APRA Warns Banks: AI Governance Failing Across $9.8tn Sector

22 hrs ago

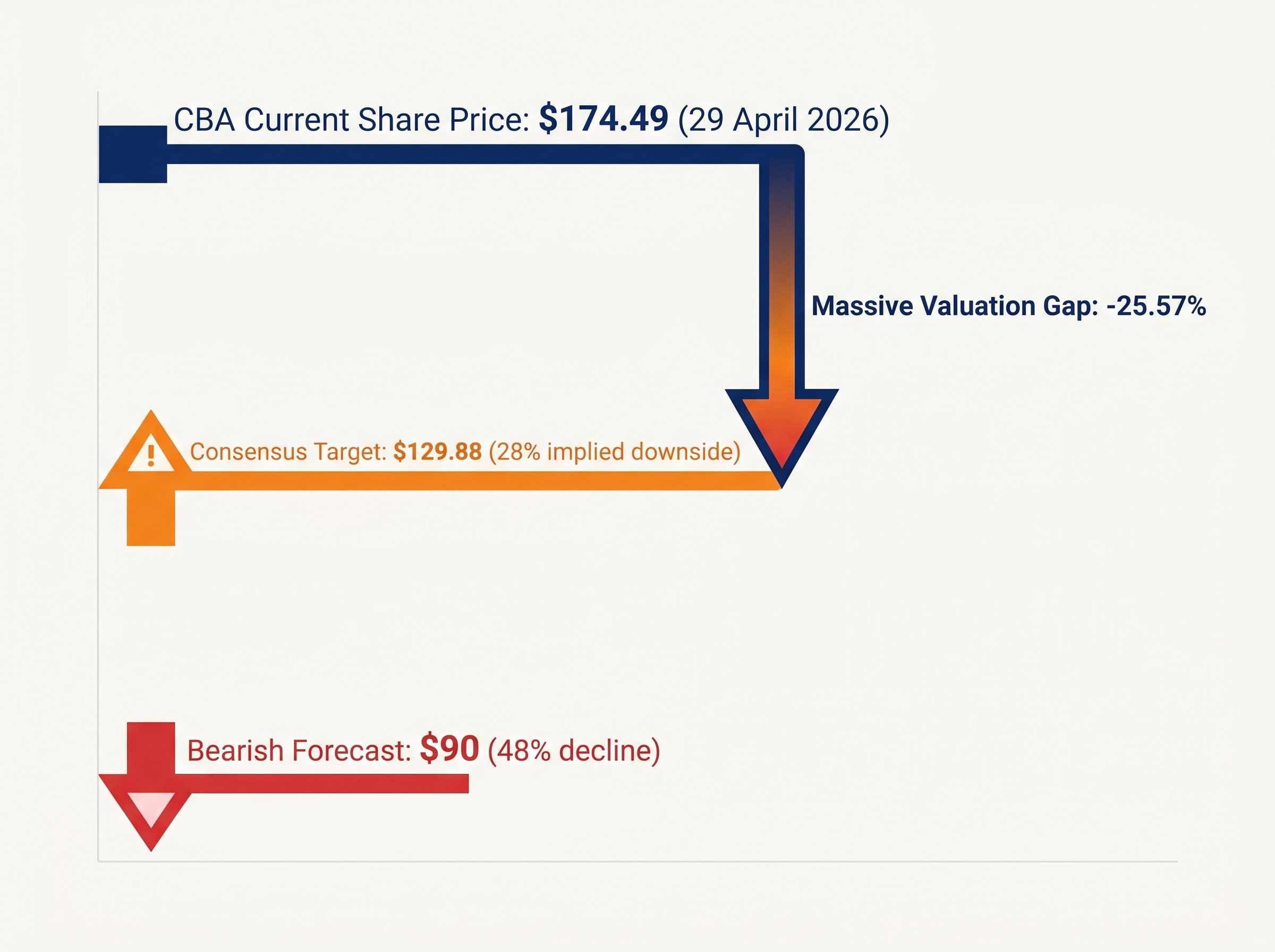

Fourteen of sixteen analysts covering Commonwealth Bank of Australia (CBA) are telling investors to sell. The stock closed at $174.49 on 29 April 2026, up more than 10% year-to-date, with a market capitalisation of approximately $291.4 billion. The consensus analyst price target of roughly $129.88 implies 28% downside from current levels, one of the most striking disconnects between market pricing and professional opinion anywhere on the ASX. What follows is a framework for understanding why that gap exists, what it means for CBA’s share price outlook, and what would need to change for the consensus to shift. Whether CBA sits as a core holding or a watchlist candidate, the numbers demand a clear-eyed assessment of the risk.

