Piper Sandler Says the US Fiscal Crisis Has Already Begun

56 mins ago

Coles shares closed at A$21.47 on 22 May 2026, sitting just 6.6% above the 52-week low of A$20.10, yet four major brokers now carry Buy ratings with price targets ranging from A$23.00 to A$25.50. That disconnect between a share price lingering near its annual floor and a consensus that implies 9% to 11% upside is the tension at the centre of the Coles investment case right now. For ASX investors weighing consumer staples exposure and dividend income, the question is straightforward: does COL at current levels represent genuine value, or does it simply look cheap relative to a recent trough? What follows is a structured assessment drawing on verified financial results, broker data, competitive dynamics, and yield context, built to deliver a grounded answer.

The baseline matters before any valuation judgment. Coles trades at A$21.47 with a 52-week range of A$20.10 to A$24.28, placing it closer to the midpoint of that range than the floor. The market capitalisation sits at approximately A$28.84 billion.

Framing the stock as “near its lows” overstates the discount. The midpoint of the annual range is A$22.19, and the current price is less than 3.3% below it. That is a stock trading in the middle of its band, not one priced for distress.

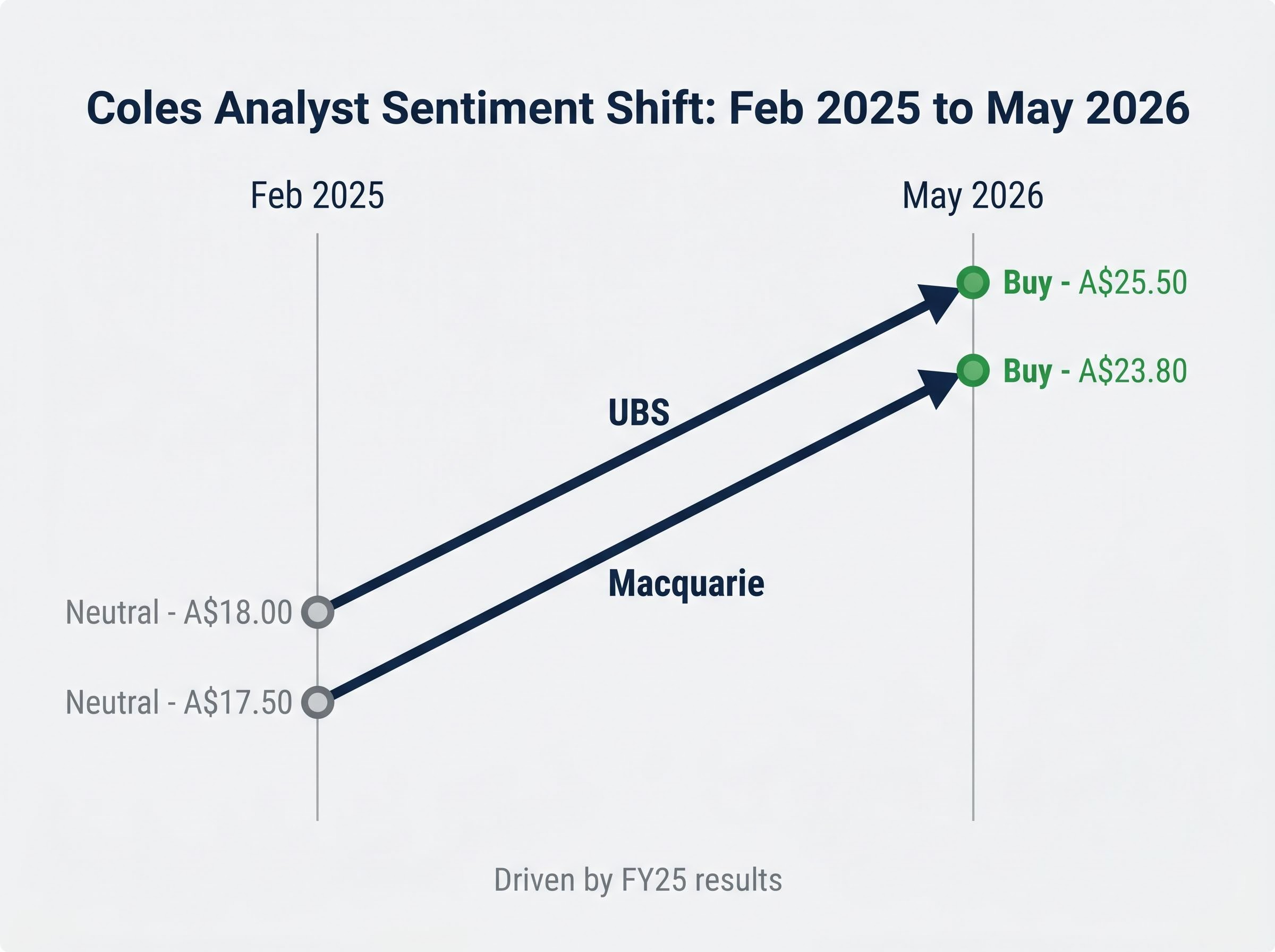

The shift in analyst sentiment since early 2025 has been pronounced. In February 2025, UBS held a Neutral rating with a target of A$18.00, and Macquarie sat at Neutral with A$17.50. By May 2026, both had upgraded to Buy with materially higher targets, a move driven directly by FY25 results that exceeded the subdued expectations embedded in earlier forecasts.

| Broker | Rating | Price Target |

|---|---|---|

| UBS | Buy | A$25.50 |

| Macquarie | Buy | A$23.80 |

| JPMorgan | Buy | A$24.10 |

| Jefferies | Buy | A$23.00 |

The broader consensus, drawn from 15 to 16 analysts, averages A$23.41 to A$23.89. The full range extends from a floor around A$16.50 to A$22.60 to a ceiling of A$25.50 to A$26.10, reflecting meaningful dispersion. The weight of the coverage, however, leans positive.

