Apple Stock Analysis: 30% Upside vs Tariff Risk Before Earnings

Key Takeaways

- Apple delivered a strong fiscal Q1 2026 earnings beat with EPS of $2.84 versus the $2.67 estimate and 15.7% revenue growth, yet the stock remains down 5.7-9% year-to-date due to tariff and macro headwinds.

- Wall Street's Moderate Buy consensus targets 17-20% upside to $297-$304, with Wedbush's Dan Ives maintaining a Street-high $350 target based on Apple's AI integration strategy and M5 Mac product pipeline.

- A Morgan Stanley survey recorded a record 37% iPhone upgrade intent among existing users, supporting sustained demand momentum into the iPhone 17 cycle and fiscal Q2 2026 results.

- Tariff exposure from Apple's China supply chain concentration and the need to demonstrate tangible AI monetisation represent the primary risks that could compress the current 32x earnings multiple.

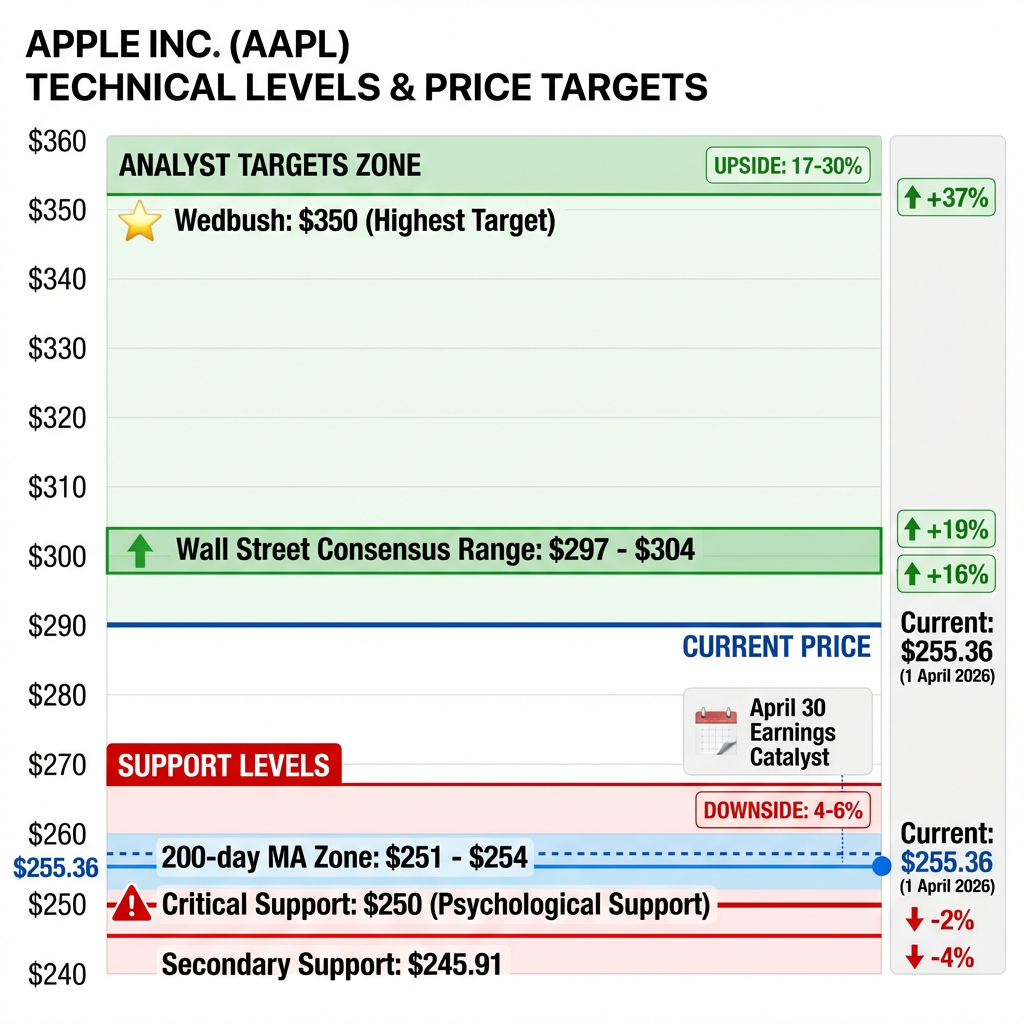

- The April 30 earnings report is the critical near-term catalyst, with $250 acting as key technical support and $255.49 resistance as the breakout trigger investors should monitor for directional confirmation.

