Alstom Stock Crashes 28% as €1.5B Cash Flow Target Withdrawn

Key Takeaways

- Alstom shares fell approximately 28% on 17 April 2026, hitting an intraday low of €16.33 after the company withdrew its €1.5 billion medium-term free cash flow target.

- The preliminary FY2025/26 EBIT margin of approximately 6% missed the 7% guidance target, while the expected €1.5 billion H1 cash outflow nearly tripled analyst forecasts of €560 million.

- Despite a record €100 billion backlog, strong order intake, and a 1.4x book-to-bill ratio, persistent execution failures in rolling stock programmes are preventing Alstom from converting demand into cash.

- Jefferies analysts warned that project execution problems are undermining the central investment thesis and that the margin for error is narrowing significantly, with potential downgrades possible if execution does not improve.

- A PEG ratio of 0.18 suggests deep undervaluation, but investors must weigh whether current prices compensate for execution risk or whether Bombardier integration challenges represent a structurally impaired profitability outlook.

Alstom SA shares crashed approximately 28% on 17 April 2026, hitting an intraday low of €16.33, the lowest level since mid-2024. The French rail equipment manufacturer withdrew its €1.5 billion medium-term free cash flow target and revealed preliminary fiscal 2025/26 results that missed margin guidance, triggering the steepest single-day decline since 2024.

The company announced an adjusted EBIT margin of approximately 6% versus its 7% guidance target, alongside an expected €1.5 billion cash outflow in H1 FY2025/26 compared to analyst expectations of €560 million. Pre-market trader estimates had anticipated a 10-15% drop, but the actual decline nearly doubled those forecasts, signalling that the severity of the guidance withdrawal exceeded what the market had priced in.

> Key Figures at a Glance

> – Stock fell from €22.84 to €16.33 (28.5% decline)

> – €1.5 billion cumulative FCF target withdrawn

> – €1.5 billion expected H1 cash outflow vs €560 million analyst forecast

> – EBIT margin 6% vs 7% target

Trading activity reflected sharp investor reaction to execution failures in rolling stock programmes, with the magnitude of the sell-off indicating that the guidance cut represented a more severe setback than anticipated. The collapse marks Alstom’s worst trading day since mid-2024, when similar operational challenges triggered significant market concern.

Understanding free cash flow guidance and why it matters for Alstom

Free cash flow represents the cash a company generates after paying for operations and capital expenditures. For capital-intensive industrial companies like Alstom, this metric is critical because it measures the money available for debt reduction, shareholder returns, or strategic investments.