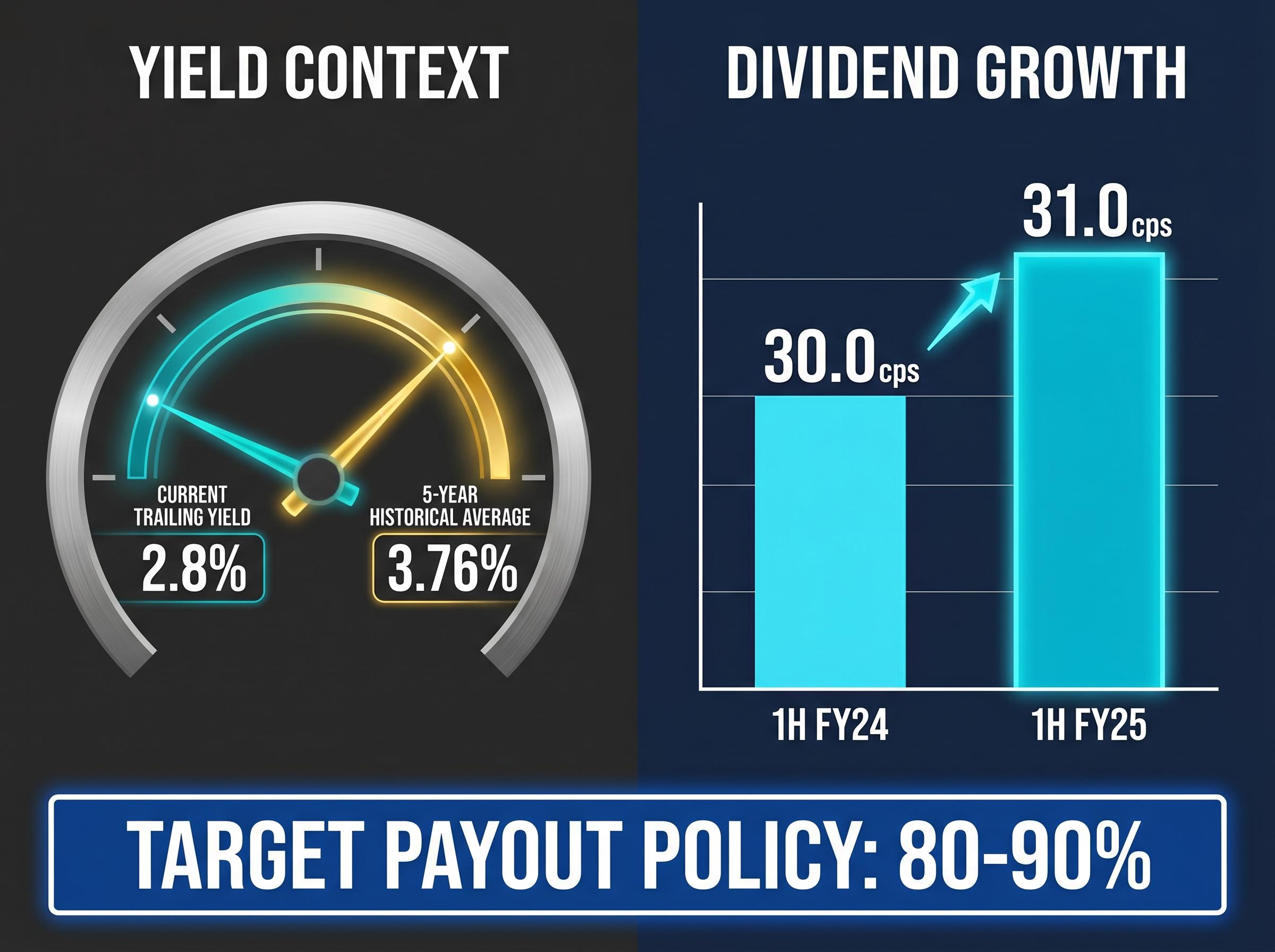

The trailing yield is the number that draws income investors to the search bar. Based on the FY24 total dividend of 60.0 cents per share (fully franked) and a share price of A$21.47, the implied trailing yield is approximately 2.8%. That figure sits meaningfully below the five-year historical average of approximately 3.76%.

A below-average yield, though, does not tell a single story. Three mechanisms can push a yield below its historical average:

The distinction matters. A compressed yield driven by price appreciation signals a market willing to pay more for the income stream, not a deteriorating payout.

According to Morgans Financial commentary from early 2025, Coles’ yield was characterised as “adequate rather than compelling,” with the firm advising income investors to buy on weakness rather than chase rallies.

Coles’ 80-90% payout policy, reiterated on 25 February 2025, acts as both anchor and ceiling. It underpins dividend reliability but limits the pace of growth. Yield expansion, for investors seeking it, will likely require price weakness rather than payout acceleration.

Coles Group is broader than a supermarket chain. Founded in 1914 in Victoria, the company operated within Wesfarmers from 2007 before being independently listed on the ASX as COL in 2018. It has paid dividends consistently since listing.

The business spans several divisions:

Coles holds approximately 28% of Australian grocery retail, operating in a duopoly with Woolworths that faces structural disruption. Woolworths outperformed Coles in Australian Food comparable sales growth in FY24, attributed to stronger loyalty engagement and perceived value.

Aldi’s continued east-coast expansion adds a third dimension to the competitive pressure. Macquarie has described Aldi’s presence as a structural drag on supermarket gross margins. Coles has responded with an expansion of its Own Brand ranges and Everyday Low Price positioning to defend volume share, but these tools compress margins even as they protect market share.