Apple heads into its critical April 30 earnings report with momentum from a strong Q1 performance that saw shares climb 2.1% to $259 in early April. Yet the stock remains down 5.7-9% year-to-date as tariff uncertainties and China risks temper investor enthusiasm despite analyst price targets ranging from $297 to $350. The upcoming fiscal Q2 2026 results will determine whether Apple stock analysis supports the bullish thesis or validates concerns about valuation sustainability at 32x trailing earnings.

With Wall Street’s consensus implying 17-20% upside from current levels around $255, investors evaluating AAPL positions face a clear decision point. Strong iPhone demand, record upgrade intent of 37%, and accelerating AI integration support the bull case, whilst tariff exposure and execution risks frame the bear scenario. This analysis examines the metrics that matter for investment decisions ahead of the earnings catalyst.

Q1 2026 Earnings Recap: The Foundation for Bullish Momentum

Apple’s fiscal Q1 2026 results delivered a decisive beat that exceeded Wall Street’s expectations across key metrics. The company reported earnings per share of $2.84 compared to the $2.67 analyst estimate, whilst revenue growth of 15.7% year-over-year surpassed the critical 14% consensus threshold that had become the benchmark for validating the growth thesis.

China emerged as the standout performer in the quarter. Chief Executive Officer Tim Cook characterised iPhone demand as “extraordinarily high” and confirmed Apple achieved its strongest-ever iPhone quarter in the Chinese market. Revenue from China surged 38% year-over-year during fiscal Q1, which ended 27 December 2025, defying broader concerns about competitive pressure from Huawei and domestic smartphone manufacturers.

| Metric | Actual Result | Analyst Estimate |

|---|---|---|

| Earnings Per Share | $2.84 | $2.67 |

| Revenue Growth (YoY) | 15.7% | 14% |

| China Revenue Growth | 38% | Not specified |

| Stock Reaction (8 April) | +2.1% to $259 | — |

The strong Q1 performance establishes a foundation for Q2 expectations, though it also creates a higher bar for the upcoming 30 April report. Wall Street consensus projects 14% revenue growth for fiscal Q2 compared to the 15.7% achieved in Q1, suggesting analysts may again prove conservative if demand trends hold through the March quarter.

Apple’s strong showing comes amid mixed broader tech sector performance in mid-April 2026, where geopolitical developments and earnings results have created divergent paths for major technology names.

When big ASX news breaks, our subscribers know first

Understanding Apple’s Valuation: What the Numbers Mean for Investors

Apple trades at a price-to-earnings ratio of 32x trailing earnings, representing a premium valuation compared to broader market multiples. This premium reflects investor confidence in the company’s ability to sustain growth through Services expansion, AI integration, and recurring product upgrade cycles. However, maintaining this valuation multiple requires Apple to continue delivering revenue and earnings growth that justifies the price.

Why does Apple command a higher P/E ratio than the S&P 500 average? Investors are willing to pay a premium for Apple’s combination of predictable revenue streams, particularly from the high-margin Services segment, alongside substantial cash generation capabilities. The company’s brand loyalty supports pricing power that insulates margins, whilst growth optionality from AI integration and new product categories such as foldables adds to the valuation case.

What growth rate does Apple need to justify its current valuation? At a 32x earnings multiple, the market implicitly expects Apple to deliver low-to-mid teens annual earnings growth. The 15.7% revenue growth achieved in fiscal Q1 2026 supports this expectation, though Wall Street’s more conservative 12% full-year projection suggests some analysts remain cautious about sustainability beyond the immediate quarters.

For investors evaluating entry points, the critical question centres on whether Apple’s AI strategy and the iPhone 17 product cycle can sustain growth above analyst projections. If the company demonstrates AI monetisation progress and iPhone demand remains robust, the earnings multiple could expand towards the $297-$350 analyst price target range. Conversely, if growth disappoints or tariff headwinds materially impact margins, multiple compression could pressure shares below the $245-$250 technical support zone.

Investors evaluating Apple’s premium valuation should consider how the company’s AI strategy aligns with industry-wide AI integration trends, where $600 billion in infrastructure spending is reshaping technology sector growth trajectories.

