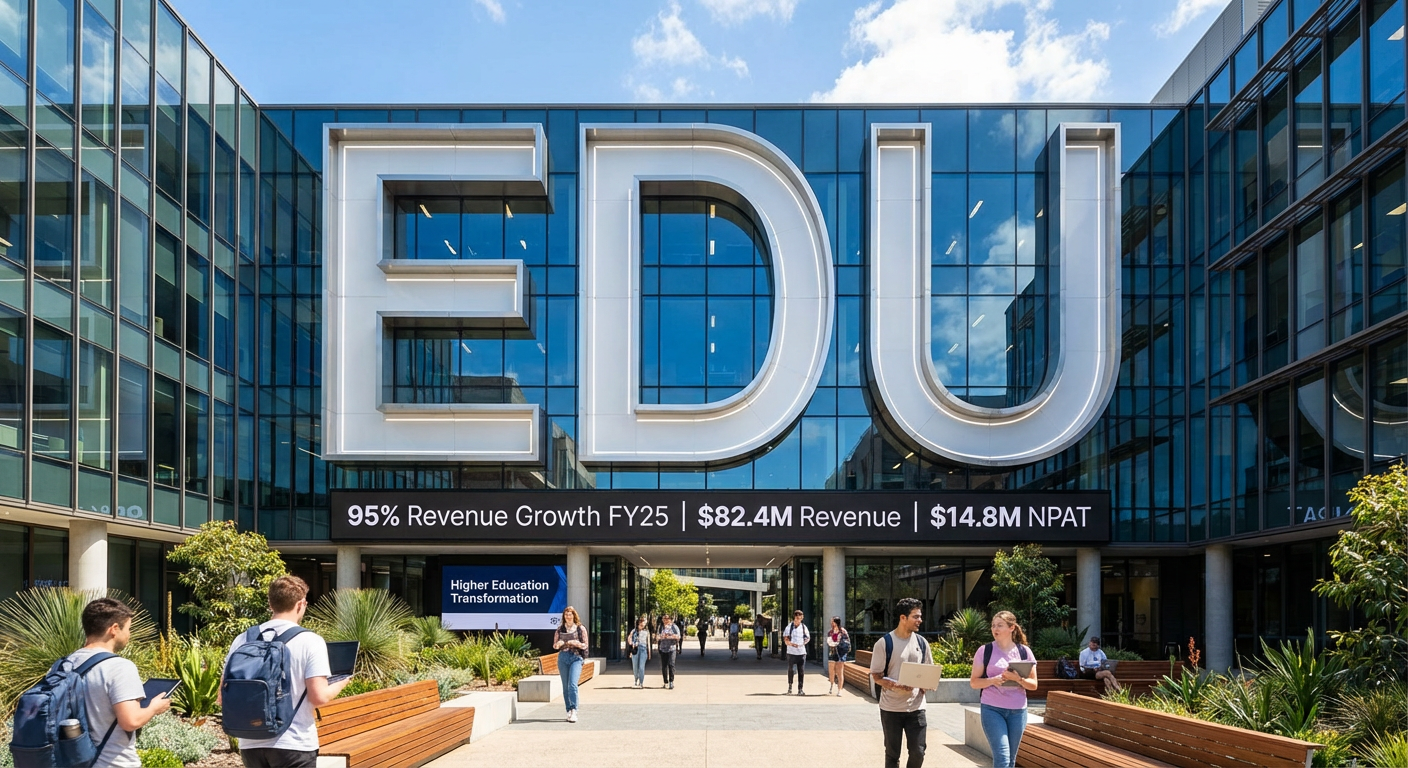

EDU Holdings delivers 95% revenue growth and record earnings in FY25

EDU Holdings (ASX: EDU) reported revenue of $82.4m for the year ended 31 December 2025, representing 95% growth on the prior corresponding period. Net profit after tax surged to $14.8m, up from $2.6m in FY24, with the NPAT margin expanding 12 percentage points to 18%. The company generated $24.0m in net operating cashflow and ended the period with $18.5m in net cash after fully repaying borrowings of $1.5m, executing on-market buybacks totalling $3.6m, and paying $1.5m in dividends. The board declared an interim fully-franked dividend of $0.01 per share and a final fully-franked dividend of $0.03 per share.

Investment Significance

The FY25 result marks a structural step-change rather than a cyclical uptick. EDU’s strategic pivot towards higher education has materially improved revenue per student, extended average study duration to 35 months, and driven margin expansion across the business. The combination of cohort layering, diversified recruitment channels, and disciplined cost management positions the group for multi-year earnings visibility.

The transformation is underpinned by Ikon Institute’s continued momentum. Ikon delivered $65.9m in revenue (up 135%) and $26.1m in EBITDA (up from $8.9m), with period-end students reaching 4,537 compared to 2,492 in the prior year. Higher education now accounts for 80% of Group revenue, compared to 45% in FY22, fundamentally altering the quality and durability of earnings.

When big ASX news breaks, our subscribers know first

Understanding the higher education pivot

The shift from vocational education and training (VET) to higher education (HE) represents the core strategic narrative behind EDU’s performance improvement. Bachelor’s degree programs average $56,000 in revenue compared to diplomas at $20,000 and certificates at $9,700. Masters programs contribute $42,000 on average. More importantly, the average study duration has extended to 35 months in FY25 from 26 months in FY22, creating cohort layering that provides multi-year revenue visibility and reduces reliance on continual new student acquisition.

| Course Type | Average Price | Average Duration |

|---|---|---|

| Certificates | $9,700 | <1 year |

| Diplomas | $20,000 | 1-2 years |

| Bachelors | $56,000 | 3-4 years |

| Masters | $42,000 | 18 months – 2 years |

Higher education enrolments now represent 75% of domestic enrolments delivered online, up from 39% in FY22, reflecting the scalability of the online delivery model. The course portfolio has expanded to 313 courses in FY25 from 22 in FY22, with 95% of FY25 enrolments in Community Services courses aligned to identified skills shortages. The combination of higher-value programs, longer duration, and alignment to workforce priorities has driven sustainable margin improvement and reduced earnings volatility.

