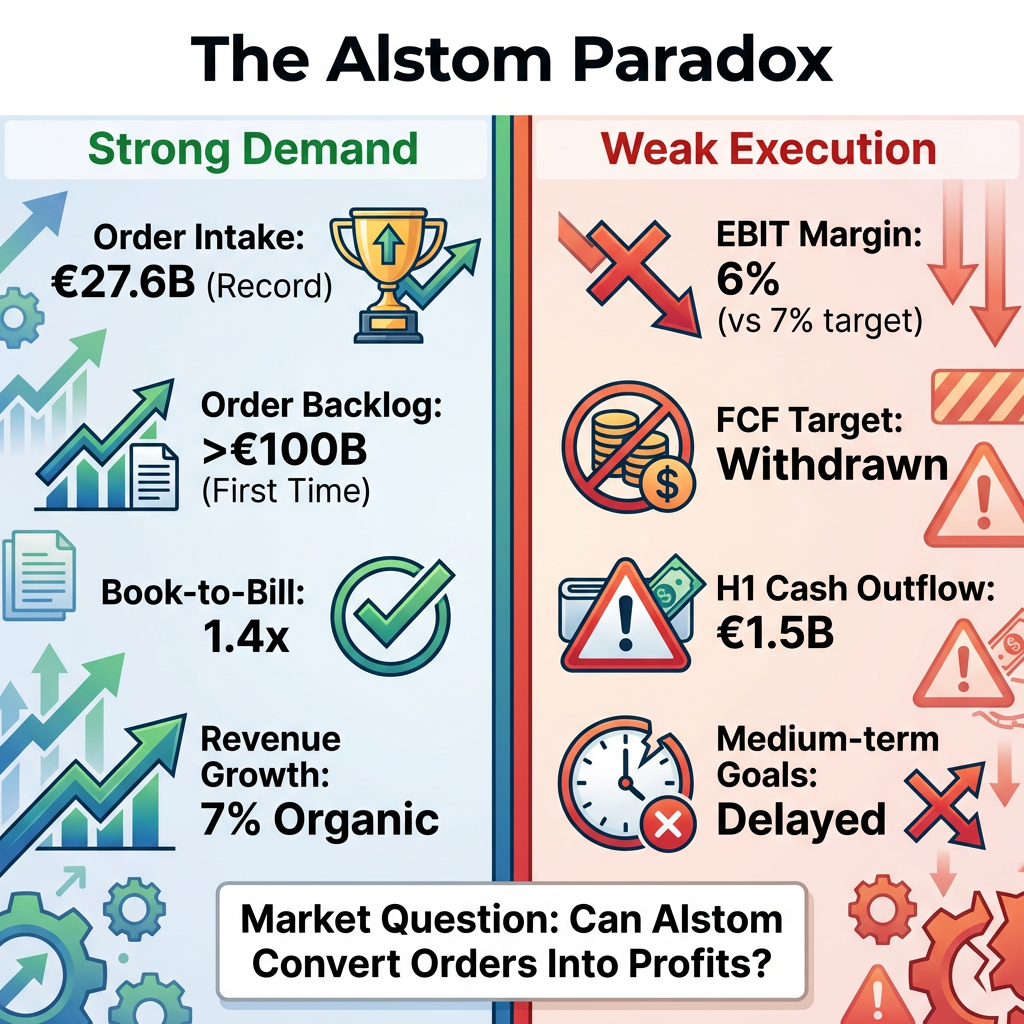

- Despite the cash flow crisis, Alstom reported record order intake of €27.6 billion and a backlog exceeding €100 billion for the first time, highlighting a stark gap between commercial success and operational execution.

- Adjusted EBIT margin missed guidance by 100 basis points at 6% versus the 7% target, with fiscal 2026/27 projections also falling below consensus on both revenue growth and margin.

- Analysts at Citi downgraded Alstom to neutral, warning that project execution failures are eroding the free cash flow progress central to the investment thesis.

French rail equipment manufacturer Alstom suffered one of its worst trading days in recent history on 17 April 2026, with shares plunging approximately 17% to around €16.50. The crash follows the company’s decision to withdraw its €1.5 billion three-year free cash flow target and warn of substantial near-term cash outflows. The stock fell to its lowest level since mid-2024, positioning Alstom as the worst performer on the STOXX 600 index for the day.

