Why Super’s 8% Returns Are a Trap for Retirement Planning

12 hrs ago

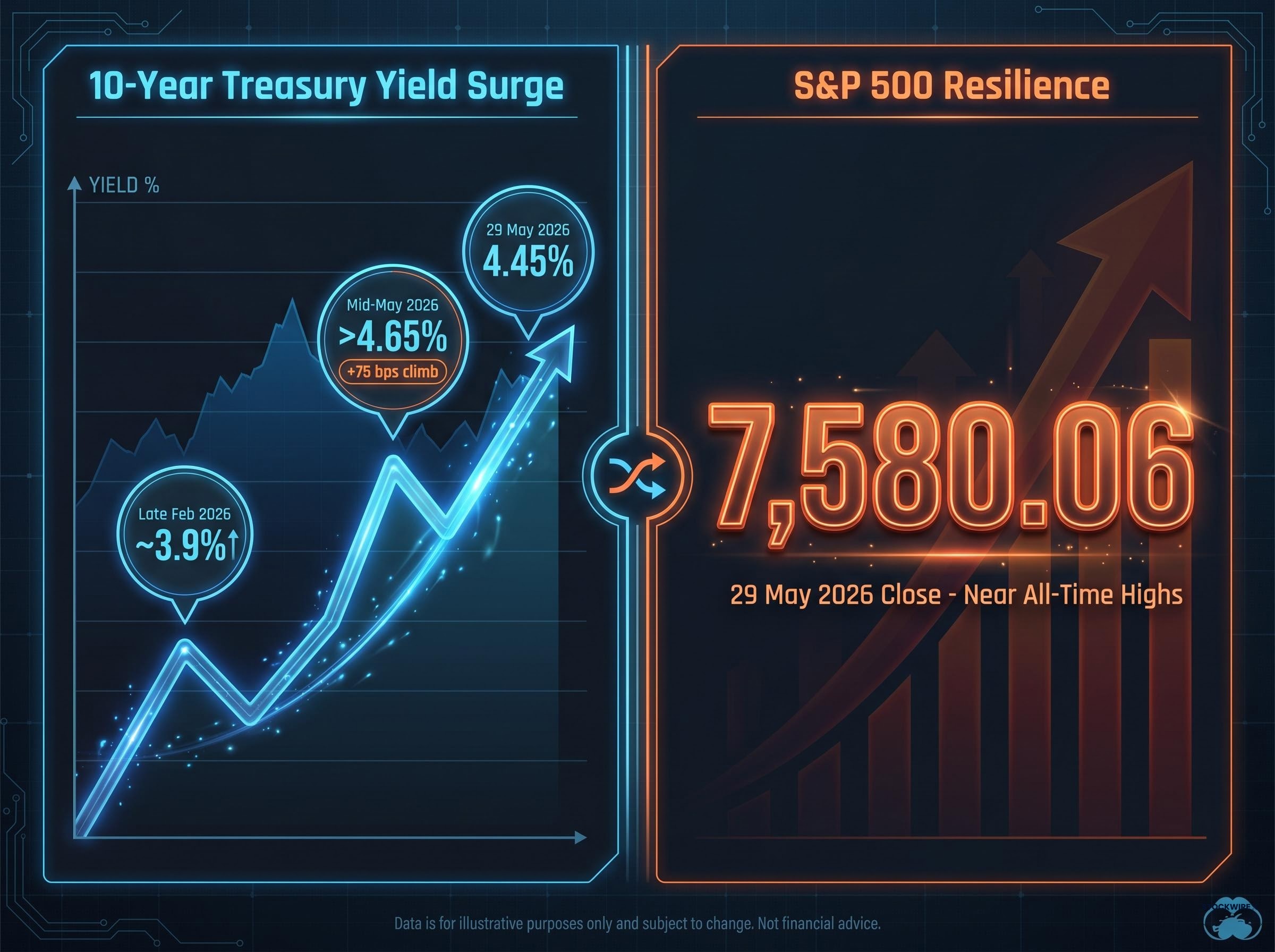

The 10-year U.S. Treasury yield climbed more than 75 basis points in roughly ten weeks, surging from approximately 3.9% in late February 2026 to above 4.65% by mid-May, yet the S&P 500 closed 29 May at 7,580.06, near all-time highs. For anyone who learned that rising Treasury yields hurt stocks, the market appears to be breaking its own rules.