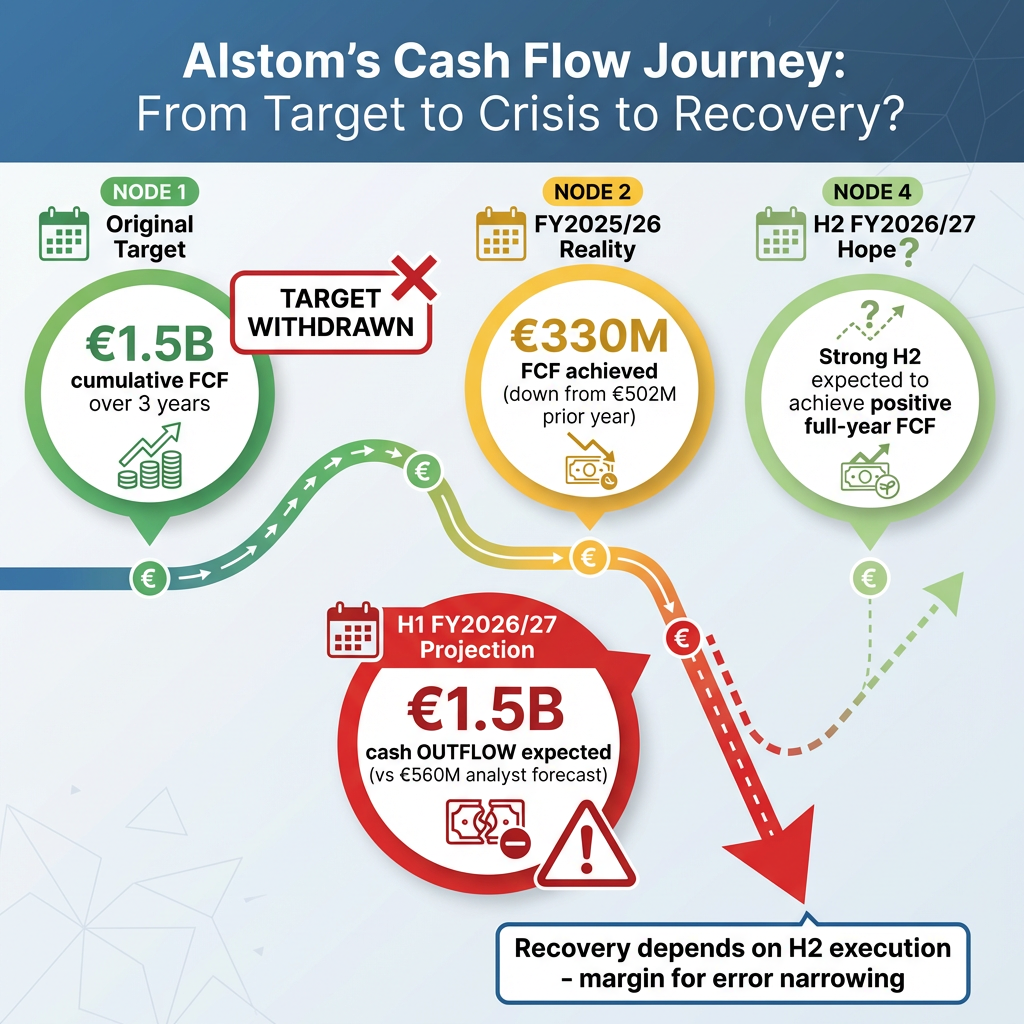

Alstom carries substantial debt from its 2021 acquisition of Bombardier Transportation. The €1.5 billion cumulative FCF target over three years was designed to demonstrate that the company could convert its massive order backlog into actual cash, reducing leverage and proving the integration was succeeding. Withdrawing this target removes a key credibility benchmark that investors had relied upon to assess management’s execution capability.

Alstom has an impressive €100 billion backlog, but orders don’t equal cash. Complex rail projects often require significant upfront investment in inventory, research and development, and production before payments arrive. The gap between booking orders and generating cash is precisely what’s concerning investors today, as the preliminary results reveal that execution challenges are preventing the company from converting its order book into positive cash flow within expected timeframes.

Understanding how companies execute free cashflow turnarounds after periods of operational difficulty can provide useful perspective on the recovery pathways available to capital-intensive businesses facing execution challenges.

Harvard Business Review’s research on cash flow as the primary measure of operational efficiency in capital-intensive industries demonstrates why investors prioritize actual cash generation over accounting profits when evaluating companies with large project backlogs.