The severity of the decline reflects a dramatic loss of investor confidence triggered by the company’s abandonment of specific financial commitments. Management replaced the quantified target with vague guidance for positive free cash flow only by the end of fiscal year 2026/27, extending the recovery timeline by at least 18 months.

Why free cash flow targets matter for industrial stocks

Free cash flow represents the cash a company generates after covering operating costs and capital expenditures. This metric is particularly critical for capital-intensive industrial manufacturers like Alstom, which operate long project timelines and require substantial upfront investments. FCF indicates the money available for dividends, debt repayment, or reinvestment in growth.

When a company withdraws free cash flow guidance, it signals management can no longer predict cash generation with confidence. This raises fundamental questions about financial stability and operational control. For investors in industrial stocks, FCF serves as a key health indicator, directly affecting debt servicing capacity and shareholder returns.

The severe market reaction aligns with NBER research on how markets value cash flow changes, which demonstrates that unexpected deterioration in free cash flow expectations triggers disproportionate stock price volatility in capital-intensive industrial sectors.

When big ASX news breaks, our subscribers know first

What triggered the guidance withdrawal

Alstom’s decision to abandon its €1.5 billion free cash flow target stems from a combination of rolling stock project execution failures and a dramatic near-term cash outflow warning. The company now expects €1.5 billion in cash outflows during the first half of the new fiscal year, nearly triple analyst expectations of approximately €560 million. This massive variance made the previous three-year cumulative target impossible to maintain.

The withdrawal of financial guidance by French-listed companies falls under strict disclosure obligations set out in the AMF guidance on ongoing information and management of inside information, which implements the Market Abuse Regulation for companies traded on Euronext Paris.

The operational root causes centre on rolling stock project execution challenges, slower-than-expected ramp-up of newer projects, and working capital pressures driven by growth. These factors compressed the adjusted EBIT margin to 6% versus 7% guidance, representing a 100 basis point miss. Production difficulties and inventory surges further strained cash conversion.

While Alstom faces project execution difficulties in rail manufacturing, operational execution challenges affecting companies across diverse industries—from consumer staples to infrastructure—highlight how supply chain and production problems can quickly erode investor confidence regardless of sector.

Management confirmed the company’s medium-term goal of achieving 8-10% EBIT margins will not be reached by fiscal 2026/27. This timeline extension compounds investor concerns about the company’s ability to execute projects profitably, despite strong commercial demand.

Fiscal 2025/26 results: A mixed picture

Alstom’s preliminary results present a paradox of commercial success alongside operational underperformance. Order intake reached record levels at €27.6 billion. The order backlog exceeded €100 billion for the first time, with a healthy 1.4x book-to-bill ratio signalling sustained demand.

Revenue performance beat forecasts, delivering 4% overall growth and 7% organic growth. However, profitability metrics disappointed, with the 6% EBIT margin falling short of the 7% target.

| Metric | Actual Result | Guidance/Consensus |

|---|---|---|

| EBIT Margin | ~6% | ~7% |

| Order Intake | €27.6 billion | Record level |

| Revenue Growth | 4% (7% organic) | Above forecast |

| Order Backlog | >€100 billion | Record level |

The disconnect between top-line strength and profitability weakness highlights the central concern. The market punished Alstom not for lack of demand, but for inability to convert orders into expected profits and cash flow. Strong commercial momentum means little if the company cannot execute projects profitably.

Analyst reaction and forward outlook

Citi analysts downgraded Alstom to neutral following the announcement, characterising the update as disappointing. According to Citi, strong order demand and a growing backlog at improved margins are undermined by project execution problems, which are eroding the free cash flow progress that forms the central investment thesis. Jefferies echoed similar concerns, noting execution failures are the critical weakness.

Forward guidance for fiscal 2026/27 came in below consensus across key metrics. The company projects approximately 5% organic revenue growth versus 5.4% consensus expectations, and 6.5% EBIT margin versus 7.1% consensus. Alstom’s CFO indicated net debt is expected to remain stable or increase modestly, adding to balance sheet concerns.