The conventional inverse relationship between bond yields and equity prices is grounded in real mechanics, and those mechanics have not disappeared. What has changed is the specific combination of forces on the other side of the ledger: corporate earnings outperforming expectations, a labour market that continues to add jobs, and a concentrated wave of AI-driven capital expenditure lifting the index’s most heavily weighted names. Understanding why this moment is different also reveals exactly what could make it stop being different.

This article explains the mechanics of how rising yields normally pressure equities, then walks through each of the three forces that have allowed the S&P 500 to defy that pressure in 2026. It closes with the conditions that would end the defiance.

The numbers are difficult to reconcile at first glance. Between late February and mid-May 2026, the 10-year Treasury yield rose from approximately 3.9% to above 4.65%, a move of a magnitude that has historically forced equity markets to reprice.

The 75-basis-point climb in roughly ten weeks represents one of the sharpest yield surges of the post-pandemic era.

By 29 May, the yield had pulled back to 4.45%, still significantly elevated versus its late-February starting point. The S&P 500, meanwhile, printed 7,580.06 on the same day, sitting near all-time highs as if the bond market had been speaking a language equities chose not to hear.

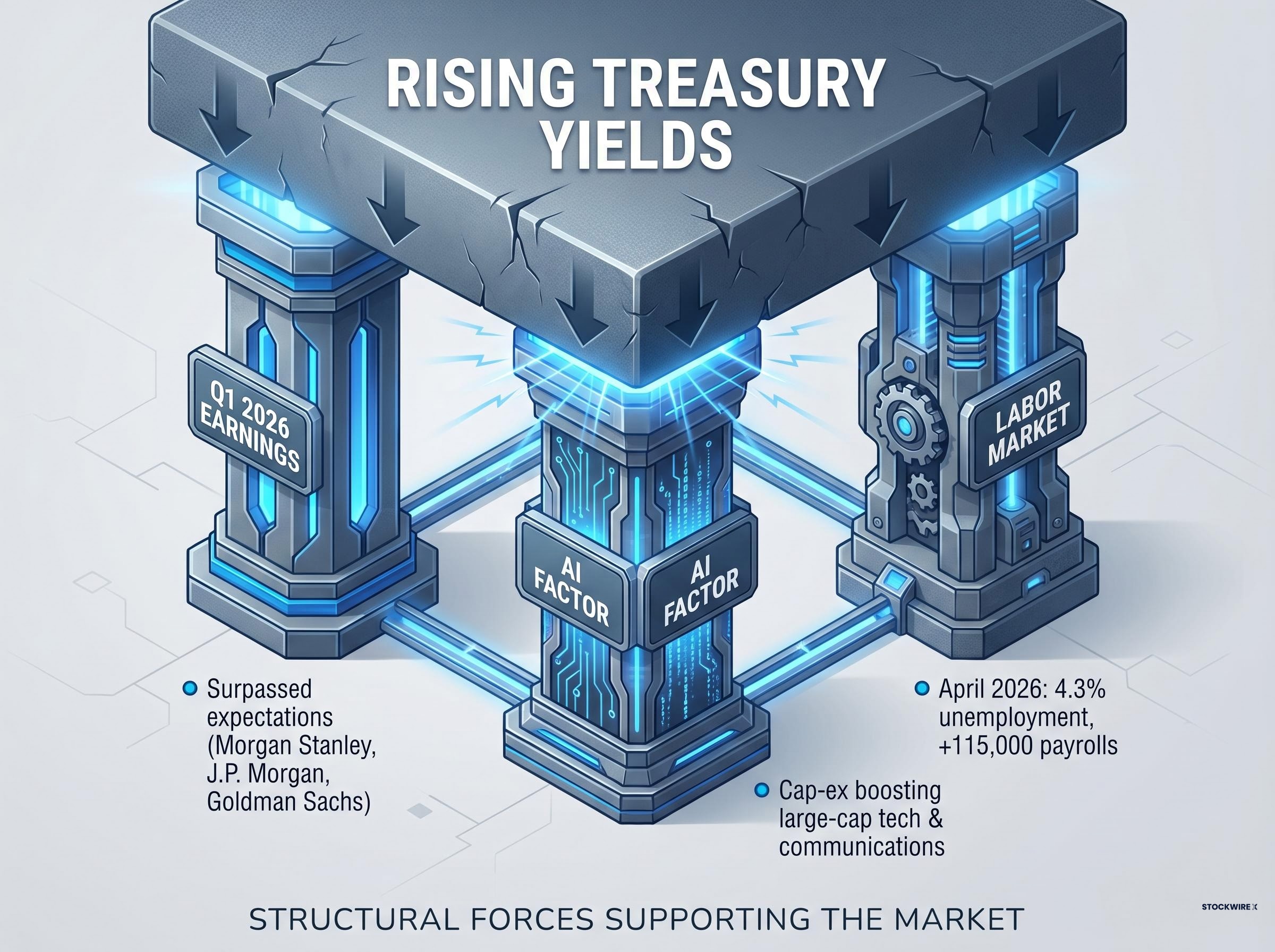

This is not routine market noise. A move of this speed and scale in the risk-free rate is supposed to reshape the mathematics of equity valuation. That it has not, at least not yet, is a puzzle worth unpacking. The explanation involves three specific forces, each doing measurable work to offset what higher yields would normally impose.

The relationship between higher yields and lower stock prices operates through three distinct channels. Each is grounded in financial mechanics rather than market sentiment, and none has been repealed.

The discount-rate mechanics at work here are not new: when Treasury yields rise, investors apply a higher rate to discount future corporate cash flows, which compresses the present value of those earnings even when the earnings themselves are unchanged, and the effect is sharpest for growth stocks whose value is concentrated furthest into the future.

These three channels are the reason the “higher yields hurt stocks” relationship exists. They have not stopped operating. What has happened is that a specific set of forces on the other side of the ledger has, so far, been strong enough to absorb them.

The abstract claim that “earnings have been strong” requires specifics before it carries analytical weight.

Q1 2026 corporate earnings broadly surpassed analyst expectations, with profit growth surprising to the upside relative to pre-season consensus. May 2026 strategy notes from Morgan Stanley, J.P. Morgan, and Goldman Sachs each characterised the earnings season as stronger than anticipated.

According to May 2026 strategy commentary from Morgan Stanley, J.P. Morgan, and Goldman Sachs, Q1 2026 earnings were described as “stronger than expected,” with profit growth surprising to the upside relative to pre-season consensus.