The FY25 full-year results, released 26 August 2025, did the work that shifted broker sentiment. Revenue reached A$44.4 billion, underlying net profit after tax (NPAT) came in at A$1.18 billion, normalised sales growth hit 3.6%, and underlying earnings before interest and tax (EBIT) grew 6.8%. Each of these figures exceeded the subdued expectations that had characterised analyst commentary through early 2025.

The trajectory becomes clearer when set against the prior periods.

| Metric | FY24 | 1H FY25 | FY25 |

|---|---|---|---|

| Revenue | A$41.98B | A$21.19B | A$44.4B |

| NPAT | A$1.05B | A$520M | A$1.18B |

| Dividend (per share) | 60.0 cps | 31.0 cps (interim) | Pending final |

Wage and energy inflation remained headwinds through the period, partially offset by ongoing automation and efficiency investment across the supply chain. The earnings progression confirms a business growing rather than stagnating, which is the precondition for any meaningful dividend growth. The upgrade cycle from Neutral to Buy across multiple brokers was evidence-based, not speculative.

A Buy consensus and growing earnings do not eliminate the risks. Three categories warrant clear-eyed assessment:

A portfolio manager surveyed by the Australian Financial Review in early 2025 described Coles’ yield as “adequate rather than compelling,” expressing a preference to add on price dips closer to the 52-week low.

Goldman Sachs noted in September 2024 that consensus margin recovery forecasts may have been too optimistic, a view that, while partially challenged by the FY25 results, still applies to the forward outlook in a structurally competitive market. These risks are not thesis-breaking, but they do limit conviction at prevailing yield levels.

The evidence points to a specific conclusion. The FY25 earnings beat, a predominantly Buy broker consensus with average targets implying 9% to 11% upside, and a growing (if modest) dividend stream describe a stock that is fairly priced for a defensive income position. It is not deeply discounted.

The case for and against adding COL at current levels splits along investor type:

Dividend yield comparison is a useful starting signal, but investors seeking a complete picture should consider applying a discounted cash flow (DCF) or Dividend Discount Model analysis. The 80-90% payout policy and the moderate earnings growth trajectory of 3% to 7% per annum implied by the FY25 results provide the inputs for that work. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

Coles is a well-capitalised, consistently profitable duopoly player with a reliable fully franked dividend and moderate broker-supported upside. It is not, however, a stock offering a compelling discount at current levels. Income investors should calibrate expectations accordingly: this is a defensive hold with a credible path to modest capital appreciation, not a mispriced opportunity.

The catalysts to watch from here are the 1H FY26 results, further developments from the ACCC pricing review, and the next dividend declaration, each of which will either strengthen or soften the investment case at prevailing prices. Yield comparisons offer a starting point, but DCF and Dividend Discount Model frameworks provide a more complete valuation lens for a stock with Coles’ payout structure.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Coles shares closed at A$21.47 on 22 May 2026, sitting within a 52-week range of A$20.10 to A$24.28, placing the stock near the midpoint of its annual trading band rather than at a deeply discounted level.

Coles paid a total FY24 dividend of 60.0 cents per share (fully franked), implying a trailing yield of approximately 2.8% at the current share price, which is below the five-year historical average of around 3.76%.

Four major brokers currently hold Buy ratings on Coles with price targets ranging from A$23.00 (Jefferies) to A$25.50 (UBS), while the broader consensus across 15 to 16 analysts averages between A$23.41 and A$23.89.

Key risks include ongoing ACCC regulatory scrutiny into supermarket pricing, competitive pressure from Woolworths and Aldi's east-coast expansion, and a trailing dividend yield that currently sits below its five-year average, limiting compensation for income investors at today's price.

Coles reported FY25 revenue of A$44.4 billion, underlying NPAT of A$1.18 billion, normalised sales growth of 3.6%, and underlying EBIT growth of 6.8%, all of which exceeded the subdued expectations that had characterised analyst forecasts earlier in 2025.