Companies across the industrial sector have been implementing industrial sector guidance revisions in recent months, with external pressures and internal execution issues combining to force management teams to reset financial expectations.

Alstom’s situation mirrors a broader pattern of industrial companies struggling with execution challenges, as seen in recent guidance revisions across multiple sectors where management teams have had to reset investor expectations amid operational pressures.

Analysts believe the balance sheet can absorb near-term free cash flow weakness, including the substantial first-half outflow. However, they warned the margin for error is narrowing significantly. The company must demonstrate improved execution in coming quarters to rebuild investor confidence.

The next major ASX story will hit our subscribers first

What comes next for Alstom investors

Alstom’s path forward depends on demonstrating improved project execution and stabilising cash flow generation. Management must rebuild trust after abandoning specific targets, with positive free cash flow now expected only by the end of fiscal 2026/27. This timeline means at least 18 months before financial recovery can be verified.

Key monitoring points for investors include:

- Quarterly EBIT margin trends and signs of improvement from the 6% baseline

- First-half cash outflow actual performance versus the €1.5 billion expectation

- Project execution updates, particularly on problematic rolling stock contracts

- Debt levels and balance sheet health as net debt evolves

- Any further guidance revisions or strategic announcements

The €100 billion-plus backlog and continued order momentum provide a foundation for eventual recovery. Commercial demand remains robust, evidenced by record order intake and the strong book-to-bill ratio. However, the 17% crash reflects how severely investors have repriced near-term expectations and execution confidence. The company faces significant pressure to deliver on operational improvements and restore credibility with the market.

Frequently Asked Questions

Why did Alstom stock crash?

Alstom shares crashed due to the company’s withdrawal of its €1.5 billion three-year free cash flow target and warning of €1.5 billion in cash outflows during the first half of fiscal 2025/26, compared to analyst expectations of approximately €560 million. Preliminary fiscal 2025/26 results showed the adjusted EBIT margin missed guidance by 100 basis points, signalling management has lost control over the financial trajectory.

How much has Alstom stock fallen?

Alstom shares fell approximately 17% on 17 April 2026, dropping to around €16.50. This represents the lowest level since mid-2024 and marks one of the most severe single-day declines in recent company history.

What is Alstom’s new financial guidance?

Alstom now expects positive but unquantified free cash flow only by the end of fiscal year 2026/27. For the immediate fiscal year, the company projects approximately 5% organic revenue growth and 6.5% EBIT margin, both below analyst consensus expectations of 5.4% and 7.1% respectively. The previous €1.5 billion three-year cumulative free cash flow target has been completely withdrawn.

Is Alstom at risk of financial distress?

Analysts believe Alstom’s balance sheet can absorb near-term free cash flow weakness, but the margin for error is narrowing. The company maintains a record €100 billion-plus order backlog, providing long-term revenue visibility. However, net debt is expected to remain stable or modestly increase, and operational execution must improve to avoid further deterioration.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

Why did Alstom stock crash on 17 April 2026?

Alstom shares crashed approximately 17% after the company withdrew its €1.5 billion three-year free cash flow target and warned of €1.5 billion in cash outflows in the first half of fiscal 2025/26, nearly triple analyst expectations of €560 million.

What is free cash flow and why does it matter for Alstom investors?

Free cash flow is the cash a company generates after covering operating costs and capital expenditures, and for capital-intensive industrial manufacturers like Alstom it is a critical indicator of financial health, debt servicing capacity, and ability to return value to shareholders.

What is Alstom's new financial guidance after the target withdrawal?

Alstom now targets positive but unquantified free cash flow only by the end of fiscal year 2026/27, projects approximately 5% organic revenue growth and a 6.5% EBIT margin for the coming year, both below analyst consensus expectations.

Is Alstom at risk of financial distress following the stock crash?

Analysts believe Alstom's balance sheet can absorb near-term free cash flow weakness, supported by a record €100 billion-plus order backlog, but warn the margin for error is narrowing and net debt is expected to remain stable or modestly increase.

What should investors monitor to assess Alstom's recovery?

Investors should track quarterly EBIT margin trends, actual first-half cash outflow performance versus the €1.5 billion expectation, progress on problematic rolling stock contracts, and any further guidance revisions or debt level changes.