The sectors leading the beats were concentrated rather than broad:

The connection back to the discount-rate mechanism is direct. If expected future cash flows are revised upward quickly enough, a higher discount rate applied to those cash flows does not necessarily reduce their present value. The numerator (earnings expectations) grew fast enough to offset the denominator (the discount rate). This is not a permanent override. It is a race between two moving variables, and in Q1 2026, earnings ran faster.

Understanding this distinction matters. A market where earnings surprises are actively doing work to counterbalance yield pressure is fundamentally different from one that is simply ignoring the risk.

The S&P 500 is a market-capitalisation-weighted index, which means the stocks with the largest valuations move the headline number the most. In 2026, those stocks are overwhelmingly concentrated in large-cap technology and communication services, the same sectors at the centre of AI-driven capital expenditure. This is not a coincidence. It is the mechanism.

According to Wells Fargo (via Investing.com, 31 May 2026), enthusiasm for artificial intelligence continued to bolster technology sector shares and is considered a potential counterweight to elevated borrowing-cost headwinds. Morgan Stanley’s May 2026 commentary described ongoing AI investment and spending as a “central pillar” supporting U.S. equity markets, particularly for mega-cap technology and semiconductor names.

The specific reason these stocks have absorbed higher yields is that upward revisions to their long-term cash-flow expectations have, so far, outweighed the higher discount rate applied to those cash flows. Strategists describe the S&P 500 as increasingly “barbelled,” with AI beneficiaries offsetting rate-sensitive and cyclically exposed sectors.

AI concentration risk at the index level is more complex than headline S&P 500 volatility implies: the top five companies now control roughly 30% of total US market capitalisation, meaning low index-level volatility can mask sharply opposing moves by individual AI winners and losers that cancel each other out, leaving investors exposed to single-stock risk they believe they have diversified away.

| Factor | Direction of pressure | Current offset |

|---|---|---|

| Higher discount rate (10-year yield above 4.45%) | Downward pressure on equity valuations | AI-driven upward revisions to long-term cash-flow expectations have outpaced the discount-rate drag at the index level |

| AI capital expenditure and revenue growth | Upward pressure on mega-cap tech earnings | Heavy S&P 500 weighting in tech and communication services means AI gains disproportionately support the headline index |

The caution embedded in the same institutional commentary deserves equal weight. Valuations in some AI-linked names are increasingly reliant on very long-dated growth assumptions. A disappointment in AI revenue adoption, or a substantially higher yield, could quickly reverse this dynamic. The offset is real. It is also conditional.

