NAB Shares Near 52-Week Low: Value Play or Value Trap?

34 mins ago

Citi has identified seven stocks as the clearest equity plays on China’s national data centre programme, splitting them across two categories with distinct risk and timing profiles. Two of those names, GDS Holdings and VNET Group, have already posted record bookings in Q1 2026, figures the bank says confirm that policy is translating into real commercial activity. The framework, reported via Investing.com, gives investors a structured entry point into a multi-year, state-driven infrastructure cycle that spans data centre operators, AI server manufacturers, optical component makers, and software services providers. What follows profiles all seven stocks Citi flagged, explains the two-category logic underpinning the recommendations, and identifies the specific data points and watch variables that matter for each position.

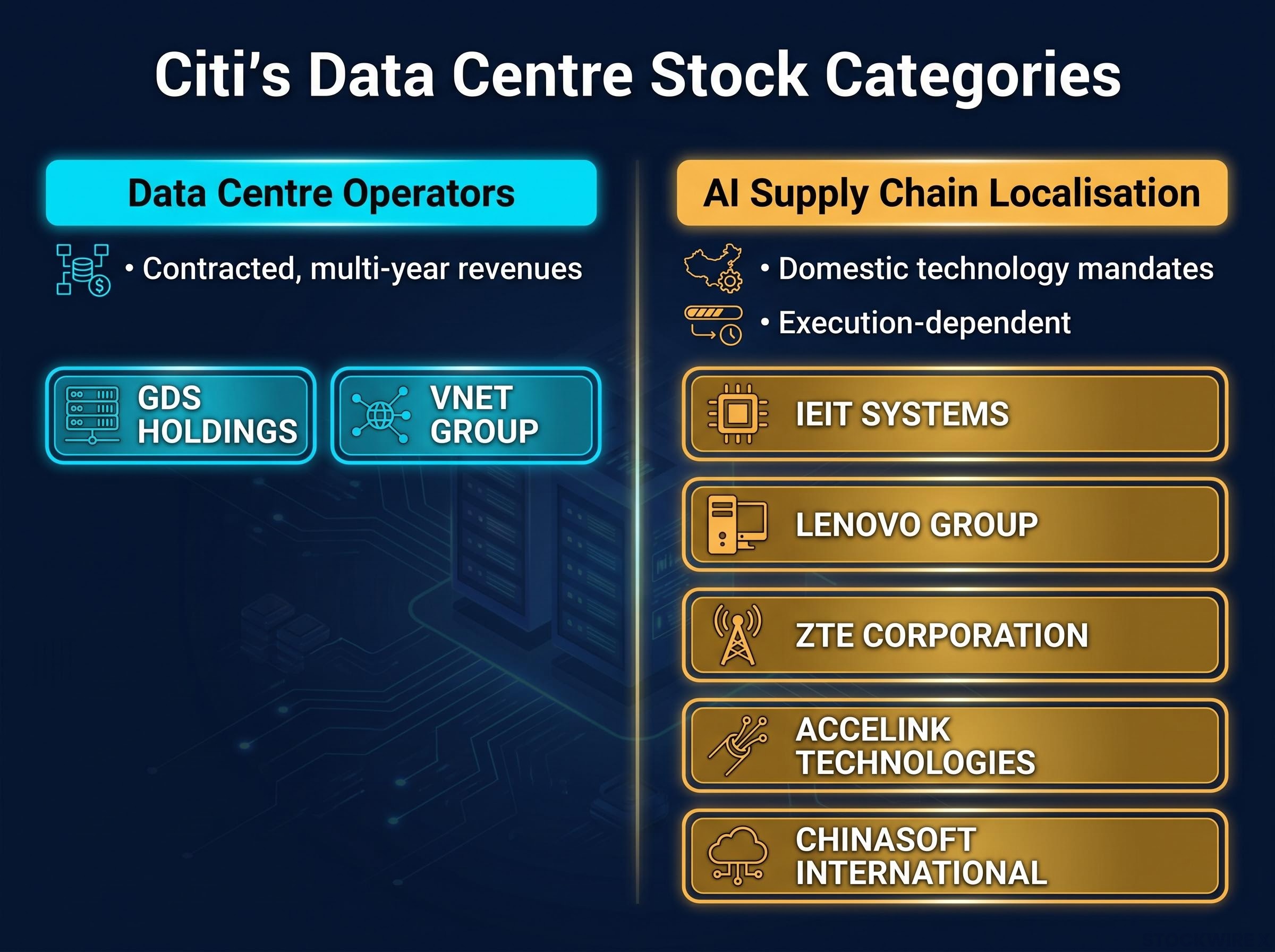

Citi’s framework rests on a distinction that changes how each stock should be evaluated. The bank separates beneficiaries into data centre operators and AI supply chain localisation beneficiaries, reflecting materially different demand timing and risk structures.

Understanding which category a name belongs to is the prerequisite for assessing its timeline and risk. Treating all seven as interchangeable infrastructure plays would be a misread of the framework.

| Category | Company | Role |

|---|---|---|

| Data Centre Operators | GDS Holdings | Hyperscale data centre operator |

| Data Centre Operators | VNET Group | Retail and wholesale data centre operator |

| AI Supply Chain Localisation | IEIT Systems | Domestic AI server manufacturer |

| AI Supply Chain Localisation | Lenovo Group | Diversified infrastructure solutions provider |

| AI Supply Chain Localisation | ZTE Corporation | AI server and data centre networking supplier |

| AI Supply Chain Localisation | Accelink Technologies | Optical transceiver manufacturer |

| AI Supply Chain Localisation | Chinasoft International | Software and IT services partner to Huawei |

The operator thesis is grounded in numbers, not policy projections. Both GDS and VNET posted record booking quarters in Q1 2026, and Citi’s reading is that these figures confirm an existing demand acceleration rather than a one-off event driven by programme announcements.