When big ASX news breaks, our subscribers know first

Breaking down the fiscal 2025/26 results: margin miss and execution failures

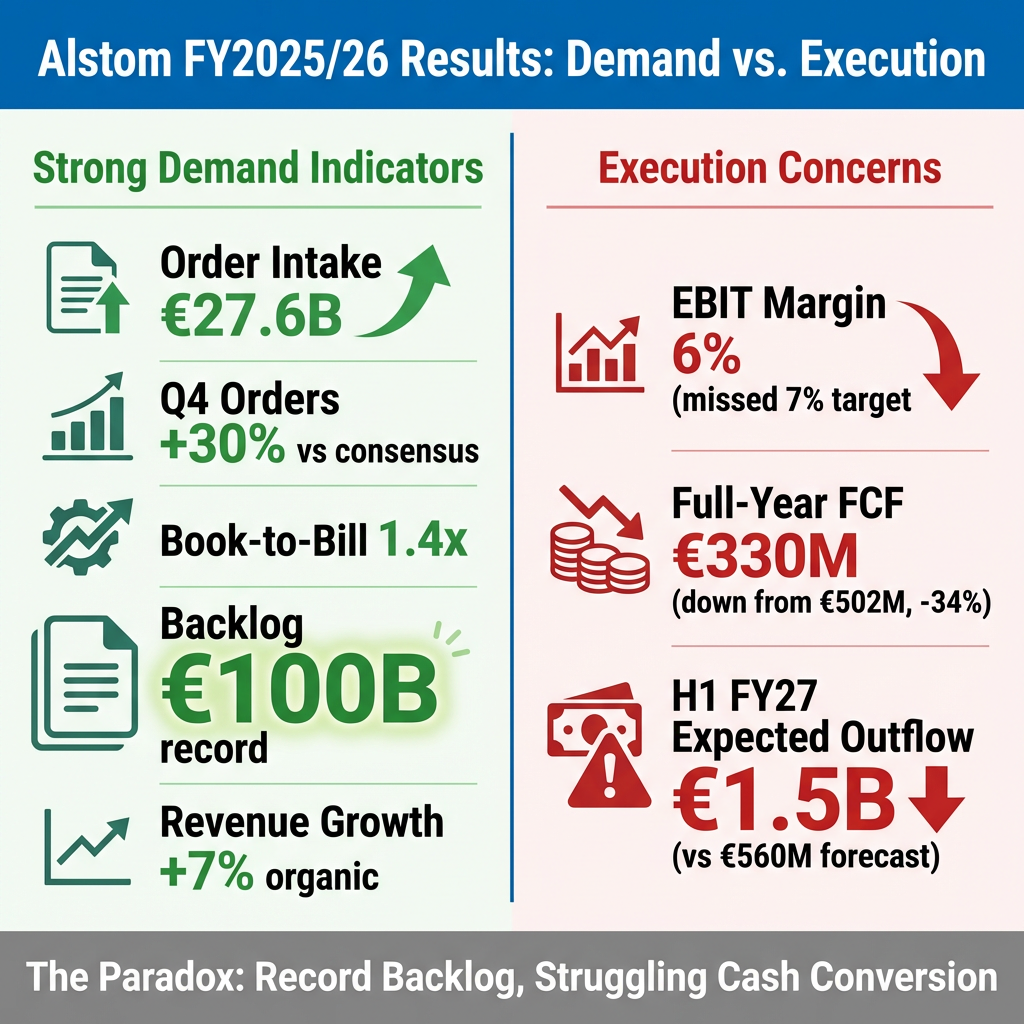

The preliminary results present a mixed picture. Order intake of €27.6 billion, Q4 orders 30% above consensus, revenue growth of 7% organically, and a record €100 billion backlog all exceeded expectations. However, the adjusted EBIT margin of approximately 6% missed the 7% target by 100 basis points, attributed to project execution challenges and slower production ramp-ups in rolling stock programmes.

The €330 million full-year FCF, down from €502 million in the prior year, and expected €1.5 billion H1 outflow reveal severe cash generation problems. The company’s strong demand indicators contrast sharply with its operational execution, creating a disconnect that has eroded investor confidence.

The magnitude of guidance cuts and earnings revisions can provide important context for understanding how markets react to operational setbacks across different industrial sectors, particularly when execution challenges emerge unexpectedly.

| Metric | Actual Result | Expectation/Prior | Assessment |

|---|---|---|---|

| Order Intake | €27.6B | Strong performance | Positive |

| Q4 Orders | €7.6B | 30% above consensus | Positive |

| Book-to-Bill | 1.4x | Healthy demand | Positive |

| Backlog | €100B record | Multi-year visibility | Positive |

| Revenue Growth | 7% organic | Beat forecasts | Positive |

| EBIT Margin | 6% | Missed 7% target | Concerning |

| Full-Year FCF | €330M | Down from €502M | Concerning |

| H1 FY27 FCF | €1.5B outflow | vs €560M expected | Concerning |

The root causes of the execution failures include project delays in rolling stock programmes, higher research and development costs, inventory buildup creating cash strain, and slower-than-expected production ramp-ups. These issues connect to the Bombardier integration legacy that continues to create operational challenges, with the acquisition completed in early 2021 now representing a five-year integration period that has yet to deliver the expected synergies.

The execution challenges stemming from rail infrastructure acquisitions and integration challenges highlight the operational complexity of integrating large-scale purchases in capital-intensive transport sectors, particularly when legacy systems and production ramps require careful coordination.

Specific execution problems identified include:

- Rolling stock programme delays creating cost overruns

- Higher R&D costs compressing margins

- Inventory buildup straining working capital

- Production ramp-up timelines extending beyond plan

- Legacy integration issues from Bombardier acquisition

Fiscal 2026/27 outlook: below-consensus guidance extends recovery timeline

Beyond the disappointing FY2025/26 results, the forward guidance for FY2026/27 also missed analyst expectations across key metrics. This extends the investment timeline and reduces visibility on when Alstom will achieve its medium-term profitability targets.