The most recent official U.S. labour market data, covering April 2026 and released by the Bureau of Labor Statistics on 8 May 2026, delivered two numbers that anchor the macro case for equity resilience:

The chain from these figures to the equity market is direct. Continued job gains sustain consumer spending power. Consumer spending supports corporate revenues. Revenues that hold up reduce the probability of a near-term earnings deterioration, the scenario that would remove the first line of defence described earlier.

May 2026 macro commentary from Morgan Stanley, J.P. Morgan, and other institutional notes consistently described the labour market as “resilient” or “robust.” This characterisation matters for equity positioning because a labour market still adding jobs at 4.3% unemployment is not the environment in which corporate profits collapse. It is the macro floor beneath the entire resilience argument.

The next BLS Employment Situation release, covering May 2026 data, is scheduled for 5 June 2026. That report will be the next significant checkpoint for this thesis.

The April payrolls report carried a headline beat of 115,000 jobs, but beneath that number both ISM Manufacturing Employment and ISM Services Employment moved simultaneously into contraction territory, and involuntary part-time employment surged by 445,000, signals that complicate a straightforward reading of the labour market as uniformly resilient.

The resilience described above is conditional, not permanent. Two specific risks are flagged across May 2026 institutional strategy commentary, and both deserve attention.

The pace and origin of yield moves matters more than the level itself. A rapid, inflation- or deficit-driven spike is substantially more dangerous for equities than a gradual move reflecting growth optimism.

Neither of these risks requires prediction. They require monitoring. The difference between a market that is ignoring yields and one that is betting the offsets hold is the difference between complacency and a conditional thesis.

US fiscal deficit dynamics feed directly into term premia through the volume of Treasury issuance required to service $952 billion in annual interest payments, and Goldman Sachs has noted that rising yields have already compressed the S&P 500 equity risk premium to near multi-decade lows, reducing the valuation buffer against exactly the kind of earnings disappointment the article identifies as a break condition.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The S&P 500 at 7,580.06 on 29 May 2026, with the 10-year yield at 4.45% (still well above the late-February starting point of approximately 3.9%), is not a market that has forgotten how yields work. It is a market where three specific forces, stronger-than-expected earnings, AI-driven cash-flow revisions, and a labour market still adding jobs, have so far been strong enough to absorb the pressure.

This is a conditional equilibrium, not a permanent regime change. The yield-equity relationship has not been repealed. It has been temporarily offset by a specific configuration of fundamentals. The variables to watch are the pace of any further yield moves, the next earnings season’s ability to repeat Q1’s upside surprises, and AI revenue adoption data as it emerges through the second half of 2026. The BLS release on 5 June will test the labour market pillar. Investors who understand the equilibrium as conditional are better positioned to update their view quickly when the conditions shift.

Rising Treasury yields typically pressure stock prices through three channels: higher discount rates reduce the present value of future corporate cash flows, risk-free bonds become more competitive with equities for capital, and elevated borrowing costs slow economic growth and corporate earnings.

Three forces have offset the usual yield pressure in 2026: Q1 corporate earnings broadly surpassed expectations, AI-driven capital expenditure has lifted long-term cash-flow revisions for the index's heaviest stocks, and the labour market remains resilient with unemployment at 4.3% and 115,000 nonfarm payrolls added in April.

Because the S&P 500 is market-cap weighted and mega-cap technology and communication services companies represent a large share of the index, upward revisions to their long-term cash-flow expectations from AI investment have so far outweighed the drag from higher discount rates, partially insulating the headline index from yield pressure.

Institutional strategists at Morgan Stanley, J.P. Morgan, and Goldman Sachs identify two key break conditions: a disorderly yield spike well above current ranges driven by sticky inflation, fiscal deficit concerns, or rising term premia, and a disappointment in AI revenue adoption that would erode the earnings-revision offset supporting mega-cap valuations.

The BLS Employment Situation report covering May 2026 data, scheduled for 5 June 2026, is the next major checkpoint for the labour market pillar, while Q2 earnings results and AI revenue adoption disclosures through the second half of 2026 will test whether the earnings offset can be repeated.