In May 2026, analysts at Piper Sandler made a claim that most major institutions have carefully avoided: the United States is already inside the early phase of a fiscal crisis, not approaching one. The assertion lands against a backdrop of public debt above 100% of GDP, a $1.7 trillion deficit recorded during full employment in FY 2024, and $659 billion in net interest outlays that now consume roughly 13% of the federal budget. With the Congressional Budget Office (CBO) projecting debt at 116% of GDP by 2035, the structural picture underpinning Piper Sandler’s conclusion has been building for years. What follows examines the conditions that led the firm to that conclusion, the structural buffers it says remain intact, why political dysfunction makes resolution unlikely, and the signals investors should monitor in Treasury markets for evidence the crisis is deepening.

Piper Sandler’s diagnosis: why this is a crisis, not a warning

The word matters. Most institutional commentary on U.S. fiscal health, from the IMF to the CBO to Goldman Sachs, has settled on “unsustainable trajectory” or some variation of it. Piper Sandler crossed that line, characterising current conditions as the opening phase of something already underway.

Piper Sandler has described the current U.S. fiscal environment as “the early phase of a fiscal crisis.”

The firm’s diagnosis does not rest on a single metric. It rests on a specific combination of structural conditions arriving simultaneously:

- Public debt exceeding 100% of GDP (the CBO estimated 99% at end-2024, projected to reach 101% in 2025)

- A federal deficit of approximately $1.7 trillion, or 6.3% of GDP, occurring during full employment rather than recession

- Post-Global Financial Crisis (GFC) and post-COVID debt accumulation compounding into a self-reinforcing cost structure

- Policymaker behaviour patterns that the firm identifies as structurally incapable of correcting the trajectory

That last point distinguishes the Piper Sandler note from balance-sheet-only analyses. The firm treats political inaction not as a background risk but as a diagnostic input, one that confirms the system has entered crisis rather than merely approaching it.