Wall Street’s View: Price Targets and Analyst Ratings Breakdown

Wall Street maintains a Moderate Buy consensus on Apple stock based on 33 analyst ratings comprising 25 Buy ratings, 6 Strong Buy ratings, and only 2 Sell ratings. The consensus 12-month price target ranges from $297.58 to $304.40, representing 17-20% upside potential from current trading levels around $255.

| Analyst/Firm | Rating | Price Target | Key Thesis |

|---|---|---|---|

| Dan Ives (Wedbush) | Outperform | $350 | AI strategy execution, M5 Mac lineup, MacBook Neo innovation |

| Wamsi Mohan (Bank of America) | Buy | $320 | Q1 2026 earnings strength validates growth trajectory |

| Wall Street Consensus | Moderate Buy | $297-$304 | iPhone demand sustainability, Services segment growth |

Dan Ives of Wedbush Securities maintains the Street-high $350 price target with an Outperform rating, despite the stock experiencing an 11% decline from peak levels. His thesis centres on AI integration as an underappreciated catalyst, alongside the forthcoming M5 Mac product lineup and the MacBook Neo as innovation drivers. The $350 target implies approximately 30% upside potential if Apple successfully executes its AI roadmap and product strategy.

The 30 April earnings report represents a potential catalyst for analyst target revisions in either direction. Analysts are specifically monitoring commentary on AI monetisation timelines, China demand sustainability beyond the exceptional fiscal Q1 performance, and any management guidance addressing tariff impacts on gross margins.

Growth Catalysts: iPhone 17, AI Integration, and the Foldable Roadmap

Apple’s growth thesis for the remainder of 2026 rests on three primary catalysts with distinct timelines and risk profiles. A Morgan Stanley survey conducted 31 March revealed record 37% iPhone upgrade intent among existing users, suggesting the iPhone 17 product cycle maintains strong momentum. This survey data corroborates early demand reports that drove shares up 2.1% to $259 in early April and supports analyst projections for sustained revenue growth.

> iPhone sales in China rose 23% in early 2026, according to available sales data. Apple now commands 22% market share in China, demonstrating competitive resilience against Huawei and domestic rivals despite intensifying local competition.

Apple now commands 22% market share in China according to smartphone market research from Canalys, demonstrating competitive resilience against Huawei and domestic rivals despite intensifying local competition.

Investors should monitor five specific catalysts that could determine whether Apple reaches analyst price targets or tests lower support levels:

- iPhone 17 demand sustainability through fiscal Q2 and the critical holiday 2026 selling season

- Siri AI upgrades featuring multi-command capabilities and competitive positioning against AI assistant competitors

- September 2026 foldable iPhone launch potentially expanding Apple’s presence in the premium smartphone segment

- M5 Mac and MacBook Neo releases adding hardware refresh cycles to the product roadmap

- Services segment growth maintaining its high-margin contribution trajectory

Bloomberg confirms Apple remains on track for a September 2026 foldable iPhone launch, though engineering challenges related to hinge durability and display crease management are being actively addressed in testing. Success in bringing a foldable device to market could open a new premium product category, whilst delays or quality compromises could disappoint investors who have priced in innovation optionality.

Risk Factors: Tariffs, China Exposure, and Execution Challenges

Financial experts flag tariff uncertainty as Apple’s primary near-term risk given the company’s China-concentrated supply chain. Potential tariff escalation could pressure gross margins, complicate production logistics, and force difficult decisions on pricing strategy that might impact demand elasticity in price-sensitive markets.

While Apple faces significant tariff exposure through its China manufacturing base, understanding how other multinational corporations have navigated tariff exemptions illustrates the range of possible policy outcomes across different industries.

The U.S. Trade Representative’s Section 301 tariff framework under ongoing review directly impacts technology companies with China-based supply chains, creating regulatory uncertainty for margin forecasting and production planning.

Key risk factors investors should weigh against the bullish catalysts include:

- Tariff and trade policy risk: China supply chain concentration creates direct exposure to escalating trade tensions between the United States and China, with potential margin compression if cost increases cannot be passed through to consumers

- China demand sustainability: Despite the exceptional 38% revenue growth in fiscal Q1, ongoing local competition from Huawei and evolving economic conditions in China pose risks to maintaining market share and pricing power

- AI execution pressure: The 32x valuation multiple requires tangible AI monetisation progress and differentiation versus competitors, making execution on Siri upgrades and AI integration critical

- Foldable development risk: Engineering challenges with hinge and crease durability could delay the September 2026 launch target or compromise product quality, disappointing investors expecting innovation momentum

- Macro and sector headwinds: Magnificent 7 technology stock volatility and broader risk-off sentiment have contributed to the 5.7-9% year-to-date decline despite company-specific fundamental strength

Apple’s year-to-date decline of 5.7-9% reflects sector volatility, yet market resilience patterns following geopolitical shocks demonstrate how equities can recover sharply even after significant drawdowns driven by external events.