Ikon Institute continues to drive Group performance

Ikon’s Trimester 3 2025 enrolments increased 82% on the prior corresponding period, benefiting from a high proportion of students in early stages of study. New courses launched during 2025 accounted for 752 enrolments in T3’25, representing 17% of total enrolments and 24% of Trimester 1 2026 enrolments. Domestic enrolments in T3’25 grew 30% year-on-year, with encouraging uptake of newly launched programs.

The company has expanded offshore recruitment with full-time in-country sales managers now operating in Spain, Colombia, Brazil, Philippines, Nepal, Nigeria and Kenya, though management noted these channels will take time to build meaningful volume. Ikon’s new student enrolments for FY25 totalled 2,672, up from 1,911 in the prior year.

ALG navigating softer VET market conditions

Australian Learning Group (ALG) reported total FY25 enrolments up 11% despite challenging regulatory conditions in the vocational education sector. However, new student enrolments declined 43% year-on-year as graduations from larger prior cohorts outpaced new enrolments. Revenue increased 16% to $16.5m, and EBITDA rose to $2.9m from $1.3m. The segment returned to profitability with $0.4m NPAT compared to a $0.7m loss in FY24.

Management emphasised ALG’s strategic value as an articulation pathway provider, supporting student progression from VET qualifications into higher-value higher education programs. This pathway function supports EDU’s broader growth engine while the regulatory environment for VET remains constrained.

Strong cash generation and shareholder returns

Net operating cashflow reached $24.0m, up $12.7m from the prior year, with free cashflow of $18m representing 120% NPAT conversion. The company finished the year with a net cash position of $18.5m and no debt, having fully repaid $1.5m in borrowings during the period.

Capital management initiatives during FY25 included:

- On-market buybacks totalling $3.6m executed throughout the year

- Selective buyback of 18 million shares at $0.55 per share completed in February 2026, totalling $9.9m and delivering a pro-forma earnings per share increase of 12.5%

- Additional on-market buyback of up to 14.4 million shares approved at the recent extraordinary general meeting

- Total FY25 dividend of $0.04 per share fully-franked (interim $0.01, final $0.03)

Strong free cashflow conversion and balance sheet capacity demonstrate earnings quality and provide management with strategic flexibility to fund growth initiatives while returning surplus capital to shareholders.

Navigating the regulatory environment

Three regulatory developments are reshaping the international education sector in Australia. The National Planning Limit (NPL) for 2026 has been set at 295,000, up from 270,000 in 2025, with growth weighted toward higher education and public universities. EDU’s provider planning limits are 205 for Ikon and 471 for ALG.

Ministerial Direction 115, which commenced 14 November 2025, directs the Department of Home Affairs to prioritise offshore student visa processing based on provider planning limit utilisation. Applications are categorised into three levels: Level 1 (up to 80% of planning limit), Level 2 (80-115%), and Level 3 (exceeding 115%). Planning limits are not hard caps, and all applications continue to be processed at varying speeds.

Recent amendments to the National Code 2018 restrict providers from paying commissions to education agents for recruiting onshore transferring students. However, students remain expressly permitted to transfer, providers may support transfer processes, and agents may assist with transfers and charge students directly. The restrictions do not apply to domestic students, offshore students, or onshore students commencing new courses after completing their principal course.

EDU’s response to regulatory headwinds

Management has outlined a three-pillar response strategy:

- Proven execution track record: Consistent higher education enrolment growth and strong FY25 cash generation support reinvestment capacity and strategic flexibility. The company has demonstrated ability to adapt to regulatory disruption in prior cycles.

- Portfolio and recruitment diversification: Broadening course offerings aligned to skills priorities, with new higher education courses launched in 2025 accounting for 24% of T1’26 enrolments. Continued investment in offshore and direct recruitment channels, increased focus on domestic student market, and development of alternative engagement models to maintain agent support.

- Disciplined operating model: Centralised, scalable shared services supporting strategic priorities, disciplined cost management focused on campus utilisation and class size optimisation, and flexibility to adjust growth pace as conditions evolve. Strong governance, compliance and quality frameworks underpin sustainable operations.

FY26 outlook and guidance

Management expects revenue, EBITDA and NPAT to increase on FY25. The year has started strongly, with Group T1’26 enrolments up 36% on the prior corresponding period. The continued shift toward higher education is evident, with 90% of T1’26 new student enrolments from higher education programs.

Investment “ahead of the curve” will result in a step-up in costs to support growth initiatives. Further guidance will be provided later in the year as the impact of regulatory changes becomes clearer. The selective buyback of 18 million shares completed in February 2026 delivered a pro-forma EPS increase of 12.5%, with the on-market buyback of up to 14.4 million shares approved at the recent extraordinary general meeting providing additional capital management flexibility.

Board Commentary

The board remains confident in EDU’s long-term positioning as a quality provider in high-growth sectors, noting diversification strategies are well-progressed despite ongoing uncertainty regarding the full impact of regulatory changes.

The balance between funding growth initiatives, maintaining balance sheet strength, and returning surplus capital to shareholders via dividends and share buybacks will remain an ongoing focus for management.

Want the Next Education Sector Winner in Your Inbox?

Join 20,000+ investors receiving FREE ASX breaking news and in-depth analysis delivered within minutes of release. Get Big News Blast alerts the moment market-moving announcements hit—complete with expert coverage you can act on immediately. Click the “Free Alerts” button to start receiving real-time updates.