When big ASX news breaks, our subscribers know first

The interest cost spiral that changes the arithmetic

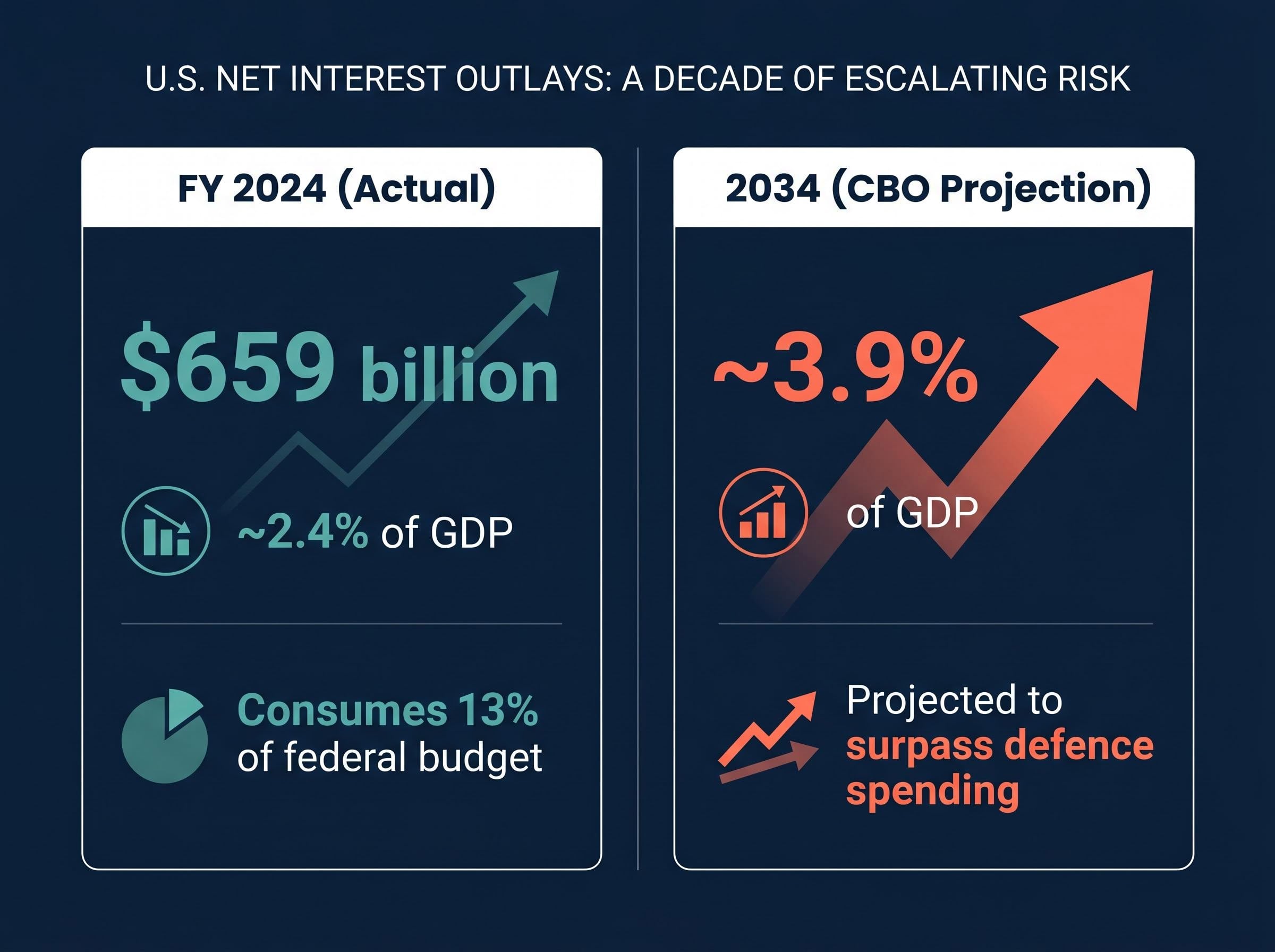

The structural shift becomes clearest in a single line item: federal interest payments. In FY 2024, net interest outlays reached $659 billion, consuming approximately 13% of total federal spending. A decade earlier, the same debt carried at near-zero rates looked manageable. Rate normalisation changed the arithmetic entirely.

| Period | Net Interest (% of GDP) | Context |

|---|---|---|

| FY 2024 (actual) | ~2.4% ($659 billion) | Already exceeds most non-defence discretionary categories |

| 2034 (CBO projection) | ~3.9% | Projected to surpass defence spending as a share of GDP |

The CBO projects that net interest costs will surpass defence spending as a share of GDP by 2034, a threshold that has no precedent in the modern federal budget.

Piper Sandler highlights a compounding vulnerability within this trajectory: the government’s heavy reliance on short-term Treasury bills to contain near-term interest expenses. While T-bill issuance lowers the immediate coupon burden, it concentrates rollover risk. If a recession coincides with a market correction, forcing the Treasury to refinance enormous volumes at elevated rates, deficits could spike to historically rare levels, feeding the interest cost problem further. The dynamic is self-reinforcing: higher debt produces higher interest costs, which widen deficits, which produce more debt.

What a sovereign fiscal crisis actually looks like, and where the U.S. sits

A sovereign fiscal crisis, in practical terms, is a condition where a government can no longer finance its obligations at sustainable rates without triggering a self-reinforcing spiral: rising borrowing costs erode credibility, reduced credibility raises borrowing costs further, and the policy space to correct course narrows with each cycle. It does not require a missed payment. It requires a loss of fiscal control.