If these risks materialise through tariff escalation, China demand weakness, or AI development disappointments, the $250 price level becomes critical as both a psychological and technical support zone. A sustained break below $250 could trigger further selling pressure towards the $245.91 secondary support level, representing 4-6% downside from current trading levels around $255.

The next major ASX story will hit our subscribers first

Technical Analysis: Key Levels to Watch Before and After Earnings

Apple trades at approximately $255 as of 1 April 2026, testing resistance near $255.49 after rebounding from the 200-day moving average support zone between $251-$254. The stock has exhibited a sideways-to-slightly bullish pattern in early April following a bearish start to the week, with technical indicators suggesting potential for either direction depending on the 30 April earnings catalyst.

| Technical Level | Price | Significance |

|---|---|---|

| Current Price (1 April) | $255.36 | Reference point for risk-reward assessment |

| Near-Term Resistance | $255.49 | Breakout trigger above this level confirms bullish momentum |

| 200-Day Moving Average | $251-$254 | Trend support providing technical floor |

| Critical Support | $250 | Psychological and technical level; break signals potential weakness |

| Secondary Support | $245.91 | Next downside target if $250 level fails |

Elevated trading volume on up days indicates institutional accumulation patterns, suggesting larger investors are positioning ahead of the earnings report. This volume characteristic typically signals confidence in an upcoming catalyst, though it does not guarantee positive price action following the 30 April results.

For investors considering positions ahead of earnings, the $250 level represents a logical stop-loss zone for risk management, whilst $255.49 resistance offers a potential breakout entry trigger if the stock confirms bullish momentum. A post-earnings move above $260 would likely confirm renewed buying interest and support a technical path towards the $297-$304 analyst target range.