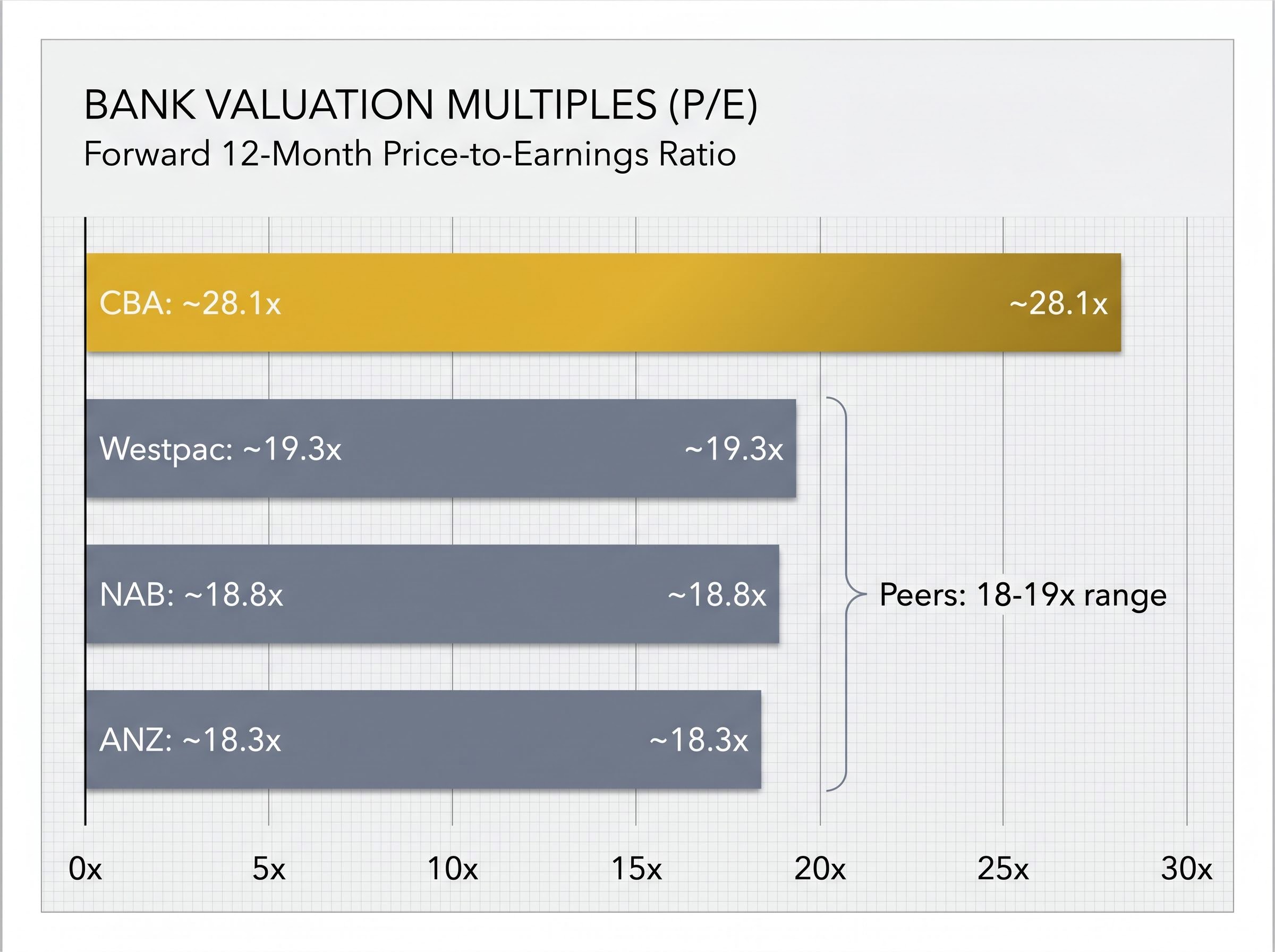

Start with the earnings multiple. CBA trades at a price-to-earnings ratio of approximately 28x, derived from a share price of $174.49 and trailing earnings per share of roughly $6.21. For a bank, in a mature lending market, with no high-growth catalyst on the horizon, that multiple carries weight.