The record bookings at GDS and VNET sit within a broader surge in global AI capital expenditure, with the four largest US hyperscalers collectively committing approximately $725 billion in 2026 alone, a spending trajectory that is pulling forward data centre capacity demand across multiple geographies simultaneously.

Q1 2026 Booking Comparison GDS Holdings: approximately 200 megawatts of new wholesale bookings (record quarter). VNET Group: in excess of 500 megawatts in new orders (record quarter). Combined, these bookings represent contracted future revenue that will compound over multiple years as capacity is built and brought online.

GDS recorded approximately 200 megawatts of new wholesale bookings in Q1 2026. At wholesale scale, these leases typically represent multi-year commitments from top-tier cloud tenants, creating durable contracted revenue.

Citi noted that GDS had already been capturing accelerating demand momentum before the programme’s formal rollout, meaning the national initiative acts as a force multiplier on an existing upcycle. The watch variable is GDS’s capacity mix: how new builds split between domestic AI workloads and broader enterprise use will influence long-term pricing power and capital expenditure requirements.

VNET secured in excess of 500 megawatts in new orders during the same period. The company operates a mixed retail and wholesale model across core urban markets.

As with GDS, VNET’s bookings were already inflecting higher before the programme launched. The key concern is different, however. VNET has historically operated with higher leverage than some peers, and as demand for new capacity accelerates, balance sheet fitness and financing costs become as material as the top-line booking figures themselves.

The China data centre programme provides a live case for a framework that applies well beyond this single theme. Whether evaluating state-backed programmes in energy, transport, or defence, the same analytical steps apply.

The programme’s stated five-year horizon is a planning guide, not a guaranteed backlog. Government mandates that create demand can also be delayed, redefined, or reprioritised.

China’s programme explicitly embeds domestic technology mandates designed to reduce reliance on foreign semiconductor and technology supply chains. Citi identifies five companies across servers, networking, and software as proxies for the localised AI ecosystem. Each occupies a different layer of the data centre stack.

China’s $295 billion AI buildout plan targets domestic suppliers for 80% of technology procurement, including AI chips, which is the policy foundation that transforms localisation mandates from regulatory guidance into a guaranteed addressable market for the five supply chain names Citi identifies.

The domestic chip mandate underpinning IEIT’s investment thesis is partly a consequence of Nvidia’s near-total exit from the Chinese AI accelerator market, with Huawei Ascend now holding an estimated 70-80% share and creating structural procurement demand for local server manufacturers built around non-US silicon.

No state-driven infrastructure thesis is without structural risks, and investors who enter these positions without accounting for them face foreseeable volatility.

U.S.-China technology tensions remain structurally durable regardless of bilateral trade progress because AI chip export controls are grounded in national security law with bipartisan Congressional backing, placing them outside the jurisdiction of trade negotiators and keeping ZTE’s regulatory exposure elevated even in optimistic diplomatic scenarios.

The stated five-year programme horizon is a planning guide, not a guaranteed backlog. Policy risk applies across both categories.

The combination of record operator bookings in Q1 2026 (GDS at 200 megawatts, VNET at over 500 megawatts) and embedded domestic localisation mandates means the China data centre programme has moved from policy aspiration to observable commercial activity across multiple value chain layers.

Citi’s two-category structure is itself a signal of the programme’s maturity. The ability to segment the opportunity by timing and risk reflects enough on-the-ground data to make category-level distinctions, a development that was not available when the programme sat at the announcement stage.

The five supply chain names function collectively as a localised ecosystem proxy, benefiting from structural demand ring-fencing that limits foreign competition across servers, networking, and software. For investors, this framework offers both a specific watchlist and a transferable method for evaluating future state-backed infrastructure cycles.

For investors wanting to apply this value chain framework beyond China’s national programme, our deep-dive into AI supply chain investing maps where profit is genuinely concentrated across semiconductors, foundries, cloud operators, and software globally, including analysis of how legacy application software multiples are diverging sharply from AI-native valuations.

This article is based on Citi’s research as reported by Investing.com. It is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Citi identified seven China data center stocks: GDS Holdings and VNET Group as data centre operators, and IEIT Systems, Lenovo Group, ZTE Corporation, Accelink Technologies, and Chinasoft International as AI supply chain localisation beneficiaries.

Data centre operators like GDS and VNET generate contracted, multi-year revenues from leases with hyperscalers and enterprises, offering higher near-term revenue visibility, while supply chain localisation names depend on domestic technology mandates and production ramp-ups, representing a longer-horizon opportunity with more execution risk.

GDS Holdings recorded approximately 200 megawatts of new wholesale bookings in Q1 2026, while VNET Group secured in excess of 500 megawatts in new orders, both representing record quarters that Citi views as confirmation of sustained demand acceleration.

Key risks include policy execution delays that could slow the programme's five-year timeline, timing divergence between operator and supply chain categories, and geopolitical or regulatory risk, particularly for ZTE given its prior history with US export restrictions.

China's programme targets domestic suppliers for 80% of technology procurement, creating a policy-backed addressable market for local server manufacturers like IEIT Systems and software partners like Chinasoft International by ring-fencing demand away from foreign competitors.