Alstom’s FY2026/27 guidance projects approximately 5% organic revenue growth versus 5.4% consensus, 6.5% EBIT margin versus 7.1% consensus, and positive but unquantified free cash flow with negative H1 and strong H2. The CFO indicated net debt will remain stable or increase modestly, signalling that deleveraging is also delayed.

> FY2026/27 Guidance vs Analyst Consensus

> – Organic Revenue Growth: Alstom ~5% vs Consensus 5.4%

> – EBIT Margin: Alstom 6.5% vs Consensus 7.1%

> – Free Cash Flow: Positive but unquantified vs Expected specific target

> – Net Debt: Stable or increasing vs Expected reduction

The 8-10% medium-term EBIT margin target will not be achieved in FY2026/27, pushing the recovery timeline further out. The CFO’s acknowledgement that net debt may increase modestly signals that deleveraging, a key investor expectation, is also delayed. The company expects negative H1 FCF followed by strong H2 cash generation, creating another period of uncertainty that investors must navigate before determining whether the recovery thesis remains intact.

Analyst reaction and investment thesis under pressure

Jefferies analysts, led by Lucas Ferhani, characterised the update as “disappointing”, noting that while order demand remains robust with a growing backlog at improved margins, execution problems are undermining the central element of the investment thesis. Their immediate commentary provided the clearest professional assessment available in the hours following the announcement.

> “Project execution problems are undermining free cash flow progress—the central element of the investment thesis.”

> Jefferies analysts

Jefferies believes the balance sheet can absorb near-term FCF weakness, including the substantial €1.5 billion H1 outflow, but cautioned that “the margin for error is narrowing significantly”. This framing captures the core tension: strong demand versus weak execution, with diminishing room for further setbacks. Another execution miss or guidance cut could create more serious financial stress, potentially triggering credit rating reviews or covenant concerns.

Formal rating changes and price target revisions have not yet been issued in the immediate aftermath, as analysts process the full implications of the guidance withdrawal. However, the framing around “investment thesis under pressure” suggests downgrades are possible if execution doesn’t improve through the next two quarters.

Valuation and long-term considerations for investors

At current prices following the 28% decline, Alstom trades at a PEG ratio of 0.18, suggesting significant undervaluation relative to growth expectations. The market cap of approximately $12.4 billion compares favourably to a €100 billion backlog that provides multi-year revenue visibility. The 1.4x book-to-bill ratio demonstrates continued strong demand for rail equipment globally, with European infrastructure investment focus supporting long-term sector fundamentals.

UNIFE’s World Rail Market Study forecasting 2.7% annual growth through 2027 confirms that European rail infrastructure investment remains robust, driven by decarbonization policies and fleet modernization programmes across major economies.

> Investment Case: Pros and Cons

>

> Potential Opportunities:

> – Deep undervaluation on PEG basis (0.18)

> – Record €100 billion backlog for revenue visibility

> – Strong demand with 1.4x book-to-bill

> – European rail sector benefits from infrastructure investment

> – Production ramps in H2 could drive cash recovery

>

> Key Risks:

> – FCF guidance withdrawal removes credibility benchmark

> – Bombardier integration issues persist five years post-deal

> – Margin expansion timeline extended beyond FY2026/27

> – €1.5B H1 cash outflow creates near-term pressure

> – Management track record on targets is weakening

Undervaluation only matters if the company can execute, and execution is precisely what’s in question. The Bombardier acquisition closed in early 2021, and integration challenges continue to create margin and cash flow pressure five years later. Investors must weigh whether current prices adequately compensate for execution risk or whether this represents a value trap with structurally impaired profitability that may take years to resolve.

The next major ASX story will hit our subscribers first

What to watch: key metrics and catalysts ahead

With significant uncertainty following the announcement, investors need clear metrics to monitor. The company’s guidance creates specific checkpoints that will either rebuild or further erode confidence in management’s ability to execute its recovery plan.

Priority monitoring items include:

- H2 FY2026/27 free cash flow: The company is betting on a strong second half to achieve positive full-year FCF, making this the critical near-term test of whether production ramps materialise as planned.

- Quarterly EBIT margin progression toward 6.5% target: Incremental improvement would demonstrate execution is stabilising, whilst further deterioration would signal deeper structural problems.

- Rolling stock programme updates: Any news on delivery timelines and cost performance for specific contracts will provide early signals on whether execution challenges are being resolved.