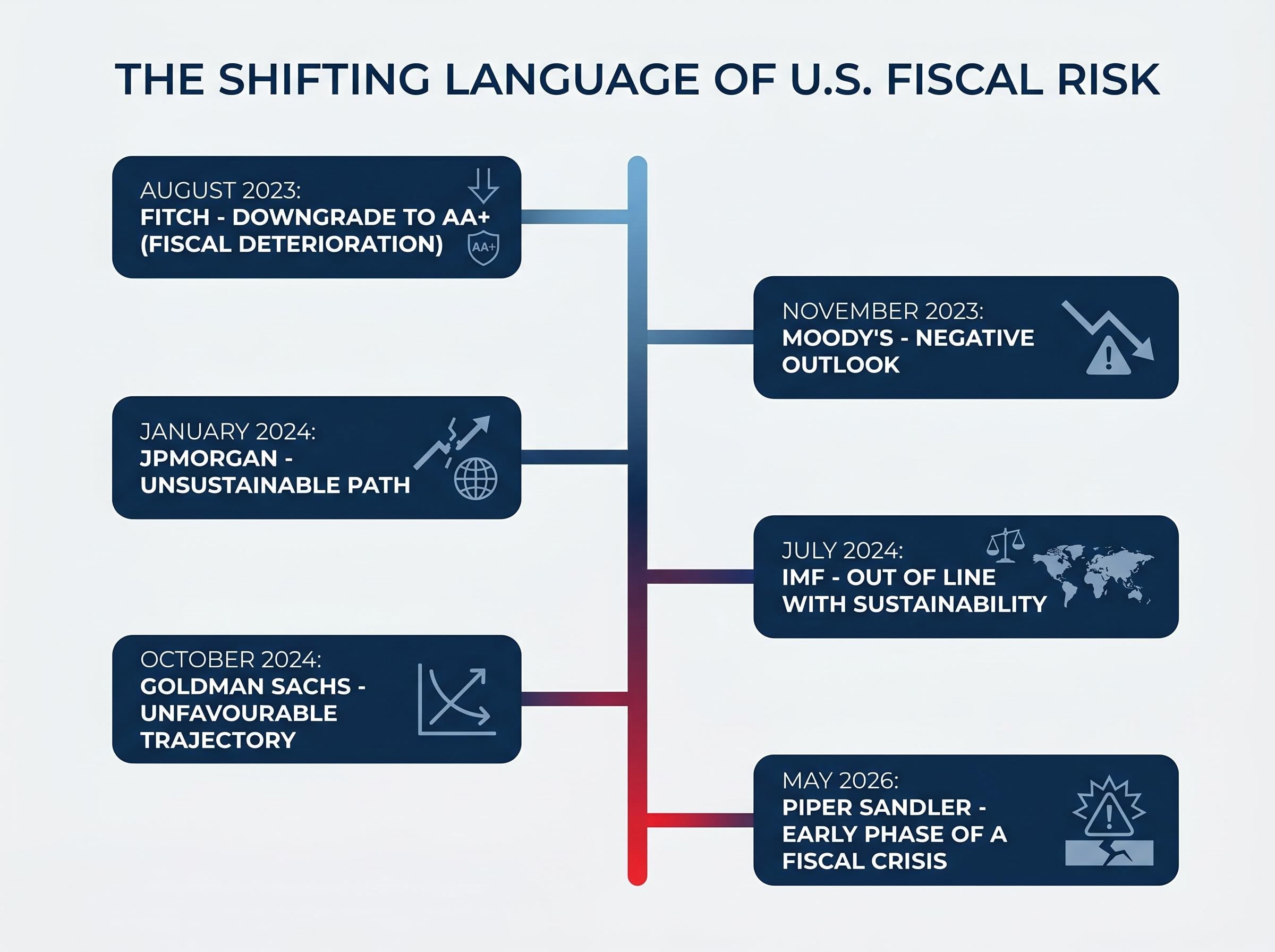

By that definition, the U.S. shares several features with historical crisis cases. The IMF reported general-government gross debt at approximately 122% of GDP in 2023 (a broader measure including state and local obligations). Fitch downgraded the U.S. sovereign rating from AAA to AA+ in August 2023, citing fiscal deterioration and repeated debt-limit standoffs. Moody’s moved its outlook to Negative in November 2023. The CBO projects debt held by the public reaching 166% of GDP by 2054 under current law.

The U.S. buffers that remain, and why they do not resolve the concern

Piper Sandler acknowledges that the U.S. retains structural advantages that most sovereign crisis cases lacked:

- Dollar reserve currency status, which sustains global demand for Treasury securities

- Deep, liquid Treasury markets, the largest and most actively traded government bond market in the world

- Substantial taxation capacity, with federal revenue well below the levels seen in comparable advanced economies

- Federal Reserve stabilisation capability, including the ability to act as a backstop buyer in extremis

- Geopolitical standing, which reinforces the dollar’s role in trade settlement and reserve holdings

The firm treats these buffers as real. It does not treat them as sufficient. Its argument is that these advantages delay the reckoning rather than prevent it, and that their gradual erosion, through political dysfunction, rising debt servicing costs, and shifting global reserve allocations, is itself part of the crisis diagnosis.

Why political dysfunction is now a structural input, not a temporary obstacle

Piper Sandler’s assessment of the political environment is blunt. The firm identifies the measures that would be necessary to stabilise the fiscal trajectory:

- Reductions to entitlement programmes, including Medicaid

- Expanding the taxpayer base through broader or higher taxation

- Reducing overall government borrowing through sustained spending discipline

Each of these is broadly unpopular. The firm concludes that neither major party is likely to implement them. Republicans have resisted tax increases; Democrats have resisted entitlement cuts. The result, in Piper Sandler’s framing, is that the most probable policy outcomes lead to a budgetary crisis, higher taxes, or a combination of both, arrived at by force rather than design.

Piper Sandler has assessed that an adequate government response to the fiscal trajectory is “nearly impossible.”

The firm also notes that President Trump’s pressure on the Federal Reserve to lower interest rates addresses the symptom (interest costs) rather than the structural cause (deficit levels). Lower rates would reduce the government’s borrowing expenses in the near term but would do nothing to alter the trajectory of debt accumulation.