The Investment Case: Weighing Opportunity Against Risk

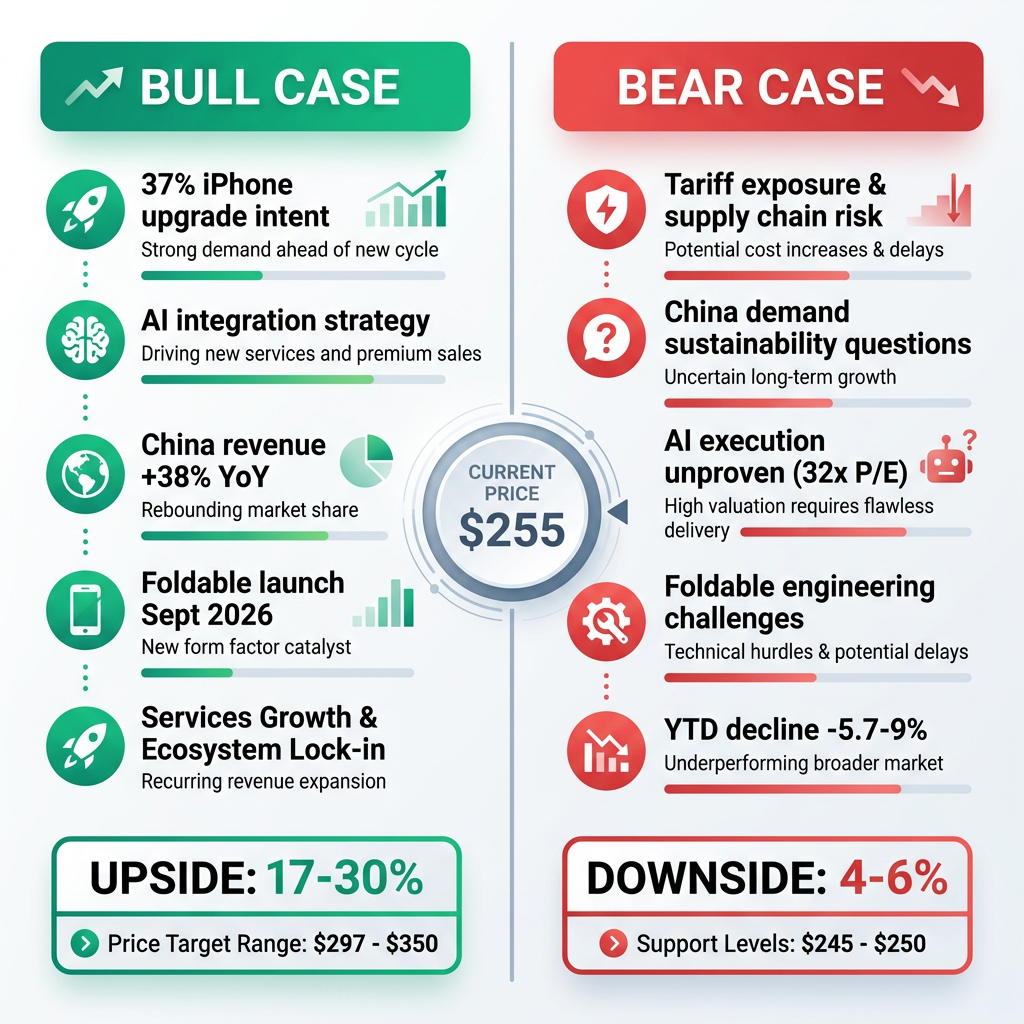

Apple’s fiscal Q1 2026 earnings beat, record 37% iPhone upgrade intent, and exceptional 38% China revenue growth validate the growth thesis supporting analyst price targets of $297-$350. For investors willing to accept tariff uncertainty and AI execution risk, the 17-30% upside potential to analyst targets compares favourably to the 4-6% downside risk to the $245-$250 technical support zone.

Bull Case: Q1 earnings beat demonstrates Apple can exceed conservative analyst projections. Record 37% upgrade intent supports sustained iPhone 17 demand through 2026. AI integration strategy, including Siri multi-command capabilities and increased AI hiring, positions Apple for new revenue streams. Foldable iPhone launch in September 2026 expands total addressable market in premium segment. Analyst targets of $297-$350 imply 17-30% upside from current $255 levels.

Bear Case: Escalating tariffs targeting China supply chain could pressure gross margins and complicate production. China revenue growth of 38% in fiscal Q1 may prove unsustainable amid local competition and economic headwinds. AI monetisation progress remains unproven, creating risk that 32x valuation multiple compresses if execution disappoints. Engineering challenges with foldable iPhone hinge and crease durability could delay September launch or compromise product quality. Year-to-date decline of 5.7-9% reflects ongoing sector volatility that could persist.

The 30 April earnings report will provide critical data on fiscal Q2 demand trends, commentary on China market sustainability, and management guidance addressing tariff impacts on margins. Investors may choose to establish positions ahead of earnings with appropriate risk management using the $250 support level as a stop-loss reference, or alternatively wait for post-earnings clarity before committing capital.

Regardless of entry timing, investors should monitor iPhone 17 demand data from supply chain reports, AI integration announcements and Siri upgrade progress, tariff policy developments affecting China manufacturing, and engineering progress towards the September 2026 foldable launch. These factors will determine whether Apple reaches the $297-$350 analyst target range or tests lower support levels through the remainder of 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

What is Apple's current stock valuation and is it overpriced?

Apple trades at 32x trailing earnings, a premium to broader market multiples that reflects investor confidence in Services growth, AI integration, and recurring iPhone upgrade cycles. Whether this valuation is justified depends on whether Apple continues delivering low-to-mid teens annual earnings growth, which its 15.7% Q1 2026 revenue growth supports.

What are analysts predicting for Apple stock in 2026?

Wall Street maintains a Moderate Buy consensus on Apple with 33 analyst ratings, including 25 Buy and 6 Strong Buy ratings, and a consensus 12-month price target of $297-$304, representing 17-20% upside from current levels around $255. Wedbush analyst Dan Ives holds the Street-high target of $350, citing AI strategy execution and the upcoming M5 Mac lineup.

How do tariffs affect Apple stock and its earnings outlook?

Apple's China-concentrated supply chain creates direct exposure to U.S.-China trade tensions, with potential tariff escalation risking gross margin compression and production complications. Investors are watching the April 30 earnings call closely for management commentary on how tariff impacts are being managed and whether cost increases can be passed through to consumers.

What key levels should investors watch for Apple stock before earnings?

Apple is testing near-term resistance at $255.49 with critical technical support at $250, which analysts identify as the key stop-loss reference zone for risk management. A post-earnings move above $260 would likely confirm renewed buying interest and open a technical path toward the $297-$304 consensus price target range.

What catalysts could drive Apple stock higher in the second half of 2026?

The five primary catalysts analysts are monitoring include iPhone 17 demand sustainability, Siri AI upgrades with multi-command capabilities, a September 2026 foldable iPhone launch, M5 Mac and MacBook Neo product releases, and continued high-margin Services segment growth. A record 37% iPhone upgrade intent among existing users, per a Morgan Stanley survey, supports the near-term demand outlook.