- Net debt trajectory: The CFO indicated stable or modest increase, but investors should watch for worse outcomes that could trigger credit rating reviews.

- Order book quality: Continued strong intake at improving margins would support the demand thesis, whilst order cancellations or margin pressure on new contracts would be concerning.

- Analyst rating actions and price target revisions: Professional assessment will crystallise over coming weeks as analysts digest full-year results and management commentary.

The stakes are clear: if H2 cash generation disappoints, the margin for error that Jefferies warned about will shrink further, potentially creating more serious financial stress. Conversely, strong execution through calendar year 2026 could begin restoring confidence in management’s ability to convert the substantial order backlog into cash. The next two quarters will be decisive for determining whether the 17 April crash represents a buying opportunity or the beginning of a deeper derating.

Frequently Asked Questions About Alstom’s Stock Decline

Why did Alstom stock drop 28% on 17 April 2026?

Alstom’s shares crashed following three simultaneous triggers: withdrawal of the €1.5 billion medium-term free cash flow target, preliminary FY2025/26 EBIT margin of approximately 6% missing 7% guidance, and expected €1.5 billion cash outflow in H1 FY2026/27 versus analyst expectations of €560 million. The severity of the decline exceeded pre-market trader estimates of 10-15%, indicating the guidance cut shocked even prepared investors.

Is Alstom stock a buy after the crash?

The investment case presents balanced considerations. A PEG ratio of 0.18 and €100 billion backlog suggest undervaluation, whilst the 1.4x book-to-bill ratio demonstrates continued demand. However, execution concerns are real, with Jefferies analysts warning that “the margin for error is narrowing significantly”. Whether this represents opportunity or value trap depends on investor risk tolerance and timeline. Long-term thesis remains intact if execution improves, but near-term uncertainty is elevated.

What is Alstom’s outlook for fiscal 2026/27?

Alstom’s guidance projects approximately 5% organic revenue growth, 6.5% EBIT margin, and positive full-year free cash flow with negative H1 and strong H2. All metrics fall below analyst consensus expectations. The CFO indicated net debt will remain stable or increase modestly, and the 8-10% medium-term margin target is delayed beyond FY2026/27, extending the recovery timeline.

Is Alstom’s problem company-specific or industry-wide?

The issues appear company-specific, tied to Bombardier integration legacy and rolling stock programme execution challenges. European rail sector fundamentals remain strong with continued infrastructure investment focus. Competitors like Siemens Mobility and Stadler Rail have not reported similar cash flow or margin challenges, suggesting Alstom’s operational difficulties are not reflective of broader sector trends.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

Why did Alstom stock drop 28% on 17 April 2026?

Alstom shares crashed after the company simultaneously withdrew its €1.5 billion medium-term free cash flow target, reported a preliminary EBIT margin of approximately 6% against a 7% guidance target, and revealed an expected €1.5 billion H1 cash outflow versus analyst forecasts of just €560 million — a triple negative shock that exceeded pre-market trader estimates of a 10–15% decline.

What is free cash flow and why does it matter for Alstom investors?

Free cash flow is the cash a company generates after covering operating costs and capital expenditure, and for Alstom it is the critical metric investors use to assess whether its €100 billion order backlog is converting into real financial returns and whether the company can reduce its substantial debt from the 2021 Bombardier acquisition.

Is Alstom stock a buy after the crash?

Alstom trades at a PEG ratio of 0.18 with a record €100 billion backlog and a 1.4x book-to-bill ratio suggesting strong demand, but Jefferies analysts warn that 'the margin for error is narrowing significantly' due to persistent execution failures — making the risk-reward dependent on whether management can deliver promised H2 cash generation improvements.

What is Alstom's financial guidance for fiscal 2026/27?

Alstom guided for approximately 5% organic revenue growth, a 6.5% EBIT margin, and positive full-year free cash flow with a negative first half followed by a strong second half — all metrics below analyst consensus, with the CFO indicating net debt will remain stable or increase modestly and the 8–10% medium-term margin target pushed beyond FY2026/27.

What are the key metrics investors should monitor following Alstom's guidance withdrawal?

Investors should closely track H2 FY2026/27 free cash flow delivery, quarterly EBIT margin progression toward the 6.5% target, rolling stock programme execution updates, net debt trajectory, and any analyst rating changes — as these checkpoints will determine whether the April crash represents a buying opportunity or the start of a deeper derating.