Goldman Sachs, JPMorgan, and the Brookings Institution have all separately identified entitlement reform and tax increases as prerequisites for any meaningful fiscal stabilisation, reinforcing the breadth of institutional agreement on the remedies, if not the political will to pursue them. Piper Sandler’s contribution is stating plainly what that political reality implies: investors should assume the response will be inadequate.

The signals investors should watch as the crisis evolves

The distinction between a fiscal concern and an active fiscal crisis will ultimately be settled in markets. The following signals, drawn from institutional research and market commentary, form a surveillance framework for tracking whether fiscal stress is intensifying:

- Treasury auction performance: Bid-to-cover ratios and auction tails (the gap between auction yield and pre-auction when-issued yield) are the most direct measures of whether demand is absorbing expanding supply. Bank of America’s Michael Hartnett warned of a potential “Treasury tantrum” driven by fiscal concerns in March 2024.

- Term premium trajectory: Rising term premia in 10-year and 30-year Treasuries, particularly when disconnected from Federal Reserve policy expectations, signal that investors are demanding compensation for sovereign fiscal risk specifically.

- Foreign demand via TIC data: Brad Setser of the Council on Foreign Relations (CFR) has framed foreign buying as a variable directly tied to fiscal sustainability. Shifts in holdings by major foreign holders, particularly Japan and China, bear monitoring.

- T-bill share of outstanding debt: A rising share of short-term bills in the debt stock signals growing rollover risk, the vulnerability Piper Sandler specifically flagged.

- Credit-rating actions: Moody’s Negative outlook and Fitch’s AA+ rating already represent markers of eroded fiscal credibility. Any further downgrades or outlook changes would represent a material escalation.

Institutional and political triggers that could accelerate the timeline

Beyond market signals, Piper Sandler has indicated that significantly higher interest rates would likely be needed to motivate legislative intervention, a threshold the firm considers high given the political dynamics described above. The interaction between the Fed’s balance sheet and Treasury issuance volumes also warrants attention: if rising interest costs begin to pressure Fed communications around the pace of quantitative tightening or rate normalisation, fiscal dominance (where debt levels effectively constrain monetary policy) would move from a theoretical risk to an observable one.

The next major ASX story will hit our subscribers first

The Piper Sandler warning in the context of a crowded institutional conversation

Piper Sandler is not alone in its concern. What distinguishes the firm is its language.

| Institution | Assessment Summary | Language Used |

|---|---|---|

| IMF (July 2024) | U.S. fiscal policy inconsistent with sustainability | “Out of line with long-term fiscal sustainability” |

| Fitch (August 2023) | Downgrade from AAA to AA+ | “Fiscal deterioration,” governance weaknesses |

| Moody’s (November 2023) | Outlook moved to Negative | “Deterioration in debt affordability” |

| BlackRock (June 2024) | Structurally higher deficits imply sustained yield pressure | “Higher for longer” yields |

| Goldman Sachs (October 2024) | Unfavourable debt trajectory, rising term premium likely | “Unfavourable,” term-premium concerns |

| Piper Sandler (May 2026) | U.S. already in crisis; policymaker behaviour confirms diagnosis | “Early phase of a fiscal crisis” |

The spectrum runs from cautionary trajectory language to explicit crisis language. Piper Sandler sits at the sharpest end, distinct not because its data differs but because it integrates policymaker behaviour into the diagnosis and states the conclusion most others imply. The firm advises investors to operate under the assumption that government responses will most likely be inadequate or fiscally irresponsible, a posture more direct and actionable than the carefully hedged language of most institutional notes. JPMorgan’s Michael Cembalest described the U.S. fiscal path as “unsustainable” without entitlement reform or tax increases in January 2024, arriving at a similar destination through softer phrasing.

Whether Piper Sandler is precisely correct matters less than what the note represents: a shift in how at least some institutional voices are willing to characterise U.S. fiscal conditions. The language is moving.

The fiscal reckoning may already be underway

Piper Sandler’s core argument is that the United States has structural advantages that delay but do not prevent a fiscal reckoning, and that the political system has demonstrated it will not act until rates and markets force the issue. The investment implication is not panic positioning. It is elevated vigilance: monitoring Treasury auction demand, term-premium behaviour, foreign holdings data, and credit-rating trajectory for signs that the market is beginning to price what the balance sheet already shows.

The significance of the note lies less in whether every element of the firm’s timing proves accurate and more in what it signals about how institutional thinking on U.S. sovereign risk is evolving. The language is sharpening. The buffers are real but finite. The arithmetic, for now, continues to compound.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking projections, including CBO estimates and institutional forecasts, are subject to change based on economic conditions, policy developments, and market dynamics.