The analyst community has drawn its conclusion. According to TradingView consensus data, 14 of 16 brokers covering CBA rate it Sell or Strong Sell. The remaining two hold neutral positions. Not a single analyst carries a Buy rating.

14 out of 16 analysts rate CBA as Sell or Strong Sell. Zero carry a Buy recommendation, a degree of bearish consensus rarely seen on Australia’s largest listed company.

The consensus 12-month price target sits at approximately $129.88, implying roughly 28% downside. The most bearish forecast falls as low as $90, which would represent a decline of nearly 48% from current levels.

The key valuation metrics, taken together, frame the scale of the concern:

For retail investors holding CBA as a portfolio anchor, these figures are the starting point for any hold-or-exit decision. The market is pricing the stock in one direction. Nearly every professional analyst is pointing in the other.

A premium multiple for CBA is not unusual. It has historically commanded a higher rating than its major Australian banking peers, reflecting its larger deposit franchise, stronger technology platform, and dominant position in home lending.

The question is whether the current premium has stretched beyond what those advantages justify. At approximately 28.1x trailing earnings, CBA trades at a 40-50% premium to NAB, Westpac, and ANZ, all of which sit in the 18-19x range.

| Bank | P/E Ratio | Share Price (approx.) | Analyst Consensus |

|---|---|---|---|

| CBA | ~28.1x | $174.49 | Sell / Strong Sell |

| NAB | ~18.8x | — | Mixed |

| Westpac | ~19.3x | $39.01 | Strong Sell |

| ANZ | ~18.3x | — | Mixed |

The gap is not confined to CBA alone. Westpac itself faces broker downgrades, with a consensus price target of $34.75 implying approximately 11% downside from its recent close of $39.01. Westpac’s year-to-date return of roughly +1% and a 12-month return of approximately +22% suggest the broader sector is encountering valuation resistance, not just CBA.

ANZ’s contrasting analyst consensus, where buy ratings outnumber sell ratings and the implied downside sits near 4% rather than 28%, illustrates that the valuation concern is not a blanket indictment of Australian banking but a judgment about where individual franchises sit relative to their earnings trajectories.

Still, CBA’s premium is in a category of its own. Paying 28x for a bank when three comparable institutions trade below 20x requires conviction that the quality gap is not only real but widening. The peer data suggests otherwise.

CBA’s 28x multiple is not an isolated anomaly but the sharpest expression of a broader Big Four valuation problem: record profits across the sector in recent years have been met with higher share prices rather than earnings-driven multiple compression, pushing all four banks further above analyst targets rather than closer to them.

The bull case for CBA is genuine, and dismissing it would weaken the analysis. Four structural advantages underpin the premium argument:

These are not trivial. A premium multiple for the highest-quality franchise in Australian banking has been historically defensible, and long-term holders have been rewarded: CBA’s year-to-date appreciation of 10.13% compares with Westpac’s roughly +1% over the same period.

The trailing dividend yield of approximately 2.83%, supported by an interim distribution of $2.35 per share (fully franked, declared February 2026), adds a further income argument.

Zero analysts in CBA’s 16-broker coverage universe carry a Buy rating. The bull case for quality is real; the question is whether 28x earnings is the right price to pay for it.

That is the precise tension. The argument is not that CBA is a poor business. It clearly is not. The argument is that the current multiple, at 28x, has priced in the quality advantage and then some. When no single professional analyst covering the stock is willing to recommend purchasing it, the burden of proof shifts to those paying the premium to explain what the market sees that 16 research teams do not.

The Reserve Bank of Australia raised the cash rate to 4.10% in March 2026, and a further hike is under consideration for May 2026. For a bank as mortgage-dependent as CBA, the rate environment is not background context. It is a direct input into the earnings equation, and it cuts in two directions at once.

Net interest margin (NIM) is the difference between the rate a bank earns on its loans and the rate it pays on its deposits, expressed as a percentage of earning assets. It is the single most important driver of bank profitability.

When the RBA lifts rates, banks can typically reprice their loan books faster than they reprice deposit accounts. That gap temporarily widens NIM, boosting earnings. This is the mechanism behind the common assumption that higher rates are straightforwardly good for banks.

The offset is less visible but equally real. If higher rates slow new lending activity or cause borrowers to default, the volume and quality of the earning asset base shrinks, eroding the margin benefit from the other side.

RBA research on interest rates and bank profitability finds that the relationship between rising rates and net interest margins is more complex than the simple pass-through narrative suggests, with volume effects and deposit repricing dynamics often offsetting the headline margin benefit for mortgage-concentrated lenders.

For CBA, the dual effect is particularly acute:

Net interest margin compression to 2.04% in CBA’s H1 FY2026 result is the most concrete earnings-level evidence of the rate environment’s dual effect: the benefit of faster loan repricing has not been sufficient to offset the competitive pressure on deposit costs, tightening the spread that underpins the entire profitability argument.

Potential upside from higher rates:

Potential downside from higher rates:

Many retail investors assume higher rates are simply beneficial for banks. For a franchise as concentrated in mortgage lending as CBA, the reality is more layered. The March 2026 hike and any May 2026 increase add a further dimension of earnings uncertainty to a stock already trading at a stretched multiple.

The near-unanimous sell consensus is not permanent. Analyst ratings respond to changing fundamentals. The specific conditions that could logically trigger upward revisions fall into a narrow set of outcomes:

Recent broker activity illustrates how narrow the optimism is, even among those revising targets upward. Morgan Stanley maintained a Sell rating with a $131.20 target as recently as 7 April 2026. UBS raised its target to $130 from $125 following CBA’s February 2026 half-year results, but that upward revision still implies roughly 25% downside from current levels. Morgans continued to rate CBA as overvalued in April 2026 updates.

The arithmetic is stark. CBA’s share price would need to fall approximately $44.61 per share, roughly 28%, simply to reach the consensus target. That target is itself not a Buy recommendation; it is an estimate of fair value from analysts already telling clients to sell.

CBA’s five-year share price appreciation of approximately 96% has rewarded long-term holders generously, significantly outpacing the ASX 200’s roughly 24% return over the same period. That track record is real.

It is also irrelevant to the current risk. Historical gains do not reduce the gap between today’s price of $174.49 and the consensus fair value estimate of $129.88. A trailing dividend yield of 2.83% does not meaningfully offset 28% implied downside.

The core tension is straightforward. CBA is a genuine quality business, trading at a price that 14 of its 16 professional analysts consider too expensive, in a rate environment that complicates its earnings outlook, with a dividend yield that provides limited cushion.

The question for CBA holders is not “is CBA a good bank?” It clearly is. The question is: at $174 per share, is the price proportionate to what is being purchased?

This is not a question that resolves itself through patience alone. It requires an active assessment of whether the premium reflects future value creation or simply the momentum of past performance.

For SMSF trustees and retirees relying on CBA’s fully franked dividend stream, our dedicated guide to CBA’s valuation for SMSF trustees examines how the income case interacts with position sizing risk, portfolio concentration, and the specific considerations that apply when CBA represents a core income holding rather than a speculative position.

The analytical thread runs through every layer of CBA’s story: a P/E of 28x against peers below 20x, near-unanimous sell consensus, a macro environment that pressures the bank’s largest revenue line, and a dividend yield too thin to compensate for the implied downside. CBA could continue rising in the short term; momentum and retail demand can sustain premiums longer than analysts anticipate. That possibility does not change the valuation arithmetic.

The next step for holders is specific: revisit portfolio weighting in CBA against individual risk tolerance, and track the triggers identified here, including earnings updates, RBA rate decisions, and analyst revisions. A 28% gap between market price and professional consensus is large enough to require an active decision, not a passive one.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

As of late April 2026, 14 of 16 analysts covering CBA rate the stock a Sell or Strong Sell, with a consensus 12-month price target of approximately $129.88, implying around 28% downside from the current price of $174.49.

CBA trades at roughly 28x trailing earnings, a 40-50% premium to NAB, Westpac, and ANZ which all trade in the 18-19x range, and analysts argue that CBA's quality advantages do not justify paying such a steep premium over comparable franchises.

Higher rates can temporarily widen net interest margins by allowing faster loan repricing, but CBA's heavy concentration in mortgage lending also exposes it to slower new origination, affordability headwinds, and potential credit quality deterioration, and CBA's NIM already compressed to 2.04% in H1 FY2026.

Analysts would likely revise their view if CBA delivers strong enough earnings-per-share growth to compress its P/E toward the low 20s, demonstrates sustained net interest margin expansion without credit quality deterioration, or if the share price falls materially toward the consensus target around $130.

CBA's trailing dividend yield of approximately 2.83%, supported by a fully franked interim dividend of $2.35 per share declared in February 2026, provides limited income cushion when set against the roughly 28% downside implied by the analyst consensus price target.